Painting Spray Guns Market Research Industry: Key Success Factors

Other |

2026-04-07 09:15:01

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused, decision-grade preview of our comprehensive Semiconductor Photomask Market study. This briefing is crafted as a strategic trailer: it surfaces the analytic depth, structural drivers, and high‑impact implications executives must weigh in 2026 — while intentionally omitting granular segment tables and proprietary datapoints reserved for the full report.

Semiconductor Photomask Market

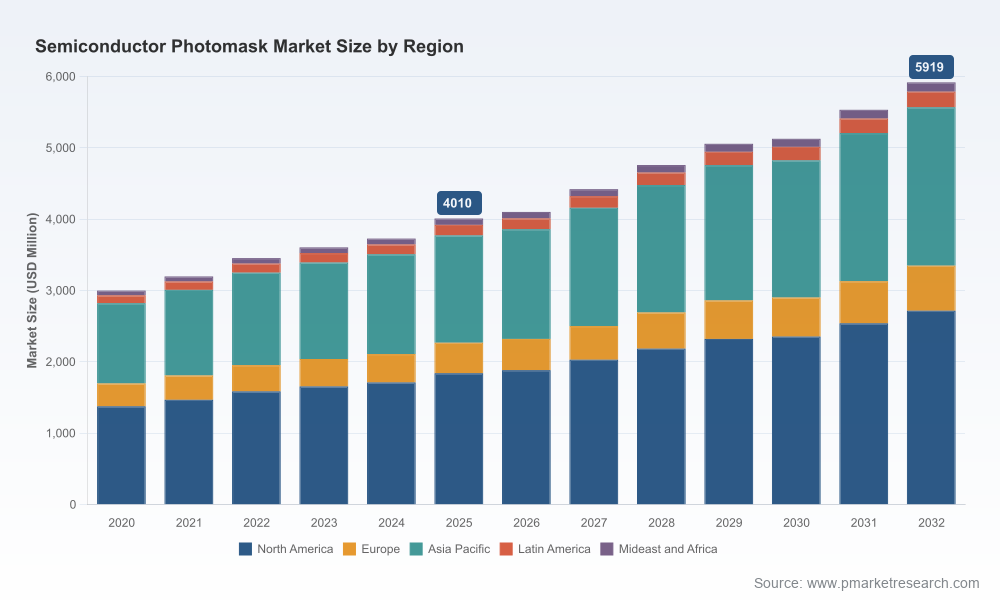

Photomasks remain a critical, high‑value node in the semiconductor value chain, linking lithography systems to wafer production and therefore to device performance, yield and cost per node. Between 2020 and 2025 the market expanded from a clear mid‑market base to a materially larger, more diversified industry. Our baseline (2025) valuation shows the market at roughly USD 4.01 billion (Million‑unit reporting convention), and PW Consulting’s forecast through 2032 anticipates continued, steady growth to approximately USD 5.92 billion by 2032 — a multi‑year compound annual growth rate of about 5.8% across the forecast window (2026–2032).

Semiconductor Photomask Market

Resilience with selective acceleration: The mid‑single‑digit CAGR conceals important heterogeneity — while aggregate demand climbs steadily, pockets of disproportionate upside exist around advanced nodes, EUV mask blanks, and display photomasks tied to next‑generation panel formats.

Semiconductor Photomask Market

Capital intensity and lead times matter: Capacity additions, EUV‑capable production lines, and high‑purity substrate sourcing require multiyear lead times and tight capex planning. Firms that front‑load investments aligned to 2027–2029 demand inflection points will capture premium ASPs and strategic customer relationships.

Margin pools are being reallocated: Technological specialization (EUV, 7nm and below reticles, high‑precision master masks) and vertical integration into mask blanks are concentrating higher margin pools among suppliers with advanced R&D and cleanroom footprints.

Capacity and customer alignment: For IDM and foundry purchasers, lock‑step alignment with a small set of qualified merchant suppliers is necessary to secure advanced node supply. Procurement strategies should prioritize multi‑year offtake contracts and technical co‑development agreements for EUV and high‑NA roadmaps.

Supplier risk management: With reported supply constraints on specialty raw materials (notably high‑purity quartz and related substrates), buyers must adopt dual‑sourcing strategies and consider strategic inventory buffers for critical mask blank inputs.

Capex sequencing: Photomask producers should rationalize capital allocation toward EUV capability, automation of reticle inspection, and yield‑improving metrology — investments that compress time‑to‑qualify for hyperscaler and advanced logic customers.

M&A and JV playbook: The market’s structure rewards scale in advanced segments. Expect continued deal activity around technology tuck‑ins (EUV toolsets, metrology), regional footprint expansion, and mask blank vertical integration.

Our full study goes well beyond high‑level trends to deliver practical, executable intelligence for 2026 planning cycles. Highlights include:

Market sizing and trend decomposition across a 2020–2032 horizon (base year 2025), with scenario modeling that stresses node‑specific demand, display panel cycles, and MEMS/optical device pockets.

