Embedded Non-volatile Memory (eNVM) in 2026: Strategic Compass for Decision-makers

Introduction — Why this study matters for enterprise strategy in 2026

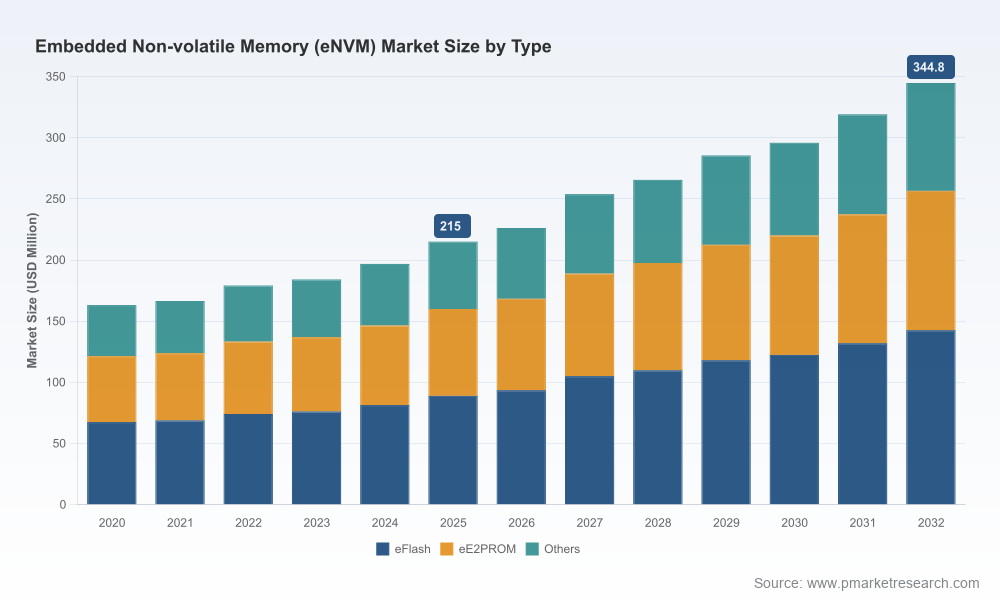

The embedded non‑volatile memory (eNVM) market is entering a phase of accelerated structural change that will shape semiconductor roadmaps, supplier strategies, and product architectures for the next decade. Our PW Consulting market study — anchored on a 2025 base year and projecting through 2032 — shows a sustained compound annual growth rate (CAGR) of 11.54%. The market has expanded consistently in the 2020–2025 historical window and is forecast to continue rising through 2032, reflecting broad adoption of emerging memory technologies in automotive, industrial, IoT and consumer domains. For executives and product leaders planning capital allocation, IP licensing, foundry partnerships or M&A in 2026, this research provides the evidence base needed to convert strategic intent into executable roadmaps.

Embedded Non-volatile Memory (eNVM) Market

Market trajectory — the macro view

From a strategic perspective, two macro facts drive all tactical choices: (1) eNVM is no longer a niche peripheral; it is a design-in lever that affects die-area economics, system reliability, and lifecycle cost; and (2) the overall market scale and growth profile make it a material factor for any MCUs, SoCs, and edge processors targeted at automotive, industrial and high-reliability applications. Our study quantifies that expansion from the 2025 baseline through 2032 and models multiple scenarios that reflect technology substitution, foundry availability and regulatory tightening. These macro outputs enable scenario planning — from conservative adoption to accelerated migration — and feed directly into TCO, roadmap phasing and go/no-go decisions for 2026 projects.

Embedded Non-volatile Memory (eNVM) Market

Key dynamics shaping eNVM decisions

- Technology heterogeneity and maturity: Multiple embedded memory technologies (including emerging MRAM, ReRAM/PCM, FRAM and advanced embedded flash variants) coexist. Each brings distinct trade-offs across write endurance, retention, power, and integration complexity. Product architects must choose not just on die metrics but on system-level implications (e.g., boot-time persistence, safety-state retention, and in-field updates).

- Manufacturing and integration cost pressure: Embedding non‑standard memory cells often requires additional process steps, non‑standard tooling and extended verification — elevating unit and NRE costs. Our models quantify cost-kicker stages and breakpoints where economies of scale or licensing make sense.

- Regulatory and reliability constraints: Automotive and industrial segments demand extended temperature ranges, longevity and functional safety compliance (e.g., AEC‑level qualifications). These constraints materially influence supplier selection, qualification timelines and warranty exposure.

- Geopolitical and foundry diversification risk: Regional supply footprints and the increasing role of diverse foundry partners affect lead times, IP portability and procurement risk. Our analysis flags critical sourcing contingencies and regional concentration risks for 2026 planning.

- Certification and high‑reliability requirements: Aerospace and space applications add layers of qualification (radiation‑hardened options, specialized test programs). The implications are longer development cycles and higher unit cost, but also higher margins where qualification barriers exist.

Competitive landscape — who matters and why

The eNVM ecosystem comprises large IDM and fabless vendors, specialized IP licensors, and foundries embedding memory directly into process stacks. Our report profiles the strategic positioning of the leading players, and below we summarize the roles these organizations play in the value chain:

Embedded Non-volatile Memory (eNVM) Market

- Samsung Electronics (Seoul): A major developer and manufacturer of embedded STT‑MRAM and advanced flash solutions, Samsung’s vertical integration and process leadership influence availability of high‑performance embedded options for SoC vendors.

