How Is the Electric Cargo Bike Market Transforming Urban Logistics?

Networking |

2026-04-06 05:43:02

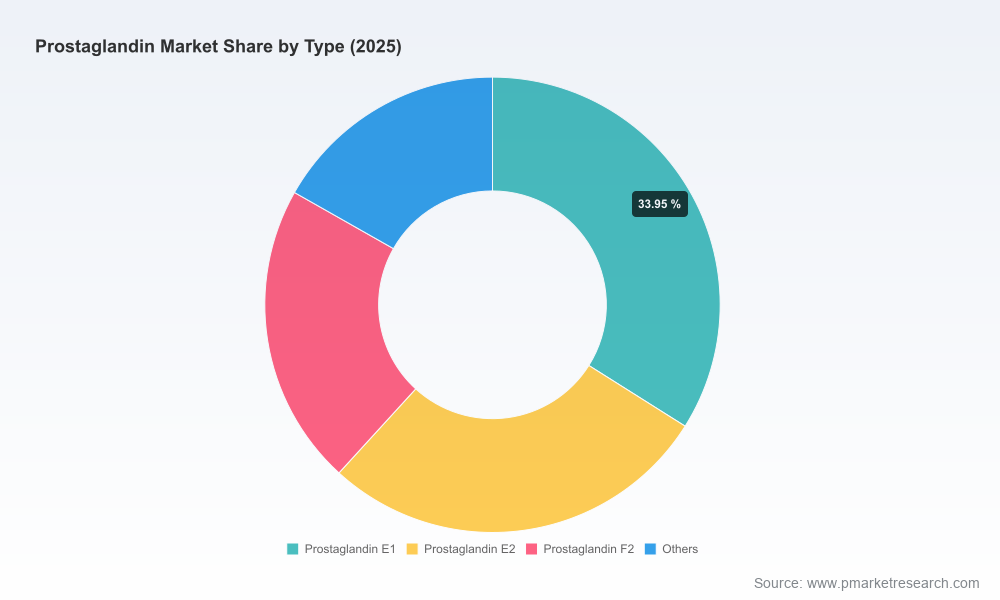

As the prostaglandin market enters 2026, it is no longer a niche biochemical supply story: it is a strategic battleground spanning ophthalmology, obstetrics/gynecology, cardiovascular therapies, and adjacent specialty uses. Our base-year assessment (2025) places the global market at approximately USD 4,470 million, having expanded from roughly USD 3,300 million in 2020. Under a 2026–2032 forecast horizon, PW Consulting’s modeling projects a steady compound annual growth rate of 6.5%, with the market approaching roughly USD 6,901 million by 2032. Market concentration is material — the top three players account for a majority share (CR3 ~58.5%), and the top five increase that dominance further (CR5 ~68.2%) — creating both predictable supplier power and tactical openings for challengers and consolidators.

Prostaglandin Market

Time-sensitive supply risk: A high share of API and intermediate production sits in a small set of geographies, exposing procurement to geopolitical, tariff and logistics shocks. For any commercial plan dependent on uninterrupted supplies, 2026 is the year to harden sourcing strategies.

Prostaglandin Market

Regulatory inflection points: New regulatory opinions and tariff regimes enacted since 2024–2025 have altered both cost and permissible end-uses for prostaglandin analogues. Firms that assumed steady cosmetic or export demand must re-evaluate product lifecycles and compliance roadmaps.

Prostaglandin Market

Technological disruption on the horizon: Recent academic and industrial advances in biosynthetic routes suggest a credible path to materially lower-cost production in the medium term. Companies needs to decide now whether to invest, partner, or purchase optionality through licensing.

Reimbursement and commercial inflection: Procedure-level reimbursement updates and incremental regulatory approvals in ophthalmology create revenue models that favor device-drug combinations and implantable delivery systems — a structurally different commercial play than commodity API sales.

Robust market sizing and bottom-up forecast model (base year 2025) with scenario envelopes and sensitivity toggles for prices, raw-material shocks, and tariff scenarios. Please note: the public preview intentionally withholds granular regional and application split tables; these are included in the full dataset.

Segmentation framework by type, application and value-chain node, with unit economics and margin waterfalls for APIs, intermediates, formulated products and device-adjacent offerings.

Vendor and competitor playbooks: strategic positioning, capability assessment, manufacturing footprint mapping, and partnership readiness scores for more than a dozen manufacturers and suppliers.

Supply-chain risk matrix and mitigation playbook: dual-sourcing strategies, inventory optimization templates, and contract structures to blunt tariff and logistics shocks.

