Hydrogen Fuel Cell Gas Diffusion Layer Market — Strategic Briefing for 2026 Decision-Makers

Executive trailer

As hydrogen mobility and stationary fuel cell deployments accelerate, the gas diffusion layer (GDL) — long an underappreciated component — is becoming a strategic locus for cost, performance, and supply-chain advantage. PW Consulting’s latest market research synthesizes historical performance and a forward-looking forecast to equip executives in 2026 with the clarity needed to set procurement, R&D, and M&A priorities. This briefing highlights the study’s strategic value, key dynamics shaping supplier economics, and the actionable use-cases executives should prioritize. For full segment tables, supplier scorecards, and scenario-modeled demand curves, please consult the full report on our website.

Hydrogen Fuel Cell Gas Diffusion Layer Market

Market snapshot — growth trajectory and what it means

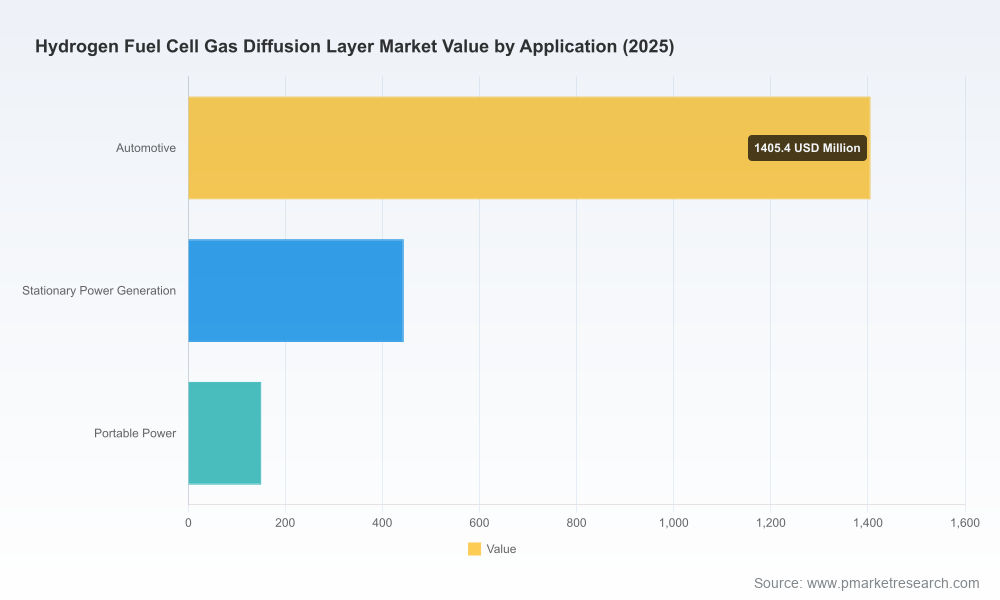

The hydrogen fuel cell GDL market has moved from niche to scale at pace. Our analysis shows the market expanding from roughly USD 700 million in 2020 to approximately USD 2,000 million in 2025 — a near threefold increase in five years. We project continued rapid expansion through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 13.18%, reaching an estimated USD 4,000 million by 2032. This growth is being driven by rising fuel cell vehicle programs, broader adoption of stationary power installations, and upstream electrification strategies that leverage PEM fuel cell stacks and water electrolyzers.

Hydrogen Fuel Cell Gas Diffusion Layer Market

For 2026 corporate planning, the implication is straightforward: GDL procurement, qualification, and supply-chain resilience are no longer back-office activities. They must be treated as strategic levers that influence unit cost, stack durability, and time-to-market.

Hydrogen Fuel Cell Gas Diffusion Layer Market

Why this research matters for 2026 decisions

- Timing of investments: The forecasted acceleration implies earliest-mover advantages for players that secure capacity, vertically integrate critical inputs, or lock favorable long-term contracts in 2026.

- Supplier selection under uncertainty: With the supplier landscape exhibiting measurable concentration, buyers must balance technical fit and commercial resilience. Our report provides a supplier risk matrix that goes beyond brand—assessing capacity flex, geographic exposure, and material substitution readiness.

- R&D and materials strategy: Developments in fluorine-free hydrophobic treatments and recycled carbon feedstocks are changing the technical trade-offs between cost, durability, and environmental compliance. Companies that align material science roadmaps to regulatory trends will capture margin and market share.

- M&A and JV prioritization: The combination of strong market growth and moderate concentration presents clear roll-up and partnership opportunities. Our scenario analysis identifies target profiles most likely to deliver scale or technological differentiation in a 24–36 month horizon.

Key market dynamics — risks and opportunities

- Supply chain friction and geopolitics: Ongoing US–China trade constraints and evolving EU trade policies introduce volatility into raw material flows and component sourcing. The report includes stress-tested supply-chain scenarios and mitigation playbooks for sourcing, dual-sourcing, and inventory hedging.

- Material innovation: Historically, GDLs have relied on carbon fiber substrates treated with perfluorinated hydrophobic agents (e.g., PTFE). Emerging alternatives — such as fluorine-free hydrophobic networks combining graphene, cellulose, and modified polypropylene — promise lower regulatory risk and potentially materially different cost/performance profiles. We quantify the SWITCH points where non-fluorinated GDLs become commercially attractive under varying carbon pricing and regulatory regimes.