Quantitative demand drivers and sensitivity analysis: elasticities to wafer starts, lithography node migration curves, equipment cadence, and ASP evolution under multiple supply/demand scenarios.

Supplier scorecards and qualification matrices: capability assessments, facility footprints, R&D roadmaps, and readiness for EUV/high‑NA transitions (commercially restricted data and performance rankings are in the full report).

Capex and working capital templates: tailored models to stress‑test investment timing, break‑even horizons and ROI for greenfield expansions vs. capacity upgrades.

Commercial playbooks for buyers and suppliers: negotiation levers, preferred contracting terms, co‑investment structures, and strategies to mitigate raw material bottlenecks and regulatory disruption.

Regulatory and geopolitical risk overlays: scenario playbooks addressing tariffs, export controls and subsidy regimes, with recommended contingency actions and timeline triggers.

The market’s competitive structure is characterized by a mix of merchant specialists, regional champions and mask‑blank focused suppliers. Leading firms combine global fabrication networks, advanced EUV capabilities, and deep customer relationships in logic, foundry and display segments. Key strategic profiles we analyze in depth include:

Photronics Inc. — a merchant leader with a global footprint across North America, Asia and Europe; ongoing investments in U.S. and South Korean facilities make it a pivotal supplier to advanced logic and specialty application customers.

Tekscend Photomask (rebranded from a legacy Japanese player) — an increasingly global manufacturer with targeted expansions in the Americas and Southeast Asia aimed at advanced precision masks for logic and foundry demand.

Dai Nippon Printing (DNP) — with R&D investments and product offerings positioned for the cutting edge of EUV lithography nodes, DNP is a strategic provider for customers migrating to 3nm/2nm class processes.

Hoya Corporation — a dominant supplier in the mask blank segment, controlling critical upstream inputs that influence the economics and availability of EUV masks.

SK‑Electronics and selected regional suppliers — significant players in regional supply chains and mask blank distribution who matter to buyers seeking diversified sourcing and local support.

Recent corporate initiatives analyzed in the report — facility groundbreakings, equipment ramp‑ups and public statements about investments — demonstrate that suppliers are moving to secure both capacity and technology leadership. PW Consulting’s company profiles synthesize strategic intent, execution risk, and partnership opportunities for each named player.

Trade and export policy: New tariffs and export control measures have introduced tangible procurement friction and compliance costs. Our regulatory matrix maps these changes to sourcing and qualification timelines so procurement teams can quantify the tradeoffs of geographic diversification versus supplier consolidation.

Government incentives and industrial policy: Subsidy programs and national semiconductor strategies materially affect capital availability and the economics of local production. The report evaluates how incentive timing and conditionality should influence capex sequencing and facility location decisions.

Raw material constraints: A meaningful share of manufacturers report constraints on high‑purity substrate inputs. The report provides mitigation paths — from supplier development to vertical partnerships and strategic inventory management — prioritized by impact and implementation lead time.

For semiconductor OEMs and foundries: formalize multi‑year offtake and joint development agreements with at least two qualified photomask partners, incorporate contractual SLAs for yield and delivery, and fund targeted co‑development for node migration timelines.

For photomask manufacturers: prioritize investments in EUV readiness, metrology automation and yield analytics. Consider strategic alliances for mask blank security and explore government co‑funding where available to de‑risk greenfield capacity.

For investors and private equity: focus on technologies that reduce qualification time and raise switching costs (advanced inspection, pellicle technologies, mask data preparation IP) and evaluate consolidation plays that acquire capability and customer access versus pure capacity buys.

For policymakers and regional planners: align incentive structures with technology roadmaps, ensure supply chain traceability for critical substrates, and coordinate export control timelines with industry stakeholders to avoid unintended supply shocks.

Use our forecast scenarios to stress‑test board‑level capital allocation and procurement commitments. Prioritize three near‑term actions this year: (1) run supplier stress tests against regulatory and material‑supply scenarios; (2) fast‑track qualification roadmaps for at least one secondary supplier; and (3) align internal capex approval cycles with the product node roadmaps of your key customers or suppliers. PW Consulting’s models provide the numerical inputs and scenario triggers to operationalize each action.

This preview outlines the strategic contour of the Semiconductor Photomask Market in 2026 but intentionally omits the granular segmentation tables, per‑region/application shares, and proprietary supplier scoring that will determine exact contract terms and investment sizing. For the complete dataset, detailed supplier matrices, and bespoke scenario modeling tailored to your portfolio or procurement footprint, access the full PW Consulting report and associated advisory services on our site.

PW Consulting’s full deliverable equips C‑suite leaders and supply‑chain managers with the actionable models, negotiation playbooks, and regulatory impact assessments required to convert photomask market dynamics into durable strategic advantage in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Semiconductor Photomask Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com