Cat Litter Market 2026: Strategic Imperatives for Decision‑Makers — A PW Consulting Industry Brief

As firms prepare budgets, product roadmaps, and M&A pipelines for 2026, the global cat litter market presents a rare combination of steady growth, concentrated supplier dynamics, and accelerating product and regulatory complexity. PW Consulting’s full Cat Litter Market study (base year 2025, historical window 2020–2025, forecast 2026–2032) synthesizes macro trajectories, competitive positioning, operational playbooks, and regulatory risk to help executives convert market signals into defensible strategic moves. Below, I summarize the study’s most consequential insights — enough to shape boardroom debate, but intentionally high‑level to preserve the proprietary segmentation and tactical levers contained in the full report.

Cat Litter Market

Market Trajectory at a Glance

The market has delivered resilient expansion through the pandemic recovery period and into 2025, rising from a global industry measured in the mid‑single‑digit billions (USD) in 2020 to an appreciably larger base by 2025. PW Consulting projects continued expansion through our 2026–2032 forecast horizon at a compound annual growth rate (CAGR) of approximately 5.5%, with the market size progressing steadily year‑over‑year under a combination of structural and discretionary drivers.

Cat Litter Market

- Structural demand: persistent pet adoption trends, increasing premiumization (odor control, dust reduction, biodegradable options), and the ergonomics of automated litter systems.

- Channel evolution: rapid e‑commerce penetration, subscription models, and continued importance of big‑box retail for household penetration.

- Input dynamics: raw material cycles (mineral vs. plant‑based inputs), supply chain concentration, and evolving sustainability mandates.

Why this Matters for 2026 Decisions

For 2026 planning, leaders must treat the cat litter market as a mature but active sector where modest aggregate growth masks high tactical variability. The macro growth rate provides a stable backdrop for investment, but three convergent vectors should sharpen priorities this year:

Cat Litter Market

- Margin pressure from input inflation and freight volatility — requiring procurement sophistication and SKU rationalization.

- Regulatory and reputational tailwinds toward safer, traceable supply chains and eco‑friendly formulations — increasing product development and compliance spend.

- Retail and digital tradeoffs — investments in D2C capabilities and subscription economics can materially shift lifetime value and reduce shelf dependency.

Competitive Structure and What It Means Strategically

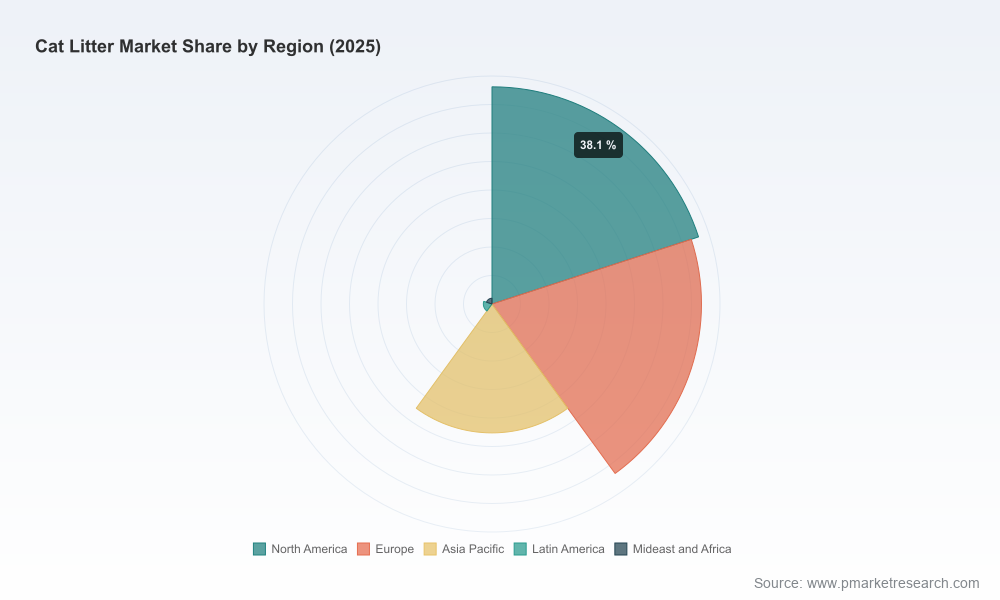

The competitive landscape is characterized by a moderate degree of concentration: the top three suppliers hold roughly 60% of market value, and the five largest players account for about three quarters of the industry. That concentration creates both barriers and openings:

- For incumbents (global bentonite and mineral producers, established branded manufacturers): scale enables negotiating leverage on raw materials and distribution, but scale also brings visibility and regulatory scrutiny.

- For challengers (specialist silica gel producers, plant‑based innovators, local OEMs): focused product differentiation and nimble supply chains allow faster entry into premium and niche segments, especially where sustainability or automation compatibility matters.

- For private label and retail brands: opportunities exist to capture higher margins via exclusive formulations and subscription bundles, but require investment in quality control and supply assurance.

Key companies to watch (profiles included in the full study) span established chemical and mineral manufacturers, legacy household brands, and a growing cohort of specialized, plant‑based producers. Examples include multi‑national bentonite leaders, large consumer packaged goods (CPG) players with national retail distribution, silica gel specialists focused on moisture and odor control, and numerous China‑based OEMs driving cost‑competitive and eco‑friendly innovations.

