IC-Substrate Market: Strategic Imperatives for 2026 Decision‑Makers

Executive overview

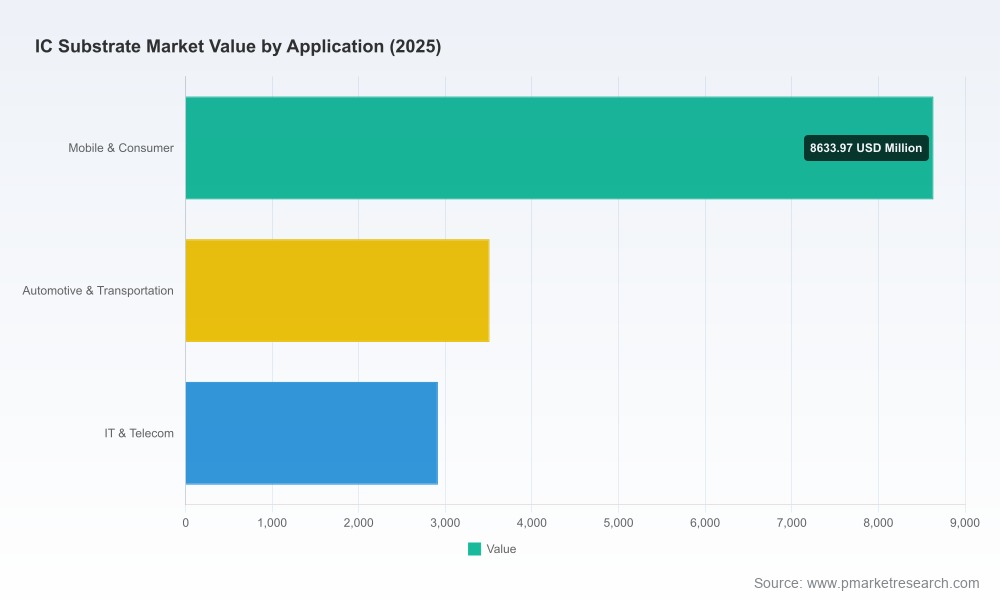

The IC‑substrate market has re‑emerged as a linchpin for semiconductor ecosystem competitiveness. After a steady recovery from 2020, the market reached roughly USD 10 billion in our base year (2025) and is projected to expand at a compound annual growth rate of 6.63% through our forecast window, reaching about USD 15.5 billion by 2032. That pace reflects a confluence of structural demand — driven by AI/HPC server systems, advanced mobile and consumer features, electrified transportation, and next‑generation telecom infrastructures — together with material and capacity dynamics that are tightening the supply side.

IC-Substrate Market

Why this study matters for 2026 corporate decisions

- Capital allocation: Firms deciding whether to green‑field, brown‑field, or enter capacity sharing in 2026 need precise, time‑phased demand and price scenarios to avoid stranded assets or missed opportunity windows.

- Supply chain and procurement: Raw‑material scarcity and supplier concentration are already influencing pricing and delivery. Procurement strategies that are calibrated to realistic supply risk curves will materially affect margin outcomes.

- Technology roadmaps: Choosing between ABF, glass‑core, rigid‑flex, and emerging multifunctional cores impacts product architecture, vendor selection, and R&D prioritization over a multi‑year horizon.

- M&A and partnerships: Identifying attractive targets or partners requires triangulating capacity, technology readiness, and regulatory tailwinds; timing is critical in 2026 as capacities added now ramp into 2027–2028 demand profiles.

- Regulatory and funding leverage: Public programs and grants are shaping competitive advantage; firms that align investment plans to available incentives can reduce payback timelines.

Market trajectory and key forcing functions

The trajectory through 2032 is not a passive extrapolation of past growth. Two sets of forces are most consequential. On the demand side, AI server deployment and high‑performance computing drive material intensity per chip package and accelerate migration to high‑end flip‑chip and glass‑core substrates. Mobile, automotive, and telecom each contribute varying loads of volume and technology requirements, but the marginal dollar growth through 2026–2032 is disproportionately concentrated in high‑value, high‑complexity substrates.

IC-Substrate Market

On the supply side, capacity investments announced and being executed in 2025–2027 will determine who can monetize rising demand. At the same time, raw material dynamics — notably persistent fiberglass and base‑resin constraints — are elevating input price volatility and creating localized supply bottlenecks. Finally, regulatory interventions and public funding (for example, targeted semiconductor acts and EU programs) are accelerating localized capacity builds and de‑risking certain investments for incumbents and new entrants alike.

IC-Substrate Market

Competitive landscape — strategic reads on the core players

The competitive map is characterized by a handful of established substrate specialists and a set of aggressive, vertically integrated electronics manufacturers expanding their substrate footprints. Market concentration is meaningful: the leading firms together command a majority share, but competition is intensifying at the high‑end of the value chain.

- Ibiden — A Japan‑based specialist doubling down on high‑performance package substrates. Recent capacity commitments and cross‑border fab plans position Ibiden as a go‑to supplier for AI server substrates; their strategy blends domestic scale‑up with targeted foreign capacity to capture demand spikes while aligning with policy incentives. For customers, Ibiden represents a premium, high‑reliability partner with capacity that will materially affect supply dynamics from late‑2027 onward.

