Step-by-Step Guide to Ordering Labubu Dolls in Germany

Other |

2026-06-06 14:23:38

As manufacturers and brand owners push to eliminate defects, comply with tighter regulation, and accelerate automation, the print quality inspection system market has moved from niche optimization to a strategic infrastructure play. Our market model shows an established multi-year upswing: the market expanded from approximately USD 148.5 million in 2020 to about USD 201.5 million in 2025 and is projected to reach roughly USD 300.0 million by 2032, implying a mid-single-digit compound annual growth (CAGR ~5.8%) over the forecast window. That trajectory reflects persistent demand for closed-loop quality control in packaging, labels, and regulated sectors, and it frames the strategic choices organizations face in 2026.

Print Quality Inspection System Market

Investment timing: Buyers must decide whether to retrofit existing lines or invest in next‑generation in‑line systems that embed AI and cloud connectivity. Capital allocation decisions hinge on realistic growth and ROI assumptions; our modeling translates market trajectory into deployment scenarios that align with payback horizons common in manufacturing.

Print Quality Inspection System Market

Regulatory alignment: New and updated quality regulations — including the Quality Management System Regulation (QMSR) that amended device CGMP requirements in early 2026 and the widespread use of ISO standards in manufacturing — are shifting procurement from “nice-to-have” to “must-have” for regulated product lines. Our study quantifies the regulatory uplift to demand and outlines compliance pathways tied to inspection architecture choices.

Print Quality Inspection System Market

M&A and partnership signals: Consolidation activity and technology-focused tuck-ins are accelerating. Buyers, investors, and strategic partners need a clear map of capability adjacencies to prioritize targets and avoid paying a premium for commoditized features.

The market’s historic performance (2020–2025) demonstrates steady expansion, with an observable acceleration as manufacturers address labor shortages and seek waste reduction. Our forecast to 2032 incorporates automation adoption curves, differential product replacement cycles (in‑line vs. off‑line architectures), and incremental value from AI and cloud services. The resulting growth profile supports a thesis where smart inspection becomes embedded in digital operations rather than remaining a bolt-on instrument.

For corporate strategists this translates to three practical imperatives: prioritize modular architectures that can be upgraded as AI capabilities evolve; plan CAPEX with an eye to obsolescence risk on line-scan camera modules; and build cross-functional procurement criteria that reward measurable defect reduction and regulatory traceability rather than feature lists alone.

AI-first inspection engines — moving from rule-based to probabilistic models — are raising detection rates while lowering false rejects. Vendors are differentiating on model training data and inference latency as much as on optics.

Cloud-enabled prepress and analytics platforms decouple software value from hardware lifecycle. Recent product releases and software launches demonstrate an industry pivot to SaaS-enabled inspection workflows and remote verification.

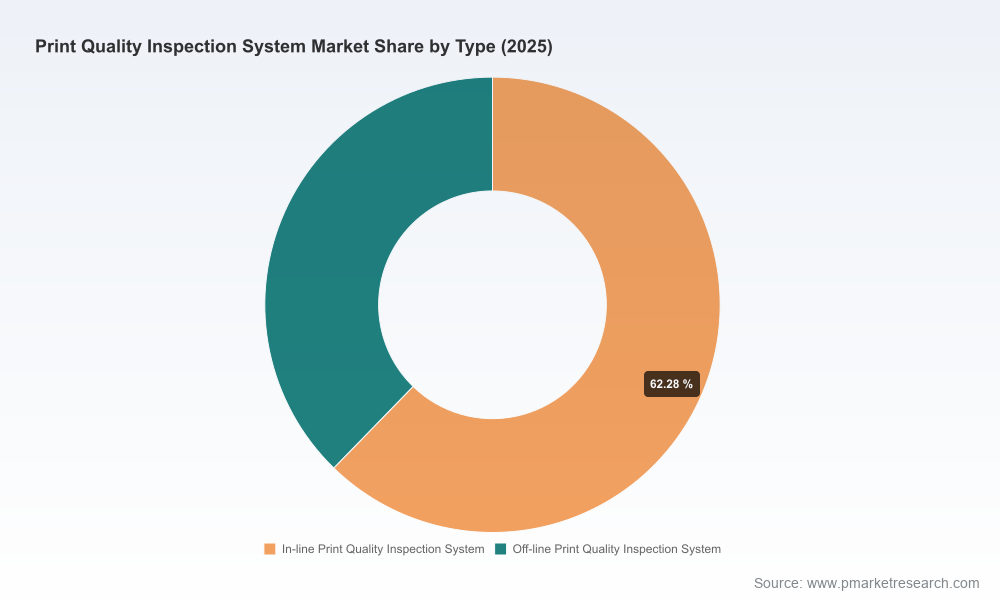

Line-scan imaging modules remain the single largest technical constraint: high-speed optics, illumination, and data throughput demand significant upfront investment and floor-space considerations. This continues to be the main barrier for rapid, wide-scale retrofit deployment in legacy plants.

Three external forces are shaping demand in 2026:

Regulatory tightening: The QMSR update (Feb 2026) and continued application of ISO quality frameworks require traceability and auditable quality evidence for many packaging and medical labeling applications. Systems that facilitate documented audit trails and integrate with QMS platforms become procurement differentiators.