Recent Developments: Regulatory & Safety Signals

2025–early‑2026 activity underscores the operational and reputational risks that must be actively managed in 2026:

- Product safety and recall events prompted heightened regulator attention; regulatory agencies have elevated some pet product recalls and tightened classification standards. For manufacturers and distributors, this has translated into faster escalation timelines and a higher bar for documentation and storage practices.

- Trade shows and product launches during 2024–2025 revealed rapid iteration in plant‑based and automatic‑litter‑box‑compatible formulations, signaling where R&D budgets are heading.

Those developments are not theoretical. They affect sourcing, distribution contracts, and the speed of product introductions. The most prudent players are treating compliance and traceability not as cost centers but as value protectors for brand equity and channel access.

Operational Playbook: Actions to Prioritize in 2026

Pilots and investments should be prioritized with an eye toward measurable returns within 12–24 months. The full PW Consulting report provides templates and cost/benefit matrices for each of these actions; high‑level priorities include:

- Supply resilience: diversify mineral and plant‑based suppliers, implement dual sourcing for critical inputs, and establish part‑number level traceability across contracts.

- Quality and compliance: adopt tighter GMP‑style storage protocols, increase batch testing frequency, and conduct third‑party audits focused on contamination risks.

- Product portfolio optimization: rationalize slow movers, accelerate premium SKU launches that fit subscription economics, and test automated‑litter‑box compatibility as a product requirement.

- Channel and pricing: pilot D2C subscription offers with variable‑frequency bundles, and model price elasticity across premium vs. commodity SKUs to protect margin while growing share.

- Sustainability roadmap: prioritize bio‑based formulations and recyclable packaging where payback can be demonstrated via higher ASP or channel support.

Competitive Moves to Anticipate

Expect three broad categories of activity from competitors and partners in 2026:

- Portfolio extension by incumbents: large mineral and CPG players will continue to add premium or eco alternatives through JV, acquisition, or in‑house development to defend shelf space.

- Scale plays by regional OEMs: China‑based and regional producers will escalate private‑label offers and OEM capabilities to capture global export demand, especially for price‑sensitive channels.

- Verticalization by digital challengers: companies that control D2C channels will integrate logistics and subscription management to optimize customer lifetime value and data capture.

M&A, Partnerships and Capital Allocation Considerations

With a mid‑single‑digit CAGR and a concentrated supplier base, M&A activity in 2026 will follow pragmatic themes:

- Fill‑the‑capabilities targets — bolt‑on acquisitions that offer biodegradable tech, odor‑control IP, or automated‑litter‑compatibility will command premiums.

- Supply chain investments — strategic stakes in raw material mines, silica processors, or plant‑based input producers can be the difference between margin compression and insulation.

- Commercial scale partnerships — exclusive distribution arrangements and co‑branded subscription initiatives are lower‑risk ways to expand reach without heavy CAPEX.

Risk & Regulatory Radar for 2026

Operational risks are now amplified by public health and regulatory expectations. Specific, actionable risk mitigants include:

- Enhanced inbound controls: sanitary storage certifications, supplier hygiene audits, and digital chain‑of‑custody documentation.

- Recall playbooks: pre‑established communications, logistics recall corridors, and insurer‑aligned response strategies to reduce financial and reputational fallout.

- Regulatory monitoring: active tracking of agency guidance in principal markets and pre‑emptive alignment with voluntary standards to avoid abrupt compliance costs.

What the Full PW Consulting Report Delivers

Our full Cat Litter Market study is designed for immediate operational use and strategic planning. It includes:

- Detailed historic and forecast market sizing (2020–2032) with scenario modeling calibrated to raw‑material price paths and channel shifts.

- Granular segmentation by product type, raw material and region (this is where the report’s tactical intelligence resides — accessible via the full document).

- Competitor profiles, SWOT analyses, and value‑chain maps for leading players and emergent challengers.

- Commercial playbooks: go‑to‑market templates, D2C subscription economics, retail negotiation levers, and private label playbooks.

- Operational checklists for quality, storage, and recall readiness, plus a regulatory timeline and compliance cost estimates.

- Investment and M&A modeling tools, including acquisition screening criteria and integration scorecards.

How to Use These Insights in 2026 Planning

Translate the macro stability and the 5.5% CAGR into concrete boardroom actions:

- Set capital allocation to preserve optionality — fund one high‑return pilot (e.g., D2C subscription), one supply‑chain de‑risking initiative, and one product‑innovation sprint focused on sustainability or automation compatibility.

- Align procurement and R&D timelines — secure long‑lead raw materials contracts while accelerating formulation tests to hit retailer buying cycles.

- Measure and monitor — adopt a small set of leading indicators (inventory days by SKU tier, recall lead time, D2C churn) to inform quarterly course corrections.

Final Word

The cat litter market in 2026 is neither a complacent commodity nor a high‑volatility frontier. It is a sector where disciplined strategy — applied to product portfolios, supply chains, and channel economics — will differentiate winners from the pack. PW Consulting’s full report provides the segmentation‑level, transaction‑ready intelligence and operational templates that enterprises require to convert the sector’s predictable growth and concentrated structure into superior returns. For teams preparing 2026 plans, the priority is clear: invest in resilience, test for premium differentiated offerings, and make data‑driven channel decisions that lock in customer lifetime value.

Access the full study for the segmented market tables, company scorecards, playbooks, and downloadable financial models that underpin these recommendations.

For detailed analysis of this topic, please visit the official page:Cat Litter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com