GaN on Diamond Semiconductor Substrates: Strategic Preview for 2026 Decision-Makers

Executive preview

By the end of our 2025 baseline year, the GaN on diamond semiconductor substrates market has emerged from niche R&D into an investable industrial frontier. PW Consulting’s proprietary modeling places the overall market at roughly USD 33 million (base year 2025) and projects a robust compound annual growth rate of approximately 17.0% through our 2026–2032 forecast window. Under current assumptions, that trajectory implies a market approaching the low‑hundreds of millions of dollars by 2032—enough scale to change sourcing, product and partnering strategies for device OEMs, substrate suppliers and system integrators.

GaN on Diamond Semiconductor Substrates Market

Why this matters for 2026 strategic choices

GaN on diamond substrates combine GaN’s high breakdown field and electron mobility with diamond’s exceptional thermal conductivity, unlocking step‑changes in power density and RF performance. For decision-makers evaluating capital allocation, partnerships, M&A, or new product introductions in 2026, three facts are decisive:

GaN on Diamond Semiconductor Substrates Market

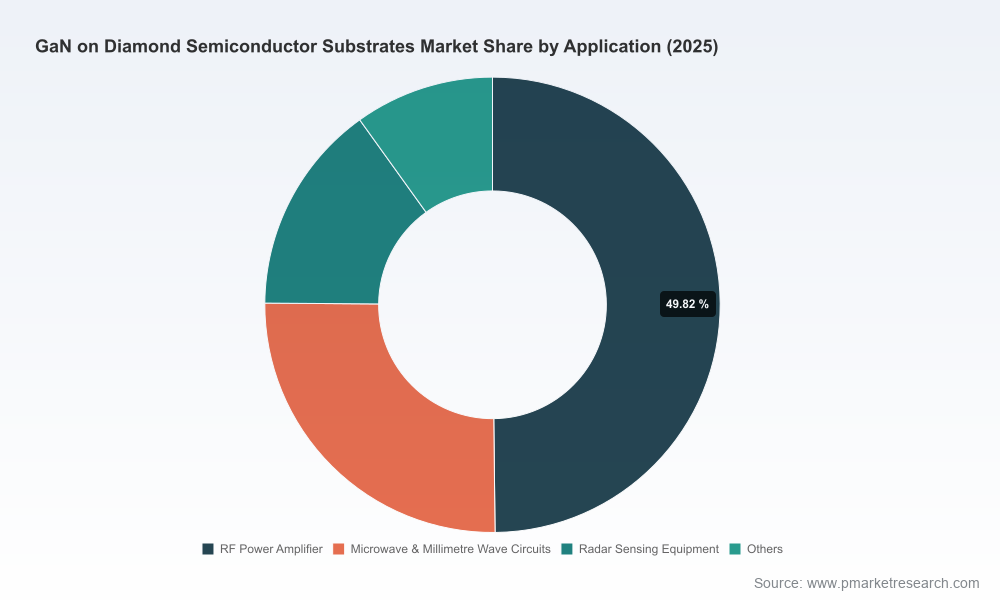

- Market momentum is real and measurable. Post‑2025 adoption curves are driven by an expanding set of compelling end‑use cases—satellite communications, advanced radar and mmWave systems, and high‑power RF amplifiers—where thermal management is a gating constraint.

- Supply-side dynamics remain the primary strategic constraint. Synthesis and bonding processes for CVD diamond wafers are costly and capacity‑constrained, creating near‑term scarcity that favors players with vertical capabilities or guaranteed offtake agreements.

- Policy and defense procurement are accelerants. Targeted government programs and defense contracts are already shortening commercialization cycles for GaN on diamond in mission‑critical platforms, increasing near‑term addressable demand beyond commercial forecasts alone.

What the full study gives you (practical, decision-ready outputs)

We designed the full report as a toolkit to convert technology promise into executable strategy. Highlights of the operational deliverables include:

GaN on Diamond Semiconductor Substrates Market

- Proprietary market-sizing and demand‑scenarios, with sensitivity testing across pricing, yield improvement and policy adoption assumptions—structured so corporate planners can plug in their own product roadmaps.

- Techno‑economic models that quantify unit economics by wafer type, bonding process and scale milestones, including break‑even scenarios for in‑house diamond synthesis versus contract supply.

- Supplier maps and manufacturing roadmaps—covering upstream diamond synthesis, epi growth, wafer bonding and device integration—plus contingency routes for faster scale or spot shortages.

- Go‑to‑market strategies for three archetypal companies: substrate specialists, GaN device OEMs, and systems integrators—each with recommended partnership structures, prioritization matrices and commercialization timelines.

- Regulatory and procurement playbooks that translate DARPA/DoD funding signals and export controls into near‑term demand pools and compliance actions for commercial teams.

- A decision matrix for M&A, joint ventures and greenfield investments, including candidate screens, valuation levers and an execution checklist for 90‑ to 360‑day integration risks.

