Band Saw Blades Market: Strategic Briefing for 2026 Decisions

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present an executive introduction to our comprehensive Band Saw Blades Market study. This briefing synthesizes the report’s most decision-relevant signals for 2026 while deliberately withholding granular segment-level tables and regional breakdowns to preserve the value of the full dataset and models available on our portal.

Band Saw Blades Market

Why this study matters for 2026

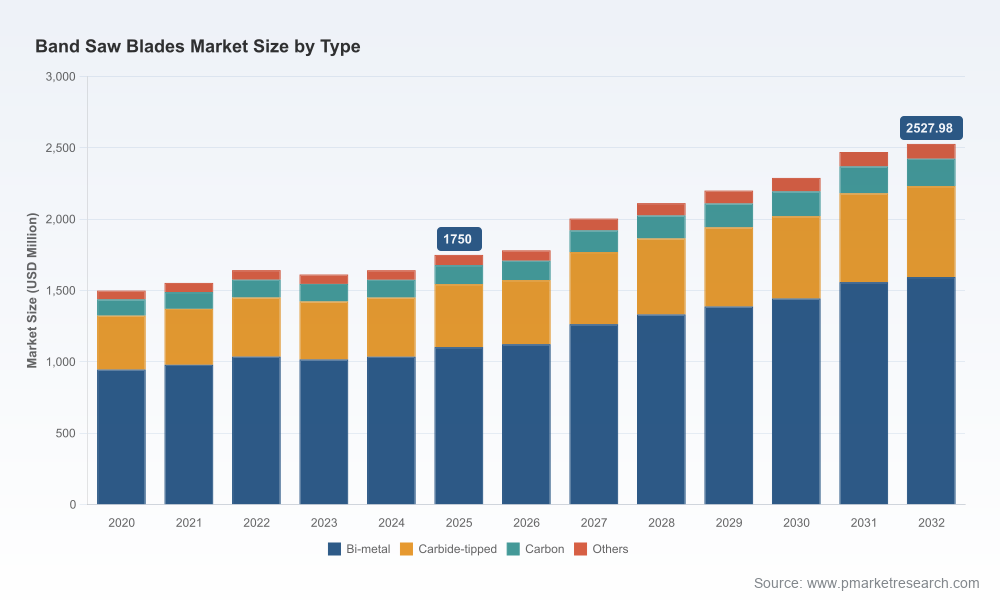

The global band saw blades market is at an inflection point. After recovering from pandemic-era distortions, the industry reached an estimated market size of approximately USD 1,750 Million in the base year (2025). Our forecast model, built on a combination of bottom-up shipment data, supplier intelligence, raw-material price trajectories, and end-market demand indicators, projects steady expansion across the 2026–2032 horizon at a compound annual growth rate (CAGR) of 5.5%, culminating in an approximate market value of USD 2,528 Million by 2032.

Band Saw Blades Market

For executives planning 2026 investments—whether capital allocation, sourcing, product development, or M&A—this market profile delivers three immediate strategic imperatives:

Band Saw Blades Market

- Protect margins from raw-material volatility and supply-chain disruptions.

- Differentiate through product-system solutions (coatings, tooth geometry, integration with automated sawlines) rather than blade commodity pricing alone.

- Prioritize aftermarket, services and digital-enabled maintenance offerings as high-margin growth levers.

What the report delivers (operationally actionable)

Our full study is organized to convert insight into action. Key deliverables include:

- Market sizing and validated forecast models (2026–2032) with scenario sensitivity to steel alloy and strip-steel price shocks.

- Demand-driver diagnostics across primary end-markets (metalworking, woodworking, food processing and others) and a detailed decision tree for prioritizing channel investments.

- Supply-side analysis including capacity maps, raw-material exposure matrices, and a supplier risk heatmap tied to logistic lanes and concentration risk.

- Technology and product benchmarking: comparative profiles for bi-metal, carbide-tipped, carbon and advanced specialty blades—covering life-cycle cost models, ideal application envelopes and retrofit recommendations for saw OEMs.

- Commercial playbooks: pricing architecture, distributor segmentation, tender response templates and a one-page ROI tool for CAPEX decisions on blade automation and band-saw line upgrades.

- Strategic M&A checklist and valuation multiples observed in the last 36 months for blade and blade-adjacent tooling companies.

- Regulatory and compliance playbook—including CE and ISO 9001 implications on market access, and recommended inspection/tension-testing protocols to reduce liability.

Each element is supported by primary interviews, trade-show intelligence, and supplier-verified production data. Crucially, the report embeds an easily deployable supplier-selection scorecard and an inventory-hedging planner designed for procurement teams to operationalize within 60–90 days.

Industry dynamics to watch in 2026

- Raw-material volatility: High-carbon strip steel and various high-speed steel alloys remain the dominant cost drivers. Our sensitivity models show that short-term price spikes materially compress margins unless manufacturers adopt hedging, pass-through pricing structures, or higher-value coatings that justify premium pricing.

- Regulatory and quality thresholds: Both EU and US safety standards, including mandatory periodic inspection and tension testing, create a compliance floor that favors established suppliers with documented quality systems. ISO 9001 and CE conformity are not optional for firms targeting industrial metal-processing customers.