- STMicroelectronics (Geneva): Differentiates through integration of PCM and RRAM into FD‑SOI MCUs, targeting automotive and industrial use cases that require reliability and low power.

- Infineon Technologies (Neubiberg): Positions embedded FRAM and RRAM within automotive controllers and edge ML processors, stressing functional safety and deterministic behaviour.

- NXP Semiconductors (Eindhoven): Leverages advanced nodes and foundry partnerships to deliver MRAM‑embedded automotive MCUs, with a focus on secure, high‑temperature automotive environments.

- Renesas Electronics (Tokyo): Offers a portfolio mixing STT‑MRAM and advanced flash for industrial and IoT MCUs, balancing legacy compatibility with next‑gen features.

- Texas Instruments (Dallas): Integrates ferroelectric and flash eNVM solutions across MCUs and processors where deterministic analog‑digital behaviour is important.

- Microchip Technology (Chandler): Sustains a strong embedded flash and NOR presence in low‑power embedded systems and niche industrial MCUs.

- Weebit Nano (Tel Aviv): Plays the IP/licensing role for embedded ReRAM, rapidly progressing platform qualifications and licensing agreements that matter for mixed‑signal and high‑voltage foundry nodes.

- Everspin Technologies (Gilbert): Specializes in MRAM with a focus on automotive, aerospace and industrial high‑reliability products and recent portfolio expansions to meet qualification demands.

- TSMC (Hsinchu) and GlobalFoundries (Santa Clara): Both embed MRAM/ReRAM options in advanced process nodes and FD platforms; their roadmap choices directly shape which memory technologies can be designed into modern MCUs and SoCs.

Our competitive analysis goes beyond vendor descriptions; it assesses vertical integration, IP openness, foundry ties, qualification timelines and long‑term support commitments — variables that determine whether a vendor is a tactical supplier or a strategic partner for 2026‑era programs.

Recent developments to watch (implications for 2026)

- IP licensing and platform qualifications accelerated in early 2025, enabling ReRAM to reach a wider set of mixed‑signal and automotive‑grade process nodes — an indicator that licensing strategies will be an actionable lever for OEMs looking to diversify memory sources.

- Product expansions of MRAM portfolios with automotive and aerospace qualification signal a maturing supply chain for high‑reliability embedded memory — shortening the path from evaluation to production for safety‑critical systems.

- Foundry and regional supply footprint shifts continue to create windows of opportunity as well as concentration risk; companies must balance cost, qualification speed and geopolitical exposure when deciding 2026 sourcing strategies.

What PW Consulting’s study delivers (practical, executable outputs)

This report is explicitly designed as a decisioning tool for 2026. Highlights of the deliverables include:

- Scenario‑based market models (2026–2032) with sensitivity analyses that map technology substitution thresholds and price points.

- Supplier heatmaps and decision matrices that combine technical readiness, qualification timelines, IP risk and commercial openness.

- Manufacturing pathway options and NRE/capex templates that quantify when in‑house integration, licensing or outsourcing is optimal.

- Product architecture playbooks illustrating when to prioritize persistence, endurance or radiation hardness in eNVM selection.

- M&A and partnership playbooks highlighting bolt‑on targets, licensing plays and joint‑development structures prioritized by ROI and time‑to‑market.

- Regulatory and test‑plan checklists for automotive, industrial and aerospace segments, reducing qualification surprises.

Note: This introduction purposefully omits granular segment and regional splits; the full report contains the detailed segment-level forecasts, supplier scorecards, and line-item financial models that underpin the summarized recommendations above.

Strategic imperatives for executives planning in 2026

- Decide on memory architecture early: The choice of embedded technology affects die area, power budgeting, and safety validation. Locking architecture in late forces expensive rework; early decisions enable cost optimization and smoother qualification.

- Diversify foundry and IP exposure: Build parallel paths with at least one major foundry partner and one IP/licensing route to hedge against availability or geopolitical disruptions.

- Budget for extended qualification: Automotive‑grade and aerospace projects will experience longer qualification timelines. Integrate these timelines into product roadmaps and revenue projections to avoid launch slippage.

- Use supplier scorecards as contractual anchors: Incorporate qualification milestones, IP support commitments and longevity guarantees into supplier contracts to protect roadmap continuity.

- Explore licensing where speed matters: For mixed‑signal or high‑voltage nodes, licensing a validated ReRAM or MRAM IP can compress time‑to‑market versus in‑house development.

- Plan for margin impact in high‑reliability niches: Although qualification adds cost, authorized suppliers commanding this space allow for premium pricing — align product and go‑to‑market strategies accordingly.

Next steps — how to use this intelligence in 2026

For teams preparing 2026 investment cycles, this study should be used to: (1) stress‑test capital plans against the alternative adoption scenarios in our model; (2) select a primary and contingency supplier path informed by our supplier heatmaps; and (3) set contractual milestones tied to qualification that convert supplier promise into enforceable timelines. The full PW Consulting report contains the segment‑level forecasts, vendor scorecards, cost‑build templates and granular due‑diligence checklists that operational teams will need to execute these steps.

PW Consulting has structured this introductory briefing to demonstrate the analytical depth we apply while reserving the proprietary, granular segment outputs for the full report. Access the complete study to obtain the fine‑grained forecasts, downloadable financial models, supplier RFP templates and the tactical playbooks required to convert eNVM market opportunity into measurable 2026 outcomes.

For detailed analysis of this topic, please visit the official page:Embedded Non-volatile Memory (eNVM) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com