- Unimicron — A Taiwanese substrate leader focused on advanced flip‑chip technologies, including ABF and glass‑core variants. Their posture combines aggressive capacity management with pragmatic pricing actions when raw‑material stress hits. Unimicron’s recent upward price adjustments signal a willingness to protect long‑run margins, which has implications for OEM sourcing strategies and contract negotiation windows.

- AT&S — An Austria‑headquartered player accelerating industrial deployment of glass‑core and multifunctional substrates. Their push into multifunctional core integration and European capacity expansion is designed to capture high‑end HPC and photonics use cases and to benefit from regional funding programs. For buyers prioritizing geographic diversity and advanced substrate features, AT&S is an increasingly strategic option.

- Samsung Electro‑Mechanics — Leveraging deep electronics integration and large capex programs, Samsung is shifting from component supplier to substrate scale player in select high‑value segments. Their investments can rapidly change capacity economics in markets where they choose to compete, creating both opportunity and risk for specialist substrate vendors.

- Kinsus, Shinko, Kyocera, LG Innotek, Nan Ya — Collectively, these firms form the innovation and volume backbone of the industry. Some are niche specialists in ABF or low‑loss laminates, others are expanding into embedded and rigid‑flex applications. Their product roadmaps, order wins, and regional investments will determine where premium price realizations occur and where commoditization pressures compress margins.

Supply chain, raw material and regulatory dynamics

2026 is shaping up as a year in which supply‑side resilience, not demand growth alone, determines commercial outcomes. Two dynamics are particularly material:

- Fiberglass and base resin scarcity: The market continues to experience constrained supply of key substrate inputs, leading to sharp supplier price actions and selective allocation. This is prompting buyers to re‑think inventory models, contract tenors, and cost pass‑through clauses. Risk mitigation options include secured long‑term offtake, co‑investment in upstream materials, and validated alternative chemistries.

- Targeted public funding and industrial policy: Grants and subsidies are altering the returns calculus for green‑field projects in certain geographies. Firms that can align investments with policy programs achieve lower effective capital costs and faster market access — but the administrative complexity and conditionality of such funding require careful program navigation.

What the PW Consulting IC‑Substrate Market study delivers (operational highlights)

Our report is designed as a decision‑grade toolkit for executives, strategy teams, and transaction advisors. Key deliverables include:

- Scenario‑based demand models (2026–2032) with stress tests tied to AI server adoption, automotive electrification, and telecom investment cycles.

- Time‑phased capacity and utilization maps highlighting near‑term pinch points and expected relief timelines, plus a dynamic view of competitive ramp schedules.

- Supplier scorecards and procurement playbooks that synthesize technology readiness, financial strength, geographic footprint, and supply risk into actionable vendor tiers.

- Raw‑material cost‑curve and sensitivity analytics that quantify margin exposure to fiberglass and base‑resin shocks and model the impact of supplier price pass‑throughs.

- Capex decision templates and ROI calculators to evaluate green‑field vs. brown‑field vs. tolling strategies under multiple demand and policy scenarios.

- Go‑to‑market and M&A screening frameworks to identify targets and partners that complement product portfolios, geographic coverage, or technology stacks.

- Technology roadmaps comparing ABF, glass‑core, rigid‑flex and emerging multifunctional cores on parameters such as performance, manufacturability, and cost trajectory.

How to translate insights into 2026 actions

- Short term (rolling 12 months): Secure supply through longer‑tenor contracts with key substrate suppliers, prioritize critical projects for guaranteed allocation, and deploy conditional price escalators tied to raw‑material indices.

- Medium term (2026–2028): Reassess fleet and capacity partnerships — where capital is constrained, consider co‑investment or tolling relationships with established substrate manufacturers; accelerate qualification plans for alternative substrate technologies if performance trade‑offs are acceptable.

- Long term (post‑2028): Invest in differentiated substrate capabilities (e.g., low‑loss laminates, glass‑core multifunctional designs) that act as durable moats, and align R&D funding to anticipated packaging transitions driven by AI and photonics integration.

Conclusion — why now

The 2026 decision calendar is unforgiving: capacity choices, supplier contracts, and technology bets made this year will crystallize supply positions when AI server and HPC demand ramps in earnest through 2027 and beyond. Our IC‑Substrate Market study provides the granular scenarios, supplier intelligence, and investment playbooks necessary to make those calls with confidence. The analysis deliberately reveals strategic direction and actionable frameworks while reserving the granular segment tables and vendor scorecards for the full report — the datasets you will need to convert insight into transaction‑grade decisions.

Next steps

For a walkthrough of the data models, supplier scorecards, and tailored scenario simulations (including bespoke ROI modelling for proposed capex), visit the full study on our publication page or contact PW Consulting’s IC‑Substrate practice to schedule a briefing. The market is moving; practical, data‑grounded choices in 2026 will determine competitive positioning into 2032.

For detailed analysis of this topic, please visit the official page:IC-Substrate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com