Nitrogen Gas Springs Market — Strategic Outlook for 2026 Decision-Makers

Executive snapshot

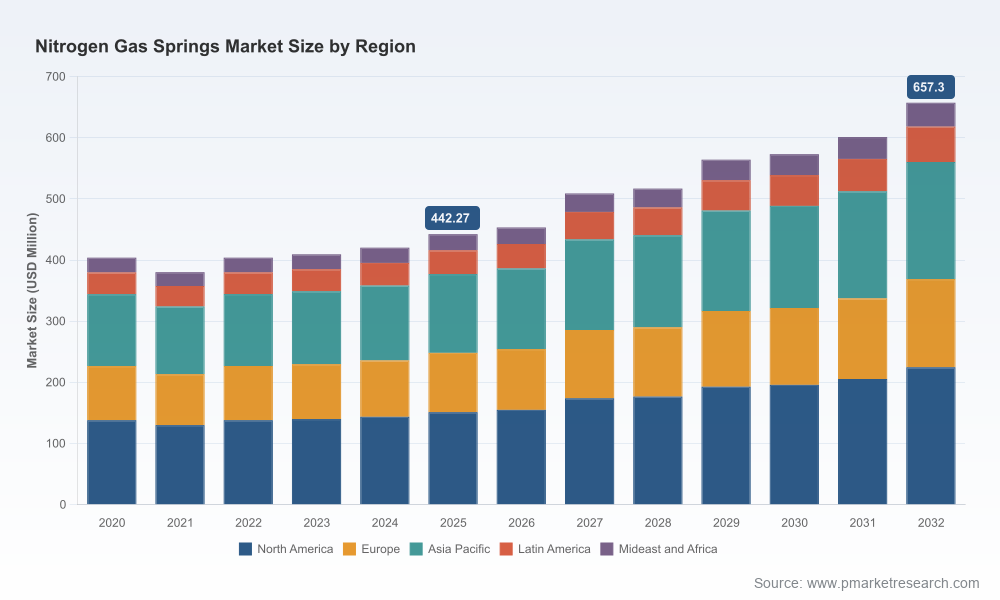

PW Consulting’s latest study on the Nitrogen Gas Springs market (base year 2025, forecast 2026–2032) frames a market in steady recovery and structural expansion. After a modest trough in the early 2020s, global revenues rose to approximately USD 442.3 Million in 2025 and are projected to reach roughly USD 657.3 Million by 2032, representing a compound annual growth rate (CAGR) of about 5.7% across the forecast window. Market concentration remains moderate: the top three suppliers account for under half of industry revenue, and the top five for just under half-plus—conditions that both enable niche differentiation and preserve room for strategic consolidation.

Nitrogen Gas Springs Market

Why this research matters for corporate strategy in 2026

- Translate macro growth into executable targets: the report converts the headline CAGR into revenue scenarios and stress-tested pathways for procurement, R&D and sales planning in 2026–2027.

- Prioritize capital allocation intelligently: it highlights where incremental capex and product investments are likely to yield the highest ROI given tooling cycles, OEM procurement rhythms, and aftermarket lifetime economics.

- De-risk supply chains: the analysis identifies the levers to mitigate raw-material shocks (notably steel) and certification bottlenecks that can delay market entry in critical geographies.

- Inform M&A and partnering: the market structure and vendor capability maps surface acquisition targets and JV profiles for scale, technology or geographic entry.

Market trajectory: what the numbers imply for 2026 planning

The market’s rebound from the early-2020s deployment cycle to a mid-decade base of roughly USD 442 Million creates a pragmatic foundation for near-term investment. Our forecast shows 2026 as a transitional year—continuing growth but with heterogeneous demand across end-use segments. The projected climb to about USD 657 Million by 2032 implies sustained demand for higher-performance variants, digitalization of lifecycle services and differentiated aftermarket offerings. For boardrooms and strategy teams, the implication is clear: scale and sophistication will be rewarded, but only if matched by agility in sourcing and compliance.

Nitrogen Gas Springs Market

Competitive landscape — who is shaping the market and how

The industry is characterized by a blend of specialized manufacturers and established tooling component suppliers. Three facts matter for strategic positioning:

Nitrogen Gas Springs Market

- Innovation hubs are shifting beyond simple force/cylinder variants toward systems that combine mechanical performance with safety and data transparency.

- Specialization remains valuable—companies that serve high-temperature or heavily contaminated environments command engineering premiums.

- Logistics and catalog breadth are competitive differentiators for industrial customers seeking same-day or short-lead replacements.

Representative vendor dynamics observed in the market review:

- DADCO Inc. — moving upstream with IoT-enabled springs that integrate pressure and temperature sensing, targeting Industry 4.0 die tooling customers and OEMs seeking predictive maintenance pathways.

