Forging Presses Market 2026: Strategic Preview for Executive Decision-Making

Executive summary

As companies plan capital allocation and operational strategies for 2026, the forging presses market presents a blend of steady growth, technology-driven disruption, and concentrated supplier dynamics. Our analysis at PW Consulting places the market on a trajectory that reflects both cyclical manufacturing demand and long-term modernization: a compound annual growth rate (CAGR) of 4.3% across our forecast horizon, with the global market expanding from a mid‑three‑figure base in 2020 to broadly exceed two‑hundred in 2025 (USD, Million), and continuing to rise toward the upper end of the forecast by 2032. These headline figures underscore a market that is large enough to warrant strategic investment yet sufficiently segmented to reward targeted approaches in product, geography, and technology.

Forging Presses Market

Market snapshot and why 2026 matters

The forging presses market has outpaced several adjacent heavy‑machinery segments through 2025, driven by renewed OEM activity in automotive and aerospace, infrastructural projects, and replacement cycles for older press fleets. Importantly for 2026 decisions, the market is now at an inflection point where energy efficiency requirements, automation adoption, and evolving raw‑material dynamics converge—creating windows for first‑mover advantage in both product offerings and retrofit services.

Forging Presses Market

- Growth trend: The market expanded materially between 2020 and 2025 and the growth momentum continues into the 2026–2032 forecast period at a mid‑single‑digit CAGR (4.3%).

- Consolidation and concentration: Market concentration is meaningful at the top, with the three‑player and five‑player concentration ratios indicating that leading OEMs hold a sizeable share—yet not to the extent that innovation is closed to challengers.

- Technology vector: Energy‑saving hybrid and servo‑driven architectures are transitioning from niche to mainstream, driven by regulatory mandates and clear TCO (total cost of ownership) benefits.

Strategic implications for 2026 corporate planning

Executives should treat 2026 as a planning year to align capital investments with three interlocking priorities: decarbonization/compliance, automation for labor resilience, and selective capacity build‑out near high‑growth submarkets. These priorities translate into concrete strategic options:

Forging Presses Market

- CapEx reallocation toward energy‑efficient presses and retrofit kits. With regulatory frameworks increasingly specifying energy‑performance thresholds (requiring in many cases 22–35% reduction versus conventional systems), press buyers must evaluate lifecycle energy consumption alongside nominal tonnage and stroke capability (German Industrial Association, VDMA, 2024).

- Investment in automation and digital controls. Labor shortages and skills mismatches in the forging sector are accelerating adoption of advanced PLCs, robotics for material handling, and digital process controls—measures that reduce headcount dependency and increase throughput consistency (US Department of Energy, 2022).

- Service and retrofit business models. As fleets age, opportunities arise for aftermarket players who can deliver energy‑saving retrofits, condition monitoring, and predictive maintenance contracts—high margin, recurring revenue streams that de‑risk OEM exposure to cyclical OEM equipment sales.

- Selective vertical and geographic positioning. While we do not disclose detailed subsegment shares here, the report identifies attractive application pockets where higher ASPs and longer equipment lifecycles justify differentiated product strategies, including hybrid hydraulic‑electric solutions and high‑speed mechanical presses for high‑volume forging.

What PW Consulting’s Forging Presses Market report contains

Our full report is designed to move decision‑makers from insight to action. It blends rigorous market modeling with practical tools for procurement, product strategy, and M&A screening. Key deliverables include:

- Market model and forecast (2026–2032) built on bottom‑up shipment, installed‑base replacement, and macro‑demand drivers. The model is granular enough for scenario testing but accessible for boardroom discussions.

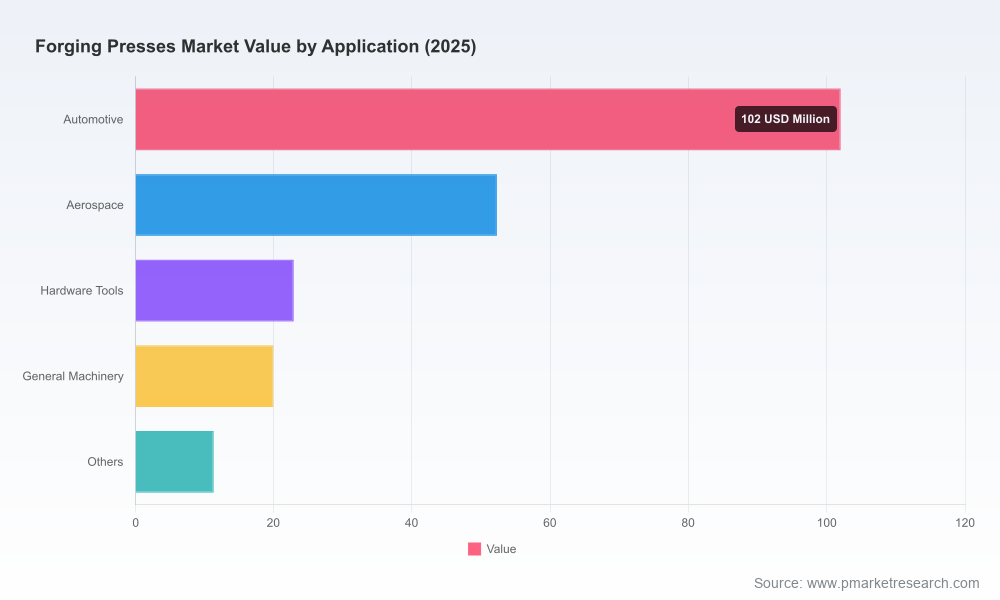

- Demand drivers and end‑use analysis, covering automotive, aerospace, industrial machinery, and specialty forging applications—articulating unit economics and replacement cycles without divulging full segment tables in this preview.

