Semiconductor Etch Equipment Market — Strategic Preview for 2026 Decision Makers

As semiconductor supply chains reconfigure and device architectures migrate toward 3D, heterogeneous integration, and quantum-enabled processes, etch equipment has transitioned from a mature capital good into a strategic vectors for competitive differentiation. PW Consulting’s latest Semiconductor Etch Equipment Market review (base year 2025; forecast 2026–2032) synthesizes the commercial, technological, and geopolitical forces that will determine winners and losers through the next investment cycle.

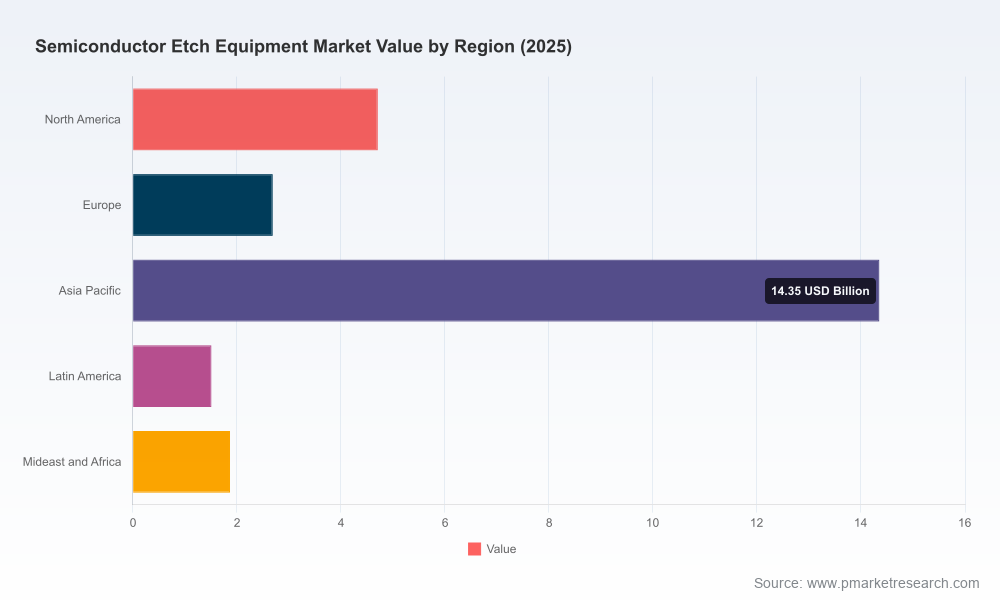

Semiconductor Etch Equipment Market

Top-line trajectory — what the numbers tell you (and what they don’t)

- The market grew materially over the 2020–2025 review period, and reached USD 25.13 Billion in our 2025 base year.

- Our 2026–2032 forecast projects a compound annual growth rate (CAGR) of 7.61%, taking the market to roughly USD 41.99 Billion by 2032 under the central case.

- Concentration is high: the leading vendors collectively command the vast majority of market revenue, creating an environment where a small number of firms shape technology roadmaps and supplier economics.

Those high-level figures matter for 2026 strategy because they reconcile two realities: robust demand driven by next‑generation logic and memory roadmaps, and structural rigidity caused by high integration and regulatory friction. Together, they create a premium on select capabilities (atomic-scale control, multi-chamber throughput, and integration with advanced packaging flows) and on disciplined go-to-market playbooks.

Semiconductor Etch Equipment Market

Why this report is a 2026 decision tool

Beyond headline forecasts, corporate leaders planning capex, R&D allocation, M&A, or supplier strategy need forward-looking, actionable intelligence that ties equipment demand to real procurement triggers. Our research translates macro growth into decision-ready outputs for 2026:

Semiconductor Etch Equipment Market

- Capital planning scenarios aligned to device roadmaps: three scenario matrices map etch equipment demand to logic, memory, and emerging device timelines, isolating timing risk and value‑capture windows for vendors and OEM customers.

- Technology maturity and adoption maps: proprietary readiness scores for atomic layer etch (ALE), high-density plasma controls, and etch integration for heterogeneous stacks — allowing product and process leaders to prioritize short-, medium-, and long-term R&D tranches.

- Supply‑chain risk and mitigation playbooks: supplier concentration heat-maps, dual‑sourcing strategies, and contingency options calibrated to lead times and service requirements in high-volume fabs.

- Regulatory impact assessment: scenario workstreams that translate export controls, foreign direct product rules, and emerging national policies into procurement and market‑access constraints for both OEMs and equipment buyers.

- Commercial templates: pricing elasticity benchmarks, trade-in and service revenue levers, and aftermarket capture strategies tailored to high‑concentration market structures.

The report purposely aggregates proprietary segment detail into operational recommendations. If your near-term capital commitments hinge on specific process or regional breakdowns, the full dataset and playbooks will materially shorten your execution time.

Competitive landscape: who matters and why

The etch market is dominated by a small set of mature equipment OEMs, each leveraging complementary strengths. Our analysis highlights strategic positioning across product technology, manufacturing footprint, and go‑to‑market intent.

- Applied Materials, Inc. (Santa Clara, CA) — a systems integrator with breadth across wafer processing; competitive advantage comes from cross‑tool process integration and service ecosystems that accelerate customer qualification cycles.

- Lam Research Corporation (Fremont, CA) — a technology leader in conductor etch and plasma control. Recent product introductions underscore an emphasis on atomic‑scale precision and multi‑chamber modularity to support 3D device stacks.

- Tokyo Electron Limited (Tokyo, Japan) — combining manufacturing scale with local fabs strategy; expansion in production capacity signals readiness to meet rising Asian demand while reducing lead times for customers.

