The Definitive Engineering Standards for Professional Fence Installation in Seattle, WA

Other |

2026-07-01 10:13:49

As chitosan moves from a niche biopolymer into multi-industry adoption, corporate leaders face a pivotal decision window in 2026: invest to capture accelerating demand, or watch competitors lock in scale and certification-led premiums. PW Consulting’s latest market study synthesizes quantitative growth trajectories, regulatory inflection points, and supplier-level dynamics into a decision-ready intelligence package. Below is a strategic preview that demonstrates the report’s analytical depth while preserving the proprietary segment detail that makes the full study essential for transaction and portfolio choices.

Chitosan Market

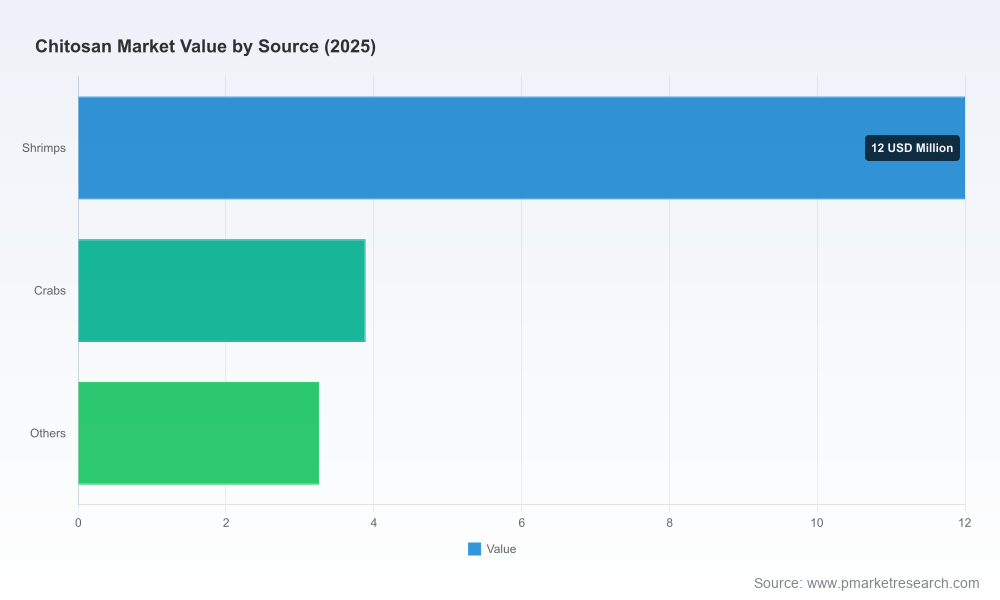

Chitosan is no longer an experimental input. The industry has scaled quickly — rising from approximately USD 7.8 million in 2020 to roughly USD 19.2 million in 2025 — and is forecast to expand to the high tens of millions by the early 2030s. Our model, based on historical adoption curves, feedstock availability, and application-level uptake, projects a compound annual growth rate of roughly 19.8% over the forecast window. By 2032 the market is expected to exceed USD 65 million, creating a multi-fold enlargement of opportunity across pharmaceuticals, agrochemicals, water treatment, and consumer-facing sectors.

Chitosan Market

This macro expansion matters because chitosan’s addressable market touches systems with long procurement cycles (e.g., regulated pharmaceuticals) and fast-moving commercial channels (e.g., crop biostimulants). The mixed velocity across end-markets raises distinct strategic questions for manufacturers, private-equity investors, and downstream integrators: where to prioritize capacity, which quality standards to invest in, and how to hedge feedstock exposure.

Chitosan Market

Put simply, 2026 is when regulatory access, product readiness, and supply flexibility converge to determine who captures the next leg of growth. Boards and investment committees must treat this year as a call to commit resources to capability, not as a distant possibility.

The chitosan landscape blends niche specialist producers with larger chemical and biotech suppliers. Market concentration remains moderate: the top three suppliers account for a meaningful but not dominant portion of capacity, and the top five expand that footprint further, indicating both leadership pockets and white space for consolidation and differentiation.

Key firms exemplify these archetypes. Several European and Nordic players emphasize medical-grade, high-purity production and customized formulations. Asian manufacturers provide scale and cost-competitive volumes that feed commodity and industrial channels. New entrants and adjacent players are commercializing application-specific formulations for agriculture and consumer health. The strategic implication is clear: scale alone will not secure leadership in 2026 — certification, formulation expertise, and route-to-customer matter as much.

Two systemic dynamics determine near-term strategic value:

Our report contains a regulatory tracker and a feedstock risk matrix that quantifies these variables across scenarios, enabling procurement teams to test hedging strategies and investment timing against a probabilistic policy calendar.

Readers of this preview should understand what lies behind the headline numbers. The full study provides operational and commercial tools designed for use in boardrooms and deal rooms:

We deliberately withhold granular segment-level tables and supplier market share dashboards in this preview. Those are core-value assets that drive commercial decisions and are included in the full report and client workshops.

Clients should consider a menu of defensible moves calibrated to their starting position:

Several commercial and regulatory events in the last 18 months illustrate the landscape’s direction: new product introductions for agricultural and inhaled delivery uses, distribution partnerships expanding reach in emerging markets, and formal regulatory reviews that could change organic classification and permitted use cases. Each of these events affects market access and pricing dynamics. PW Consulting’s report models the downstream effects of these milestones on revenue trajectories and supplier economics.

For executives and investors, the dominant strategic risk is under-exposure rather than over-commitment. Chitosan’s projected multi-decade growth and the near-term regulatory determinations make 2026 a decisive year: firms that establish optionality across feedstock, certification, and application-specific IP will be best positioned to harvest the market expansion. Those that delay will face higher customer switching costs and compressed margins as incumbents deepen relationships and scale production.

If your organization is evaluating capacity investments, M&A targets, or product roadmaps tied to chitosan, PW Consulting’s full market study provides the empirical models, supplier scorecards, and regulatory playbooks to move from hypothesis to executable strategy. For clients requiring immediate support, we also offer tailored workshops and live market models to stress-test investment cases in real time.

To access the complete segmentation, supplier scorecards, and downloadable financial models, please consult the PW Consulting Chitosan Market study or contact our industry practice for a briefing and customized roadmap.

For detailed analysis of this topic, please visit the official page:Chitosan Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com