- Special Springs s.r.l. — focused on in-house manufacturing, safety accessories and interchangeability solutions that reduce downtime in heavy stamping environments; active catalog expansion and aftermarket support strengthen their service footprint.

- Hyson Products Inc. — reinforces its position on application breadth (metal stamping, injection molding) with high-force and contamination-resistant variants aimed at long-run tooling operations.

- Pascal Engineering, KALLER (Strömsholmen AB), Bordignon and peers — emphasize high-quality, application-specific engineering (including high-temperature and long-life designs) that appeal to premium tooling customers.

- Isotech, Gemini, AZOLGAS and FIBRO — combine material variants, localized manufacturing and deep catalog availability to win on reliability and delivery.

Recent product launches and catalog updates (early 2025–late 2025) demonstrate the market’s technology vectors: embedded monitoring, contamination mitigation accessories, systemized trade-show kits and catalog consolidations. These moves validate two strategic hypotheses: first, aftermarket value capture through service and data is an emergent margin pool; second, product differentiation through safety and environmental robustness is a sustainable defense against commoditization.

Regulatory and materials context that will shape 2026 outcomes

- Standards and safety: ISO 11901 series and national/regional standards (including PED requirements for European machinery and mounting standards such as VDI/CNOMO) define permissible designs and dimensional interoperability. Compliance timelines must be integrated into product development and market-entry plans.

- Charging gas neutrality: regulatory and standards guidance require nitrogen (commercial grade, specified purity) as the only charging gas—this constrains substitution opportunities while enabling quality-based differentiation.

- Raw material volatility: steel price fluctuations driven by supply chain disruptions and geopolitical pressure materially affect cost structures. Hedging, dual-sourcing and design-to-cost initiatives are necessary near-term actions to preserve margins.

- Operational certification: PED, ISO and local machinery directives require careful product documentation and testing; firms without structured regulatory roadmaps face delayed access to key European and international customers.

What the full PW Consulting report contains (practical, actionable deliverables)

Designed as a decision-use tool for executives, procurement leads and product teams, the full study couples market-sizing with actionable modules:

- Proprietary market model (base year 2025, 2026–2032 forecast) including revenue scenarios, sensitivity to raw-material cost and demand shocks.

- Segment playbooks (by type, application and region) that translate market trends into go-to-market priorities and KPIs — note: detailed segment-level figures and split tables are reserved for the full report.

- Vendor maps and capability matrices (product portfolios, service models, IP and manufacturing footprint) with suggested partnership and M&A targets by strategic priority.

- Supply-chain risk register and mitigation playbook focused on steel procurement, nitrogen logistics and critical-component lead times.

- Regulatory roadmap covering ISO, PED and regional mounting standards, with a compliance checklist for product launch in target markets.

- Technology and services roadmap identifying digital retrofit opportunities (sensing, remote diagnostics), high-temperature materials and contamination-resistant architectures.

- Commercial toolkits: pricing model templates, after-sales service monetization pathways, and procurement negotiation levers tuned to 2026 supplier dynamics.

- Scenario planning and stress tests — demand shock, price shock and regulatory shock scenarios with recommended tactical responses and contingency triggers.

How to use these insights for 2026 decisions (recommended actions)

- Procurement: shift from single-source to dual-sourcing for key alloys; lock-in shorter-term hedges for steel and build volumetric flexibility clauses with suppliers.

- Product development: prioritize two tracks — (a) differentiated high-value variants (high-temp, contamination-resistant, safety-enhanced), and (b) modular retrofits for IoT-enabled monitoring to capture aftermarket service revenue.

- M&A and partnerships: screen small but technologically complementary vendors (sensor integration, high-temp materials) to accelerate time-to-market for digitalized solutions.

- Regulatory readiness: invest in a compliance playbook for PED and ISO standards now to avoid multi-month approvals that can derail 2026 OEM sourcing cycles.

- Aftermarket & services: develop subscription-priced predictive maintenance offers tied to sensor data; this can materially lift lifetime margins as the installed base scales.

- Commercial alignment: reposition sales incentives and distributor agreements to prioritize uptime-critical customers and to monetize rapid-replacement catalogs and same-day logistics where possible.

Final note — the value of the full intelligence

This briefing outlines the strategic opportunities and risks shaping 2026 decisions in the Nitrogen Gas Springs market: sustainable growth at a mid-single-digit CAGR, a moderately concentrated supplier base, accelerating technology and regulatory complexity, and clear margin opportunities in differentiated products and aftermarket services. For teams preparing procurement cycles, capex plans or M&A mandates in 2026, the full PW Consulting report provides the granular segment-level data, vendor scorecards, modeled scenarios and downloadable financial templates necessary to move from strategy to execution. Detailed segment tables, pricing worksheets, and the full vendor profiles are held within the report and accompanying data pack—contact our publications page to access the complete dossier and the interactive model.

For detailed analysis of this topic, please visit the official page:Nitrogen Gas Springs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com