- Circularity and feedstock substitution: Suppliers are starting to pilot recycled carbon fiber feedstocks and graphitized substrates, both to lower embodied carbon and to reduce raw material exposure. Our field-level cost models and LCA comparators help R&D and procurement teams weigh trade-offs between performance degradation risk and sustainability premiums.

- Concentration and industrial structure: The market demonstrates moderate concentration; a handful of established suppliers command a substantial share of volume and technology leadership. That creates both a barrier for new entrants on the high-performance side and an opening for niche players focused on cost-optimized or specialty GDLs.

Competitive landscape — who to watch and why

The vendor matrix in our research evaluates technical capabilities, manufacturing footprints, product portfolios (carbon paper, carbon cloth, mesh-based and molded substrates), service capabilities, and strategic intent. Below are high-level profiles of core incumbents included in the study; the full supplier scorecards, including strengths/weaknesses and sourcing risk indices, are reserved for the full report.

- SGL Carbon (Germany) — A leader in treated carbon paper and cloth GDL technologies. Noteworthy for recent pilots using recycled carbon fibers aimed at reducing raw material waste by up to 40% and improving sustainability credentials.

- Toray Industries (Japan) — Large-scale carbon paper producer with a strong presence in both fuel cell and electrolyzer applications; active in industry showcases where product readiness and industrial partnerships are highlighted.

- Freudenberg Group (Germany) — Offers an integrated portfolio spanning carbon cloth and paper GDLs, with strengths in process engineering and close collaboration with stack integrators.

- AvCarb (USA) & Caplinq (USA) — North American players providing carbon cloth and specialized carbon paper grades; positioned to serve regional OEM programs and defense/aviation niche markets.

- Technical Fibre Products (UK), Mitsubishi Chemical (Japan), Mott Corporation (USA), GKD (Germany) — Each brings differentiated technologies (carbon fiber felts, polymer-based substrates, porous metal/mesh GDLs) that map to distinct application needs.

Recent developments we track include capacity expansions, trade-show product launches, and sustainability pilots. These moves are signals of where incumbent players expect demand to concentrate and where they intend to invest in downstream integration.

Report contents — practical outputs for executives

The full PW Consulting study is built to be operational. It does not merely describe the market; it equips teams to act. Deliverables include:

- Demand-model templates and revenue forecasts (2026–2032) with scenario toggles for policy, vehicle adoption, and electrolyzer build-out.

- Supplier scorecards and a procurement playbook for qualification timelines, costing benchmarks, and contractual clauses that mitigate performance-cliff risk.

- Unit-cost and LCOH-style analyses that separate material, processing, and treatment contributions to stack-level economics.

- Supply-chain maps that overlay geographic risks, critical raw-material exposures, and suggested dual-sourcing corridors.

- Commercial models for JV/M&A screening and an M&A valuation framework calibrated to GDL manufacturing economics and EPC timelines.

Strategic playbook for 2026 — five concrete moves

- Lock near-term capacity, but with flexibility: Negotiate supply contracts with staged volumes and capacity options tied to performance milestones to avoid overcommitment if a technology pivot occurs.

- Invest in material-agnostic test infrastructure: Given the material innovation wave (e.g., fluorine-free GDLs), buyers should qualify across substrate families to reduce single-source risk.

- Pursue targeted partnerships: Seek manufacturing JVs or tolling agreements with suppliers piloting recycled-carbon feedstocks to gain early access to lower-carbon, potentially lower-cost inputs.

- Embed regulatory scenario planning: Incorporate likely EU green-energy directives and potential trade-barrier outcomes into procurement and localization strategies to avoid last-minute tariff shocks.

- Prepare the M&A shortlist: Use our triage criteria (technical differentiation, local market access, capacity scalability) to identify bolt-on acquisition targets that accelerate time-to-volume.

How to use this research in 90–180 day planning cycles

Executives can convert our insights into short-term action: prioritize supplier audits and qualification runs for 2026 production ramps; deploy our stress-tested inventory policies to cover critical windows of trade friction; and integrate the LCA comparators into sustainability-driven procurement to satisfy OEM and public-sector tenders. Our interactive models allow procurement, product, and corporate development teams to quantify the P&L and balance-sheet impact of alternative sourcing and material strategies within days.

Conclusion — why PW Consulting’s coverage is mission-critical

In 2026, decisions made around the humble GDL will have outsized effects on cost of ownership, stack reliability, and time-to-market. With the market roughly tripling between 2020 and 2025 and forecasted to grow at a 13.18% CAGR through 2032, the window for securing strategic advantage is narrow. PW Consulting’s Hydrogen Fuel Cell Gas Diffusion Layer Market study translates that market momentum into executable plans—without exposing every tactical datapoint in this preview. For the granular segment tables, supplier index, and bespoke modeling tools that will inform contracts and capital allocation this year, please access the full report on our website.

For detailed analysis of this topic, please visit the official page:Hydrogen Fuel Cell Gas Diffusion Layer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com