Labor dynamics: Persistent labor shortages and rising operator costs increase the business case for automation. Our scenario analysis links labor-driven automation demand to improved unit economics for inspection deployments across mid- to large-scale lines.

Capital and infrastructure constraints: The high capital intensity of high-speed inspection hardware and the need for plant-level infrastructure upgrades slow adoption in price-sensitive segments. Financing, leasing, and outcome-based procurement models are emerging as practical responses.

The vendor ecosystem is diverse and moderately unconcentrated — market leadership is distributed across specialist hardware firms, machine-vision incumbents, and software-first entrants. Below are synthesized strategic profiles of key players and their implications for buyers and partners.

EyeC GmbH (Hamburg, Germany) — Strength: specialty in prepress and packaging inspection with a strong product suite. Strategic momentum: recent move into cloud-based prepress inspection software signals an intent to capture recurring revenue and decouple software value from hardware. Implication: buyers should evaluate EyeC when prioritizing prepress-to-press digital workflows and when requiring vendor support for software-centric rollout strategies.

AVT Inc. (Kfar Saba, Israel) — Strength: real-time color and defect detection systems for labels and flexible packaging. Strategic momentum: corporate restructuring following acquisition in 2025 positions AVT to invest in product focus and market expansion. Implication: potential partner or acquisition target for companies seeking mature, real‑time inspection algorithms in packaging lines.

LUSTER (China) — Strength: aggressive AI-enabled product launches and high-speed systems tailored to cost-sensitive markets. Strategic momentum: product announcements at major trade shows point to rapid product development cycles. Implication: consider LUSTER for competitive pricing and fast time-to-deploy projects, especially in high-volume packaging operations where throughput is prioritized.

Procemex (Finland) — Strength: strong web-monitoring heritage for paper, pulp, and converting industries. Strategic momentum: active trade-show demonstrations of web inspection systems reveal focus on surface-defect analytics. Implication: ideal for operations where continuous web monitoring and surface-quality analytics are core requirements.

Erhardt+Leimer (Germany), Nireco (Japan), Futec (Japan), Baldwin Vision Systems (US) — Strengths: system integration, tension control, and high-speed specialization. Implication: favored where mechanical integration, line-speed stability, and local service networks are determinative.

Lake Image Systems (UK), Esko (Belgium), Omron/Microscan (US), Cognex (US) — Strengths: software-rich solutions, prepress automation, and broad machine-vision portfolios. Implication: these vendors are attractive when buyers need tight integration between artwork verification, regulatory compliance use-cases, and enterprise vision systems.

AVT’s 2025 ownership change signals renewed capital and strategic focus on inspection solutions — expect accelerated product development or market expansion initiatives.

LUSTER’s 2025 launch of a next‑generation AI inspection system underscores supplier competition on model accuracy and throughput.

EyeC’s 2026 release of cloud-based prepress software reflects a broader industry shift to software-first value capture and recurring revenues.

Procemex’s active presence at industry events in 2026 highlights continued demand in paper and converting verticals for specialized web-monitoring solutions.

Our report goes beyond directional commentary to provide operational tools and frameworks for 2026 decision-making, including:

Scenario-based demand models calibrated to historical 2020–2025 data and our 2026–2032 forecasts;

Vendor scorecards and capability matrices that map features to measurable outcomes (defect reduction, scrap avoidance, regulatory traceability);

Procurement playbooks with RFP templates, evaluation scoring, and total cost of ownership (TCO) templates tailored to retrofit vs. greenfield deployments;

Technology roadmaps showing upgrade paths for optics, edge compute, and cloud analytics to protect hardware investments;

Regulatory impact assessments aligned to QMSR, ISO standards, and FDA/EMA expectations for pharmaceutical and medical packaging;

Case studies and primary interviews that reveal real-world paybacks, installation pitfalls, and organizational change requirements.

For CEOs and CFOs: align CAPEX envelopes with a phased deployment plan that ties expenditure to measurable yield and compliance benefits. Use our ROI scenarios to stress-test budgets under different labor‑cost and regulation scenarios.

For COOs and plant leaders: prioritize pilot lines where defect cost per part and regulatory risk are highest; require vendors to commit to measurable KPIs during proof-of-concept stages.

For CTOs and procurement leads: favor vendors demonstrating modularity, clear upgrade paths, and open APIs for integration into MES and QMS systems. Assess the division of value between hardware, software, and services when negotiating commercial terms.

This briefing intentionally highlights strategic conclusions and synthesis without reproducing the granular segmentation tables and region/application breakdowns that underlie our models. The full report contains detailed segment-by-segment forecasts, vendor benchmarking spreadsheets, and downloadable TCO calculators that support procurement negotiations and capital planning exercises. If you are preparing an investment thesis, negotiating vendor contracts, or designing an enterprise-wide inspection rollout, the full dataset and appendices are essential.

Use this briefing to align leadership around the strategic importance of print quality inspection systems in 2026. Then, access the full PW Consulting Print Quality Inspection System Market study for the empirical inputs, vendor scorecards, and executable playbooks necessary to convert strategy into on-the-floor results. Our proprietary models and interviews will save weeks of internal analysis and materially reduce execution risk.

For detailed analysis of this topic, please visit the official page:Print Quality Inspection System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com