AI and Blockchain Technologies Revolutionize the Cross Border Payments Industry

Other |

2026-05-08 13:08:59

As PW Consulting’s Senior Strategic Advisor and Head of Industry Analysis, I present a high-level executive primer that synthesizes the directional intelligence from our full Eddy Current Sensor Market study. The objective here is to make clear, actionable connections between macro market dynamics and the set of tactical choices leaders must weigh in 2026—without disclosing the granular segmentation tables that are reserved for the full report.

Eddy Current Sensor Market

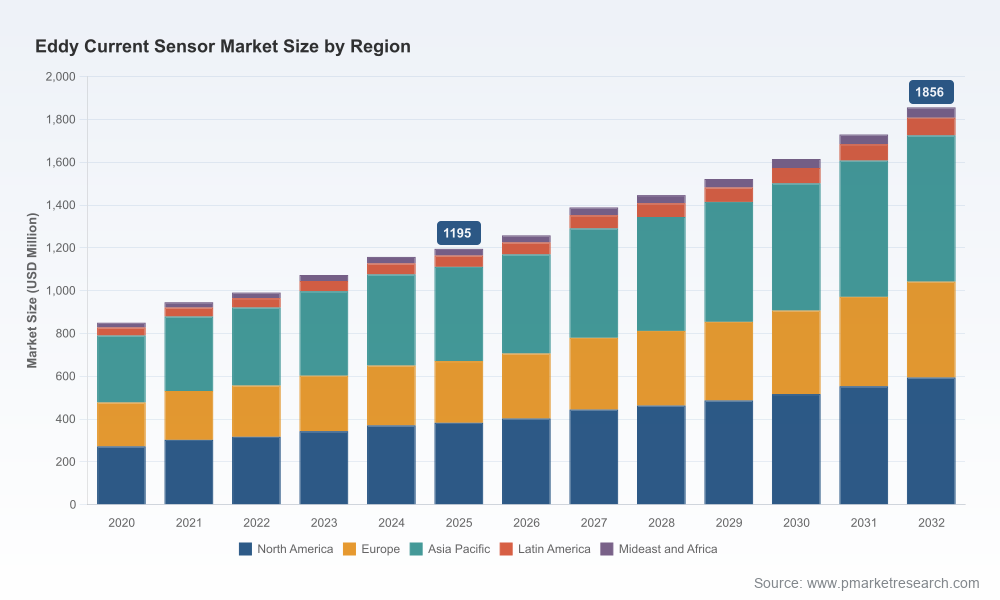

Eddy current sensing is moving from niche measurement functions into embedded, mission-critical roles across industrial automation, turbomachinery health monitoring, non-destructive testing (NDT), and advanced manufacturing metrology. Our market model—anchored on a 2025 base year—shows the market growing from roughly USD 1.195 billion in 2025 to an expected USD 1.856 billion by 2032, at a compounded annual growth rate (CAGR) of approximately 6.5% across the 2026–2032 forecast window. The segment has already demonstrated a resilient recovery over 2020–2025, rising from a sub‑billion base and tracking steadily higher as industry adopters increase precision sensing and embed diagnostics into asset lifecycles.

Eddy Current Sensor Market

For executive teams making 2026 investment decisions, these headline figures are not merely descriptive: they provide a sizing envelope for commercial expansion, R&D prioritization, and M&A appetite. The growth trajectory supports disciplined investments to capture share in higher-value system integrations and services, while also underlining the need for focused supply‑chain risk mitigation given rising commodity and geopolitical pressures.

Eddy Current Sensor Market

From component to system: buyers are increasingly valuing sensors as inputs to predictive-maintenance and condition-monitoring systems rather than discrete measurement widgets. Companies that move up the stack—pairing high‑precision eddy current probes with analytics, communications modules, and lifecycle services—will capture higher margin pools even as hardware ASPs face pressure.

Ruggedization and standards compliance are commercial differentiators. IP69K-rated devices and explicit alignment with IEC/ISO testing and personnel certification regimes materially shorten procurement cycles in industrial and defense contracts.

Supply and sourcing friction is real. Commodity volatility (e.g., copper coil costs) and rare‑earth export constraints raise component inflation risk. Tariff regimes and export controls on China-origin sensors introduce localized cost disadvantages and inventory planning complexity for North American and European OEMs.

Consolidation and strategic partnerships are accelerating. The market shows moderate concentration—the top three players account for a meaningful share of revenue, and the top five increase that share materially—creating an environment where M&A, alliances, and platform partnerships are an efficient route to scale and capability acquisition.

