Thermal Barrier Coatings (TBC) Market — Strategic Imperatives for 2026

Executive preview

As senior strategists at PW Consulting, we view the Thermal Barrier Coatings (TBC) market through the lens of near‑term operational choice and multi‑year strategic positioning. Our 2026 briefing synthesizes market sizing, competitive dynamics, technology inflection points, and regulatory pressure to deliver pragmatic options for CEOs, heads of strategy, supply‑chain leaders and M&A teams. This piece is a high‑signal preview — built to demonstrate analytical depth and the type of executable insight contained in our full report — while reserving detailed segment tables and granular regional/application splits for clients who access the complete intelligence.

Thermal Barrier Coatings (TBC) Market

Market snapshot (what the numbers tell you)

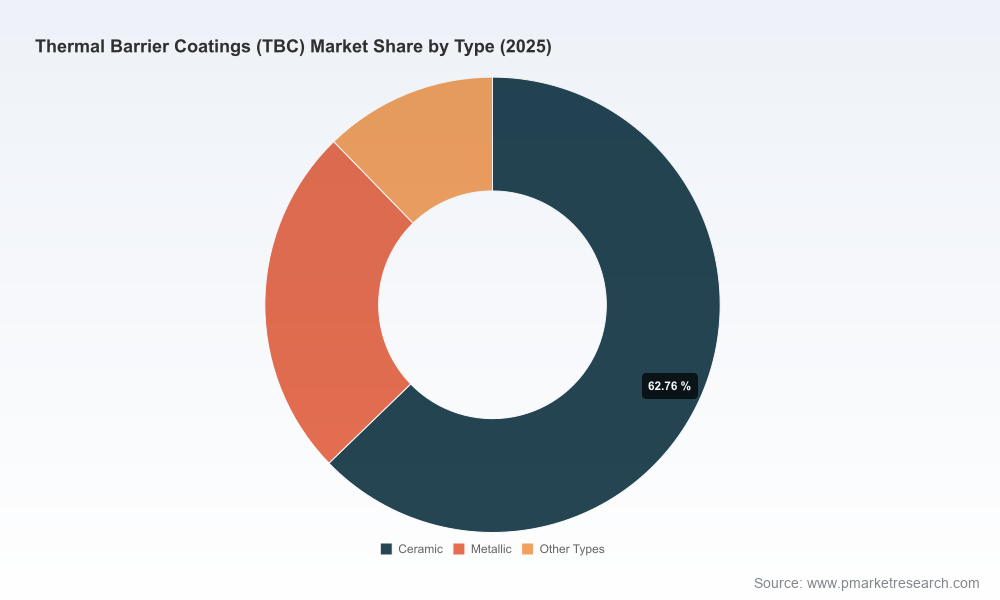

The TBC market demonstrated steady expansion over the early 2020s and reached USD 18,100 Million in our base year (2025). Forward projections indicate a mid‑single‑digit compound annual growth rate (CAGR) of approximately 5.1% across our 2026–2032 forecast window, with the market trending toward a materially larger addressable base by the end of the decade. Historical performance and the forecast both point to a market that is sufficiently large to invite continued industrial investment, yet concentrated enough to leave gaps for differentiated entrants and service innovation.

Thermal Barrier Coatings (TBC) Market

Why the TBC market will shape 2026 corporate decisions

- Operational leverage under regulatory acceleration: Stricter emissions and energy‑efficiency mandates for combustion systems are increasing the strategic value of coatings that deliver thermal efficiency and component life extension. For firms supplying engines, turbines and industrial burners, TBCs move from being a technical option to a compliance and cost‑savings lever.

- Raw material and cost volatility: Advanced ceramic compounds and specialty powders underpinning modern TBCs remain costly and supply‑sensitive. Procurement and price risk management will materially affect margins and investment cadence in 2026.

- Service economy and MRO opportunities: As fleets age and energy‑efficiency programs scale globally, Maintenance, Repair & Overhaul (MRO) demand for qualified TBC application and refurbishment is rising. Companies that integrate coating capability with MRO services can capture outsized margin pools.

- Technology bifurcation: Manufacturing approaches — from plasma and APS to EB‑PVD and HVOF — are evolving, with digital factory concepts and powder innovation driving throughput and performance gains. Early adoption of smart production and powder chemistry variants will define supplier rankings.

Market structure and competitive concentration — what to read between the lines

Market concentration metrics indicate that the TBC market is moderately consolidated at the top: the three largest suppliers command a material share, and the top five collectively represent a clear dominant cohort. That structure creates a dual incentive for mid‑tier firms: either pursue scale via consolidation or pursue specialization in technology, regional service networks, and OEM qualifications. For corporate strategists, this dynamic underscores the value of targeted partnerships and capability plays over broad, undifferentiated expansion.

Thermal Barrier Coatings (TBC) Market

Competitive landscape — players to benchmark and why

- Praxair Surface Technologies (Danbury, Connecticut) — Vertical integration across specialty powders and thermal spray services gives a competitive advantage where supply‑chain control matters most. Their model is a useful benchmark for firms considering upstream investment into powder production.

- Oerlikon Metco (Switzerland) — A leader in thermal spray equipment and EB‑PVD capabilities, recently advancing smart factory collaborations. Their integration of digital production processes illustrates how productivity and traceability become customer differentiators.