- Detailed supplier landscape with profiles, capability matrices, and go‑to‑market assessments for major OEMs and niche specialists. Profiles assess technology maturity, service footprint, and partnership potential.

- Technology deep dives into hydraulic, mechanical, servo, and hybrid architectures, including energy recovery systems and advanced control stacks. We quantify TCO tradeoffs and provide decision frameworks for OEMs and end users.

- Regulatory and raw material risk analysis. This includes impact matrices for energy efficiency mandates and raw‑material composition exposures—highlighting that carbon steel remains a significant input in forging supply chains (industry market data, 2025).

- Commercial playbooks: procurement checklists, retrofit decision trees, and an investment prioritization matrix tailored for CxOs evaluating new press purchases versus retrofits.

- M&A and partnership screening tools: threshold criteria, synergies mapping, and a short list of strategic targets—structured to enable rapid deal screening by 2026 transaction teams.

Competitive landscape: who matters and why

The competitive field mixes specialized builders with diversified heavy‑equipment conglomerates. The market leaders combine deep engineering heritage, service networks, and rising investments in energy‑efficient and automated systems. PW Consulting’s review of principal participants yields several actionable takeaways for 2026:

- Technology leaders and system integrators: Companies such as Schuler (ANDRITZ Schuler) and SMS Group are notable for delivering advanced hydraulic, hybrid and automation‑integrated presses. Recent deployments demonstrate the real‑world energy and throughput gains operators can expect—Schuler’s hybrid delivery to an OEM facility in late 2025 reporting energy reductions in the high‑teens to low‑30s percent range, for example.

- High‑volume mechanical expertise: AIDA Engineering remains relevant where mechanical and servo presses are needed for high‑throughput, precision production. Their product architecture continues to be chosen by customers seeking low cycle time per part.

- Custom hydraulic and niche suppliers: US‑based specialists (e.g., Beckwood Press Company, Ajax‑Ceco, Macrodyne) retain strong positions in bespoke and large‑tonnage hydraulic solutions. Their flexibility and application engineering capabilities make them preferred partners for heavy‑duty and specialty forging projects.

- Regional and component specialists: A set of domestic providers and component suppliers support local markets and OEM aftersales—forming attractive partnership candidates for global OEMs seeking to broaden service coverage or reduce lead times.

Recent industry events underscore the pace of technological shifts: in 2025 and early 2026, major OEMs announced deliveries and commissioning of large hybrid and high‑speed presses, while trade shows continued to concentrate mindshare around energy recovery and automation (sources: Maxiforja Group, Schuler AG, SMS Group, 2025–2026).

Technology, raw materials, and regulatory dynamics

Three systemic forces will shape supplier viability and buyer economics through 2026:

- Energy efficiency and emissions governance. Regulatory expectations and customer procurement specifications increasingly require presses to achieve significant energy reductions versus legacy designs—mandates and buyer requirements commonly target reductions in the range of approximately 22–35% (VDMA, 2024). This accelerates demand for hybrid architectures and kinetic energy recovery systems.

- Raw material composition and sourcing. Carbon steel continues to be a leading raw material in the forging industry due to its cost‑performance profile—its dominance in the feedstock mix has implications for material handling standards, die life, and maintenance cycles (Industry Market Data, 2025).

- Labor pressure and automation. Ongoing labor shortages are incentivizing automation, digitalization, and remote‑monitoring solutions. Firms investing early in integrated process controls gain both productivity and hiring flexibility advantages (US DOE, 2022).

How to use this preview and next steps

This preview is intended to guide strategic conversations ahead of major 2026 procurement cycles and capital budgeting rounds. PW Consulting recommends three practical next steps for executives preparing for the year:

- Commission a tailored TCO analysis for your press fleet. Use lifecycle energy and service costs to compare retrofit vs. replacement under your regional regulatory baseline.

- Run a supplier stress‑test. Evaluate top existing suppliers against energy‑efficiency capability, automation integration, and aftersales footprint; identify gaps that could be filled via partnerships or acquisitions.

- Outline an automation roadmap. Pilot one or two digital upgrades (e.g., condition monitoring and automated material handling) in 2026 to de‑risk wider rollouts by 2028.

Invitation to access the full intelligence

PW Consulting’s full Forging Presses Market report contains the granular models, supplier scorecards, and executable playbooks needed to operationalize the strategies outlined above. To preserve the strategic value of the research for subscribers, we have withheld detailed segmentation tables and certain proprietary data from this preview. Readers seeking the complete datasets, downloadable models, and vendor comparative matrices are invited to visit our publication page or contact PW Consulting’s industry practice for an executive briefing and bespoke implementation support.

For teams planning capital allocations, strategic sourcing, or M&A in 2026, an informed, quantified approach to energy efficiency, automation, and aftermarket monetization will be decisive. PW Consulting’s report is structured to convert those insights into tangible boardroom decisions and measurable ROI pathways.

For detailed analysis of this topic, please visit the official page:Forging Presses Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com