Regulatory & reimbursement tracker with impact mapping — including testing thresholds, cosmetic-use constraints, and procedure coding changes for implant-based therapies.

M&A and alliance decision support: valuation sensitivity, integration risk checklist, and buyer/seller playbooks tailored to strategic acquirers, private equity and mid-market players.

Primary research: over 40 stakeholder interviews across manufacturers, formulators, payers and clinical innovators; market-sourced price curves and commercial benchmarks are in the full report package.

The prostaglandin ecosystem is populated by a mix of integrated pharmaceutical multinationals, specialty fine-chemical houses, contract manufacturers and research-reagent suppliers. Each plays a distinct role within the value chain.

Integrated API and pharma players (example profiles) — Several established API manufacturers provide end-to-end capabilities, from synthetic chemistry to GMP API supply and formulation. Their strategic advantages include regulatory heritage and existing commercial channels; their risks include exposure to raw material cost inflation and long-cycle capex for regionalization.

Fine chemicals and intermediates specialists — Firms focused on catalysts, chiral intermediates and bespoke synthesis hold important process IP. These companies are frequently acquisition targets because they can compress cost and complexity for larger formulators.

Research-reagent and niche suppliers — Providers servicing academic, preclinical and diagnostic markets maintain higher-margin, lower-volume lines and are less sensitive to commodity-cycle volatility but can be a bellwether for innovation trends.

Formulators and device integrators — Companies that combine prostaglandin analogues with delivery systems (eye drops, implants, combination drops) are increasingly capturing downstream value through new reimbursement codes and lifecycle extensions.

In the full report, PW Consulting profiles leading names across these roles, assessing manufacturing scale, regulatory track record, commercial channels and M&A appetite. That profiling underpins practical options for partnerships or procurement change.

Regulatory approvals & product launches — Recent approvals and new glaucoma product launches strengthen the clinical and commercial rationale for prostaglandin-based ophthalmic therapeutics. These events create incremental demand pockets and justify investment in downstream formulation capacity.

Biosynthetic production breakthroughs — Published demonstrations of microbial routes for prostaglandin production mark an inflection in unit-cost economics. Early movers stand to benefit through licensing or captive production; late movers risk margin pressure in API markets.

Regulatory and trade actions — Expanded tariff coverage and new chemical-safety opinions have direct P&L implications: landed-cost increases, reformulation mandates and potential shelf-stock write-offs. Procurement and regulatory teams must now be tightly coupled in scenario planning.

De-risk supply through diversified sourcing and inventory design — Implement dual-sourcing where feasible, negotiate prioritized capacity with strategic API producers, and model economic tradeoffs for regional buffer inventories versus just-in-time procurement.

Build a regulatory hedging function — Establish a cross-functional rapid-response team to interpret chemical-safety opinions, tariff changes and reimbursement shifts so product and go-to-market plans can be adjusted within months rather than quarters.

Prioritize higher-value downstream plays — Given reimbursement tailwinds for procedure-based ophthalmic therapies and device-drug combinations, consider shifting R&D and commercial investment downstream where margins and stickiness are greater.

Evaluate biosynthesis and licensing options now — Conduct technology scouting and early-stage partnering; running co-development pilots can secure optionality without committing to full-scale capex.

Use competitive concentration to your advantage — For purchasers, consolidated supplier bases can be leveraged for long-term supply agreements; for entrants, identify narrow capability gaps among incumbents to win share through niche differentiation.

Prepare M&A and JV playbooks — Targeted acquisitions of intermediates players, specialty formulators or biosynthesis start-ups can accelerate strategic objectives. PW Consulting’s report includes valuation sensitivity tables and integration risk checklists to guide transaction teams.

Our full Prostaglandin Market research is structured to convert insight into executable decisions. Deliverables include an editable Excel forecast model, supplier heatmaps, regulatory impact assessments, and tailored scenario workshops. For clients pursuing supply diversification or M&A, we offer end-to-end diligence and negotiation support informed by primary-sourced price curves and production-capacity insights.

This preview intentionally showcases the analytical frameworks, strategic implications, and headline macro metrics that matter for 2026 planning while withholding the detailed regional/application split tables and raw-model outputs that are proprietary to the full report. That granular data—critical for procurement tenders, valuation workstreams, and regulatory compliance planning—is available as part of the paid research package and bespoke advisory engagements.

For immediate next steps: if your 2026 plan depends on uninterrupted API supply, expanding ophthalmic portfolios, or evaluating biosynthetic options, PW Consulting can deliver a condensed rapid-assessment within two weeks or a full strategic engagement to operationalize the imperatives above.

For detailed analysis of this topic, please visit the official page:Prostaglandin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com