- Bodycote plc (United Kingdom) — Extensive global TBC service footprint highlights the commercial value of a broad MRO network and OEM certifications; a reference case for scaling service operations.

- H.C. Starck (Germany) — Specialist supplier of high‑purity YSZ and advanced powders. Their role is emblematic of the premium attached to material science leadership.

- Honeywell International (USA) — Combining powder production with IoT‑enabled performance monitoring, demonstrating the upside of integrated product‑service digital propositions.

- Chromalloy, Sulzer, Saint‑Gobain, ASB, Cincinnati Thermal Spray, APS Materials — Collectively, these firms illustrate the breadth of competing models: vertical integration, certified MRO services, regional mid‑market specialists and OEM‑qualified plasma spray providers. Each represents a distinct route to capture value — from OEM qualification to niche aftermarket dominance.

Recent moves and disruptive signals to monitor

- Smart factory and digitalization partnerships — exemplified by advanced collaborations between equipment specialists and aero OEMs — are accelerating unit cost improvements and quality control. Expect digital traceability and process automation to become commercial prerequisites for top‑tier contracts by 2026.

- Raw material pricing and hazardous‑waste regulations continue to shape supplier economics. Firms that secure lower input costs or circular‑material streams will open competitive cost advantages.

- Regulatory tightening on emissions and industrial energy budgets is acting as a demand catalyst, particularly where TBCs can be shown to deliver measurable fuel savings or emissions reductions.

Strategic plays we recommend for 2026

Actions below are prioritized for impact and implementability within a 12–24 month window:

- Secure material continuity and cost exposure: Negotiate multi‑year offtakes, explore strategic minority stakes in high‑purity powder producers, and implement hedging/supply‑pooling where feasible. KPI: reduce input cost volatility by optimizing supplier mix and contractual terms.

- Accelerate digital and process modernization: Pilot a smart production cell (digital process control, inline inspection, traceability) to reduce rework and qualify for higher‑value OEM programs. KPI: target unit cost decline and improved first‑pass yield within 12 months of pilot completion.

- Build an OEM/MRO qualification roadmap: Invest selectively to achieve OEM certifications and regional service stations, turning coating capability into a predictable recurring revenue stream. KPI: capture increased MRO shelf share in focused sub‑segments.

- Pursue targeted M&A and partnerships: Acquire narrow‑scope powder producers, regional MRO shops, or technology licences that fill capability gaps rather than chasing broad diversification. KPI: accretive deals that shorten time‑to‑market for new offerings.

- Operationalize regulatory and circularity requirements: Implement hazardous‑waste management protocols, lifecycle analysis for product claims, and explore reclaiming powders or coat‑stripping recycling to lower environmental and cost exposure. KPI: compliance readiness and potential cost recovery from recycling pilots.

- Commercialize outcome‑based offerings: Move beyond product sales to performance contracts (e.g., life‑of‑component, fuel‑efficiency guarantees) enabled by IoT monitoring. KPI: growth in service gross margin and customer retention.

What the full PW Consulting report delivers (practical, actionable content)

We designed the full report as a strategic toolset rather than a static market narrative. Key operational components include:

- Robust market-sizing and scenario models (base, downside, upside) for 2026–2032 with sensitivity to raw‑material pricing and regulatory tails.

- Supplier maps and capability matrices that identify where vertical integration yields the greatest ROI and where partnerships are preferable.

- Technology roadmaps and comparative performance benchmarking across deposition processes (plasma, APS, HVOF, EB‑PVD) to prioritize R&D spend.

- Regulatory heatmaps and waste‑management playbooks that translate compliance into boardroom actions.

- Commercial playbooks for OEM qualification, aftermarket pricing strategies, and outcome‑based contracting templates.

- M&A target shortlists and integration checklists, built from proprietary screening and validated by primary interviews with service providers and OEM procurement leads.

- Case studies and pilot templates (digital factory, recycling pilots) with expected P&L impact and implementation timelines.

How to convert this intelligence into 2026 plans (quarterly roadmap)

- Q1 — Strategic review & rapid diagnostics: Use our supplier and capability maps to run a 90‑day diagnostic on input risk and certification gaps. Decide on top two operational pilots (e.g., smart cell, recycling trial).

- Q2 — Contracting and pilots: Execute material supply agreements and begin smart production / recycling pilots. Start OEM qualification processes for prioritized product lines.

- Q3 — Scale & commercialization: Refine pilots based on measured KPIs, initiate commercialization of outcome‑based contracts, and shortlist M&A targets for diligence.

- Q4 — Consolidation & investment decisions: Evaluate pilot economics, finalize M&A or joint‑venture moves, and set 2027 budget allocations for technology and service rollouts.

Closing perspective — where value will be created

In 2026 the TBC market will reward organizations that manage three vectors simultaneously: control of critical material inputs, operational excellence through digitalization, and commercial models that monetize performance rather than merely product volumes. Market leaders will be those who translate material science into scalable, verifiable customer outcomes and who can navigate regulatory complexity while optimizing cost structures.

PW Consulting’s full market research report provides the granular segmentation, regional and application forecasts, and tactical playbooks to execute on the strategies summarized here. For firms making capital allocation and commercial decisions in 2026, that level of granularity will be decisive — and is available in the complete study.

For detailed analysis of this topic, please visit the official page:Thermal Barrier Coatings (TBC) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com