Competitive landscape — who to watch and why

The supplier ecosystem today is a mix of specialized diamond houses, RF semiconductor companies and venture‑backed substrate innovators. Market concentration is meaningful but not prohibitive: the top three suppliers account for roughly a third of the market while the top five remain under half, leaving room for new entrants and regional champions to emerge as capacity grows.

- Element Six (Didcot, UK) — A leading synthetic diamond specialist, focused on ultra‑high‑purity single‑crystal diamond wafers tailored for RF and power device thermal solutions. Their recent product introductions (early 2025) underscore a strategy to move up the value chain into application‑specific substrate formats.

- Akash Systems (California, US) — A developer of GaN‑on‑diamond technologies for satellite communications; notable for securing CHIPS Act funding to accelerate demonstration and qualification. Akash represents the class of nimble innovators translating niche defense and satcom requirements into commercial roadmaps.

- Qorvo, Inc. (Greensboro, NC, US) — An RF device and amplifier manufacturer that has publicly showcased GaN‑on‑diamond power amplifiers with reduced thermal resistance. Qorvo exemplifies how established RF OEMs can vertically integrate or lock long‑term supply partners to protect performance advantage.

- RFHIC Corporation (Anyang, South Korea) — Supplies GaN‑on‑diamond epi wafers with a focus on radar, microwave and satellite markets—an example of regional capability that can influence procurement choices for Asian system integrators.

- Coherent Corp. (San Jose, CA, US) — Positioned to scale GaN‑on‑diamond wafer formats for commercial RF volumes, bridging lab innovations and higher throughput manufacturing.

- Blue Wave Semiconductor (US) — A commercializer targeting high‑power RF and defense electronics; representative of smaller firms that may be acquisition targets for larger substrate or device manufacturers.

Recent industry moves to factor into 2026 plans

Between 2024 and 2025 the sector has seen a series of catalytic events: product launches of higher‑purity single‑crystal diamond wafers, acquisitions aimed at vertical integration, JV formations to shore up regional supply, public funding for satellite and defense applications, and the unveiling of GaN‑on‑diamond amplifiers. Together, these developments accelerate commercialization but also raise the strategic bar: companies that do not secure supply, IP access or government engagement risk being relegated to secondary suppliers when demand spikes.

Key risks and mitigants

Executives should weigh four primary risks when defining 2026 strategy—and the report offers mitigants for each:

- Supply bottlenecks and high unit costs: Mitigate via offtake agreements, co‑investment in CVD capacity, or alternative thermal management architectures while monitoring yield improvement milestones.

- Geopolitical and trade risks: Build regional supply redundancy and pre‑qualify alternate suppliers to insulate production lines from export controls or material flow disruptions.

- Technical and integration risks: Use staged qualification plans and risk‑sharing contracts with substrate suppliers; prioritize designs tolerant of incremental thermal performance improvements.

- Policy and procurement volatility: Engage early with defense and government funding agencies to shape program requirements and secure anchor contracts that de‑risk commercial scaleup.

Practical recommendations for 2026 roadmaps

Based on our scenario work and conversations with industry leaders, PW Consulting recommends a set of prioritized actions for corporate leadership teams preparing 2026 budgets and roadmaps:

- Adopt a “supply-first” posture if your product roadmap depends on GaN on diamond: secure material options and protect lead times before scaling device production.

- Pursue selective vertical integration where economics support it—particularly for firms that can justify CapEx on diamond synthesis when long‑term demand visibility exists through multi‑year contracts.

- Leverage government and defense funding to derisk early demonstrations and reduce effective cost of qualification for commercial customers.

- Structure partnerships with substrate specialists on a staged IP and volume ramp basis—this preserves agility while securing access to specialized processes.

- Maintain optionality through dual design tracks that can accept conventional high‑performance thermal substrates if GaN‑on‑diamond yields lag projections.

Why PW Consulting’s report is decision‑relevant

This study is not an abstract technology brief. It is a decision tool: calibrated market models, executable supplier contracts frameworks, investment case templates and regulatory playbooks that align with board‑level capital allocation timelines for 2026. We show when and how the market goes from constrained niche to commercial scale under different yield, price and policy scenarios—and we map the inflection points that should trigger investment, acquisition or tactical withdrawal.

What we intentionally withhold here — and where to get it

In this preview we present the macro view and strategic implications while deliberately withholding the granular split data and proprietary segment forecasts that materially affect competitive positioning. The full report contains detailed regional and application segmentations, unit‑level cost breakouts, supplier scorecards and downloadable models that companies use to populate internal business cases. To access that level of granularity and the downloadable financial models, please consult the full GaN on Diamond Semiconductor Substrates Market study on PW Consulting’s portal or contact our client services team for a tailored briefing.

Closing note for leaders

2026 will be the year when choices about supply, partnership and product architecture determine winners and followers. The combination of accelerating demand, constrained upstream capacity and targeted public funding creates both a window of opportunity and a trap for the unwary. Use the next twelve months to lock supply pathways, clarify your IP stance and engage early with procurement agencies. The full PW Consulting report gives you the playbook to do exactly that—structured for rapid operationalization and boardroom decisions.

For detailed analysis of this topic, please visit the official page:GaN on Diamond Semiconductor Substrates Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com