- Hitachi High‑Tech Corporation (Tokyo, Japan) — niche strength in process metrology and etch-related subsystems; offers an adjacent route to capture margin through process analytics and optimization services.

- Oxford Instruments plc (Abingdon, UK) — focused on precision atomic layer etch systems and research partnerships, increasingly visible in quantum and advanced node prototyping.

- SPTS Technologies Ltd (Newport, UK) — a specialist in etch and deposition tools for advanced packaging and MEMS, placing it as a tactical partner for foundries diversifying into heterogeneous integration.

- Plasma‑Therm LLC (Northampton, MA) — regional player with strengths in customizable plasma solutions for niche process flows and long tail customers.

- ASML Holding N.V. (Veldhoven, Netherlands) — while traditionally centered on lithography, its ecosystem role and supply relationships influence etch tool roadmaps and node timing assumptions.

- ULVAC, Inc. (Chigasaki, Japan); NAURA Technology Group (Beijing, China); and SAMCO Inc. (Kyoto, Japan) — each brings differentiated regional access, cost structures, and product mix that matter for customers executing distributed fab strategies.

Market concentration metrics show that a handful of providers determine technology direction and aftermarket economics. Consequently, partnerships, licensing deals, and targeted investments in compatibility and serviceability are critical levers for OEMs and fab owners alike.

Recent developments shaping near‑term decisions

- Product innovation: major vendors introduced next‑generation conductor etch systems with advanced plasma control architectures, indicating that tool performance, not just throughput, will be a primary procurement differentiator.

- Capacity plays: select OEMs initiated manufacturing expansions to shorten lead times as demand shifts geographically and to absorb higher mix complexity associated with 3D architectures.

- Academic and industry collaboration: equipment donations and joint R&D programs signal a new wave of co‑development that can accelerate qualification cycles and reduce integration risk for early adopters.

- Alternative markets: delivery of atomic layer etch systems into quantum device fabrication highlights an adjacent growth runway beyond conventional logic and memory applications.

For 2026 planners, these developments mean you cannot treat vendor selection as a plug‑and‑play exercise. Instead, procurement and process integration must be synchronized with R&D sampling, qualification timelines, and contingency provisions for regulatory shocks.

Regulatory and geopolitical framing — the new baseline

Export controls and targeted restrictions introduced since late 2024 have redefined market access dynamics. Recent policy actions — including expanded export controls on advanced packaging equipment, additions to entity lists, and broader rules extending jurisdiction over foreign‑produced tools — have the following implications:

- Dealer and vendor risk: acquisition of certain classes of etch tools now requires new compliance workflows and, in some cases, pre‑clearance of supply chains.

- Regional sourcing strategies: manufacturers and foundries must reassess dual‑source plans, balancing cost against localization and regulatory certainty.

- Technology leakage prevention: R&D partnerships and material transfers require tighter governance, particularly when collaboration spans sensitive geographies.

We model several regulatory scenarios in the report, from incremental controls to more sweeping restrictions, and quantify the likely demand displacement and procurement latency each scenario produces.

What leaders should do now — a 90‑day playbook for 2026

- Immediate: run a vendor‑compatibility delta analysis for current node roadmaps and prioritize tools that reduce qualification cycles (target: shorten first silicon risk by ≥25%).

- Near term (3–9 months): secure conditional options with primary and validated secondary suppliers; hedge exposure to single‑country manufacturing through contractual SLA and spare‑parts stores.

- Medium term (9–18 months): invest selectively in process co‑development with equipment partners to lock in throughput and yield advantages; evaluate minority stakes or licensing to secure roadmap inputs without full vertical integration.

- Policy preparedness: implement enhanced export‑control due diligence for procurement, and map tier‑1 and tier‑2 supplier entities to the latest regulatory lists to preempt compliance friction.

These steps are calibrated against the market’s projected growth and concentration profile. They are designed to convert the macro upcycle (CAGR ~7.6%) into defensible competitive advantage rather than commodity bidding wars.

What the full report contains (briefly)

- Comprehensive market sizing with historical 2020–2025 data and granular forecasts through 2032; sensitivity cases and methodology notes.

- Technology roadmaps and adoption curves for etch variants, plasma control systems, and integration pathways for advanced packaging and 3D devices.

- Supplier benchmarking: capability maps, manufacturing footprints, margin models, and aftermarket revenue diagnostics for the leading OEMs.

- Regulatory stress‑tests: quantified demand shifts under alternate export control scenarios and practical compliance checklists for procurement teams.

- Deal playbooks and valuation priors for M&A, JVs, and strategic minority investments tailored to both OEMs and fab owners.

We deliberately withhold the full segment tables and granular regional/application breakdowns in this preview to protect the commercial value of the primary research. Those datasets and interactive decision tools are included in the full report and are essential for any team executing capex, sourcing, or M&A decisions in 2026.

Final thought

Etch equipment is no longer a back‑office capital purchase — it is a strategic lever in product differentiation, supply‑chain resilience, and geopolitical risk management. With the market at a USD 25.13 Billion baseline in 2025 and clear upside to 2032 at a ~7.61% CAGR, the cost of being a late optimizer in 2026 is measurable. PW Consulting’s full Semiconductor Etch Equipment Market study furnishes the datasets, scenarios, and playbooks your leadership team needs to convert macro growth into defensible advantage.

For access to the detailed tables, vendor scorecards, and scenario models that underpin these conclusions, please visit our report page to request the full dataset and advisory engagement options.

For detailed analysis of this topic, please visit the official page:Semiconductor Etch Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com