The market is populated by a mixture of precision-sensor specialists, industrial automation giants, and NDT-focused instrument providers. Below is a thematic synthesis of competitive positions and implications for 2026 strategy:

Micro‑Epsilon (Germany): A technology leader in high‑precision displacement sensors. Recent product introductions—most notably submicron, IP69K-rated devices—signal a deliberate push into harsh-environment industrial segments. Strategic implication: incumbents must match accuracy and ingress protection claims or differentiate via system-level services.

Lion Precision (United States): Specialized in linear encoders and precision displacement sensors. Their focus on ultra‑stable metrology positions them well for semiconductor and advanced manufacturing customers that value repeatability and traceability.

Eddyfi Technologies (Canada): A leading name in eddy current array probes and NDT instrumentation. The firm’s capabilities in array imaging and software-rich inspection workflows are highly relevant to pipeline, aerospace, and power-generation customers—especially where inspection automation is required.

Rohmann GmbH (Germany): Focused on eddy current NDT instruments and probes tailored for crack detection and material sorting. Their product breadth in inspection instruments makes them a natural partner for industrial service providers and OEMs seeking turnkey testing cells.

Emerson (United States): With sensor offerings targeted at turbomachinery monitoring, Emerson brings deep systems-engineering and aftermarket service capabilities. Their specifications updates reflect continuous optimization for radial/axial displacement sensing in rotating equipment.

AEC, Eddysun, Kaman, Keyence: These firms cover a spectrum from Japan-based integrated measurement systems to China-based NDT module providers and U.S. proximity probe specialists. The diversity in product strategy—from low-cost modules to integrated instrumentation—creates competitive pressure across price and capability dimensions.

Product innovation remains rapid. For example, the launch of submicron, IP69K-capable displacement sensors underscores that accuracy plus ruggedization is a market-winning combo for harsh industrial settings.

Partnerships between automation OEMs and sensing specialists point to a distributed go‑to‑market model where controls vendors leverage sensor expertise to accelerate factory deployments at scale.

M&A activity—highlighted by the acquisition of specialist NDT vendors—signals buyer appetite for integrated inspection suites (hardware + software + services). Expect further consolidation as platform players seek to add array capabilities and inspection analytics.

R&D and product roadmaps: Prioritize rugged, high-accuracy, and digitally enabled sensors (embedded communications, APIS, and edge diagnostics). Invest selectively in eddy-current array tech or systems integration where it creates defensible stickiness with industrial buyers.

Supply‑chain de‑risking: Map critical component exposure (coils, magnets, electronics) and develop dual‑sourcing, inventory buffers, or near‑shoring strategies for key assemblies. Negotiate conditional price‑protection clauses for commodity volatility.

Commercial strategy: Shift selling motions from point‑product to outcome‑oriented offers—bundles that combine sensors, analytics, installation, and inspection services. Build channel partnerships with controls OEMs and integrators to accelerate deployments.

Regulatory and talent investments: Ensure compliance to relevant ingress and testing standards; invest in NDT inspector certification programs aligned to ISO requirements to reduce procurement friction for customers in regulated industries.

M&A and alliances: Use M&A to acquire software-heavy inspection capabilities or array probe expertise. Consider partnerships to expand footprint quickly in regions where tariff or export regimes otherwise impede direct competition.

Executives need foresight that translates to capital allocation decisions, product bets, and go‑to‑market reshaping. Our study provides the quantitative envelope (historical market trajectory, 2025 baseline, and 2026–2032 forecasts) and a qualitative playbook to inform: incremental R&D budgets, acquisitions versus partnerships, pricing strategies under commodity stress, and regional investment sequencing. The analysis is intentionally transaction-focused—designed to reduce due-diligence time on acquisition targets and de-risk greenfield expansions.

If your team is evaluating sensor platform investments, M&A, or a major re-sourcing decision in 2026, the full PW Consulting report contains the detailed segmentation matrices, company-level financial proxies, and scenario-based sensitivity analyses required to underwrite those moves. The executive primer here outlines the strategic imperatives; the full deliverable translates them into actionable financial models, playbooks, and a prioritized implementation roadmap.

Contact PW Consulting to obtain the complete Eddy Current Sensor Market report and the underlying model, or request a tailored briefing where we map these insights directly onto your portfolio or investment thesis.

For detailed analysis of this topic, please visit the official page:Eddy Current Sensor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com