- Demand composition change: Metalworking demand continues to consume the majority of industrial blade output, but high-growth niches—higher-precision metal fabrication, composite-cutting for aerospace and advanced wood-processing lines—are where blade manufacturers can capture premium ASPs and extended warranties.

- Consolidation and concentration: Market concentration is meaningful: the top three players account for roughly two-thirds of market share, and the top five approach three-quarters. This creates both risk and opportunity: suppliers with scale benefit from purchasing leverage and distribution reach, while well-focused specialists can command margins in niche segments.

- Technology shift to system solutions: Tooth geometry optimization, advanced heat treatments, carbide-tipped technology, and coatings now determine total cost of ownership more than simple steel grade. Buyers are increasingly procuring blade-and-service bundles (installation, sharpening schedules, predictive-replacement alerts).

Competitive landscape — what leading players signal for strategy

The sector is populated by several established manufacturers and regional specialists. Our competitive analysis synthesizes public filings, trade-show activity and product releases through early 2026, and identifies play patterns worth noting for 2026 strategy:

- WIKUS (Spangenberg, Germany): Europe’s largest band saw blade manufacturer continues to leverage trade-show presence and flagship product launches to deepen OEM partnerships. Recent selection of premium blades for ultra-large saw platforms and consistent trade-fair visibility signal an emphasis on system sales and thought leadership. For competitors, WIKUS’ approach underscores the need for platform-based value propositions and co-development agreements with saw OEMs.

- The L.S. Starrett Company (USA): Starrett’s positioning on precision and tooth-geometry engineering indicates a premium-market strategy focused on diversified end-markets (metals, plastics, composites). Companies targeting high-precision OEMs should evaluate technical partnerships or licensing of proprietary tooth profiles.

- M. K. Morse (USA): Morse’s focus on heavy-structure and high-production applications highlights an opportunity in the heavy-industrial segment where durability and lifecycle cost dominate procurement decisions.

- ARNTZ and Pilana (Germany/Czech Republic): Both firms’ updated catalogs and product roll-outs in 2025–2026 point to continued innovation in carbide-tipped offerings; expect intensified competition on engineered solutions for construction materials and industrial metals.

- Bahco and DoALL: These global players continue to emphasize broad product-range strategies, leaning on distribution networks and standardized product families—an effective defense for maintaining share in mid-market accounts.

- Regional producers (China, specialized German manufacturers, and US legacy firms): A two-track competitive dynamic is emerging: low-cost suppliers competing on price and availability, and regional specialists leveraging fast local service, shorter lead times and certification credentials.

Practical strategic moves for 2026

Based on our modeling and client engagements, we recommend the following priority actions for firms seeking to win in 2026:

- Hedge and reprice smartly: Establish medium-term raw-material contract coverage and develop transparent surcharge mechanisms tied to steel-alloy indices. Combine this with SKU rationalization to reduce exposure on low-margin products.

- Shift toward system sales: Re-bundle blades with services—installation, sharpening contracts, predictive replacement and extended warranties—to lift gross margin and lock customer relationships.

- Invest selectively in certification and traceability: Prioritize ISO 9001 and CE compliance where it unlocks large industrial accounts, and add traceability (batch-level metallurgy records) for high-end metalworking customers.

- Targeted portfolio optimization: Focus R&D on blade technologies that offer measurable life-cycle cost advantages (tooth design, coatings, carbide compositions) rather than incremental improvements to commodity blades.

- Forge OEM co-development agreements: Embed blades earlier in sawline designs to capture system margins and create switching costs for end-users.

- Explore bolt-on acquisitions: Look for regional service-centric players or capability-add targets (e.g., mobile blade sharpening, specialized carbide operations) to accelerate aftermarket coverage.

Risk matrix and near-term watchlist

Top operational risks for 2026 include raw-material cost shocks, logistic congestion in critical supply corridors, and faster-than-expected shifts in end-market demand (e.g., a slowdown in heavy manufacturing). Mitigants include forward-purchasing programs, multi-sourcing strategies, and expanding aftermarket service lines to stabilize cash flow.

Regulatory developments—especially updates to inspection and safety mandates in core end-markets—can materially affect service requirements and warranty exposure. Firms should maintain active engagement with standards bodies and include compliance-cost scenarios in procurement decision gates.

How to use the full report

This briefing highlights strategic conclusions and operational playbooks from our Band Saw Blades Market research. The full report contains the proprietary segmentation tables, downloadable forecast model (editable in Excel), supplier scorecards, and detailed company profiles with recent strategic moves and trade-show intelligence. To execute the tactical recommendations above—supplier negotiations, product prioritization, and M&A diligence—you will need the full dataset and scenario models.

PW Consulting’s clients receive tailored workshops that translate the study into 90-day implementation roadmaps—complete with KPIs, supplier negotiation scripts, and a procurement-hedging calendar. For access to the complete report, interactive models, and client workshop scheduling, please visit the PW Consulting research portal.

Closing perspective

The band saw blades industry in 2026 rewards scale, technical differentiation and service-enabled monetization. With an overall market projected to expand at a 5.5% CAGR through 2032, executives have the runway to invest in higher-margin solutions, forge deeper OEM ties, and reduce commodity exposure. The right combination of procurement discipline, product engineering and aftermarket focus will define winners over the next strategic cycle.

For detailed analysis of this topic, please visit the official page:Band Saw Blades Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com