Surge Protection Device (SPD) Market — A Strategic Preview for 2026 Decision-Makers

Executive snapshot

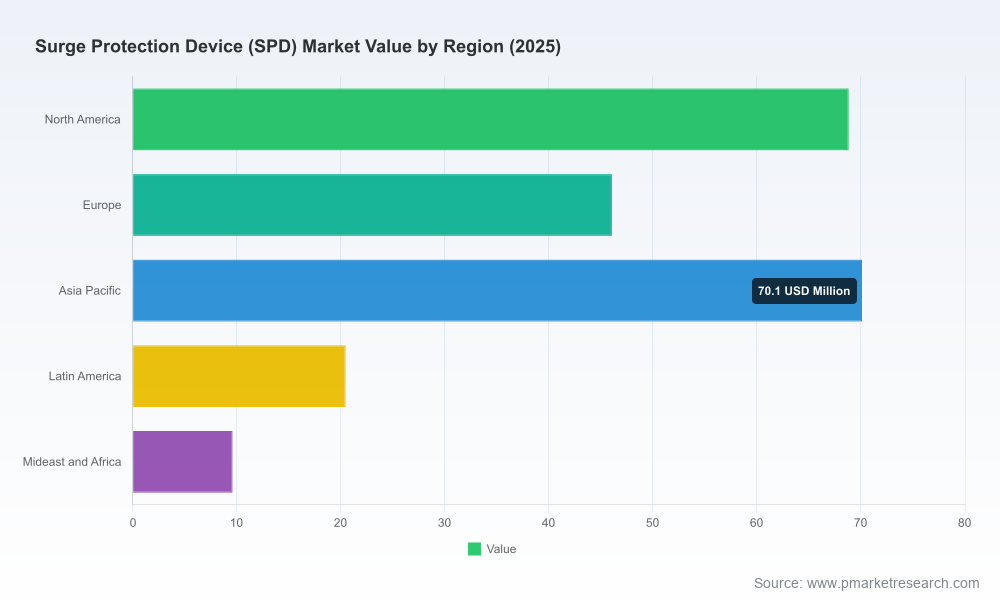

As organizations accelerate investments in resilience, power quality and distributed energy, the global Surge Protection Device (SPD) market is tracking a steady expansion. Using 2025 as our base year, PW Consulting projects the market to grow from roughly USD 215 million in 2025 to an expected USD 345 million by 2032 — a compound annual growth profile of approximately 7% over the forecast horizon. Our historical review (2020–2025) and forward-looking analysis (2026–2032) combine to create an operational planning tool that translates macro momentum into actionable 18–36 month priorities for procurement, R&D, channel strategy and M&A consideration.

Surge Protection Device (SPD) Market

Why this preview matters for 2026

- Near-term capital cycles: For many enterprises and electrical OEMs, 2026 is the inflection year to decide on product roadmaps and supplier lock-ins that will govern the next procurement cycle.

- Regulatory timing: Fresh and updated standards have taken force or are imminently active; 2026 is the first practical planning window to implement compliant designs and warranty/maintenance programmes.

- Commercial opportunity: The combination of rising distributed generation, EV infrastructure, and stricter facility uptime requirements creates discrete commercial openings for product+service bundles that capture lifecycle revenue.

What the full PW Consulting report delivers (practical highlights)

- Transparent market architecture and methodology: reproducible sizing from 2020–2025 and granular forecasting for 2026–2032 with scenario variants.

- Channel and route-to-market playbooks: decision trees for OEMs, panel builders, electrical contractors and distributors — with margin mechanics and service models for each.

- Regulatory and standards matrix: mapping UL 1449 (EOL visibility) and IEC 61643 updates against product design, test requirements and certification timelines.

- Supplier scorecards and capability heatmaps: comparative 360° assessments on product breadth, monitoring features, form-factor innovation, certification footprint, manufacturing scale and aftermarket readiness.

- Unit-cost and landed-cost models: embedded templates to stress-test pricing, labour and materials scenarios under raw-material inflation and logistics volatility.

- Commercial sizing models by product architecture and use-case: downloadable models for revenue and unit-demand planning (note: this preview intentionally omits detailed splits — full access unlocks the granular hallmarks buyers and strategists require).

- M&A and partnership shortlists: target profiles and near-term catalysts for consolidation or capability acquisition given current market concentration dynamics.

Market structure and concentration — strategic implications

The SPD market remains structurally fragmented. The combined share of the top-tier incumbents is modest relative to total market size, indicating material runway for innovation-led share shifts, premiumisation in safety-critical segments and bolt-on acquisitions that can quickly uplift distribution reach or technical differentiation. Low top-line concentration creates choice for buyers but also places a premium on product certification, field reliability and service economics as decisive procurement variables.

Surge Protection Device (SPD) Market

Key themes shaping supplier and buyer strategies

- Standards-driven product design: UL 1449 5th Edition’s explicit requirement for end-of-life visibility is no longer aspirational. Manufacturers embedding clear EOL signalling and remote indication into SPDs reduce long-term maintenance risk and win spec-driven projects.

- IEC performance updates: The IEC 61643 refresh has raised the performance bar for low-voltage AC SPDs. Compliance now splits the market between legacy offering holders and firms whose R&D has internalised the new performance envelope.

- Integration and system-level differentiation: The most commercially successful products are migrating from standalone devices to integrated, monitored modules inside distribution boards, switchgear and critical power systems — enabling upsell of monitoring, predictive maintenance and warranty extensions.

- Service economics and installation friction: Professional installation and periodic maintenance remain a material cost component. Where installers or end-users perceive high service friction, uptake of premium SPDs can be suppressed; conversely, bundled installation and monitoring services increase lifetime value.

- Input-cost pressure and pricing discipline: Energy and raw-material inflation is filtering through supply chains. Firms that protect margins via design choices, supplier hedging and operational efficiency will be best positioned to defend share without destroying demand.

- Form-factor innovation: Narrow, pluggable modules for control/measurement circuits and robust, high-SCCR units for industrial switchgear are both growth vectors. Innovations that lower footprint or simplify retrofit unlock channel momentum.

Competitive map — what incumbents are doing

We benchmarked leading names across product, certification, monitoring capability and channel readiness. Summarised below are the strategic postures and recent moves that will influence 2026 contracting and procurement decisions.

Surge Protection Device (SPD) Market

- Schneider Electric (Rueil‑Malmaison, France) — Strategy: product-system integration and panel-ready SPDs with attention to installation simplicity and monitoring. Notable move: in late 2025 Schneider launched an integrated Type 2+3 plug-in SPD for their Acti9 and KQ distribution platforms featuring end-of-life monitoring and remote indication — a clear play to capture spec-based commercial projects and panel OEM relationships.

- ABB Ltd (Zurich, Switzerland) — Strategy: broad modular portfolio across Type 1–3 with industrial-grade ranges. ABB’s value is in modularity and compliance breadth, making them a default for system integrators that need catalogue depth and CE/UL alignment.

- Siemens AG (Munich, Germany) — Strategy: system-integrated protection with an emphasis on ground-reference monitoring and residential/commercial product families. Siemens’ BoltShield family exemplifies their push to embed monitoring into low-voltage switchgear, serving spec-driven commercial builds.

- Eaton Corporation plc (Dublin, Ireland) — Strategy: high-SCCR integrated solutions for power distribution and UPS ecosystems. Eaton competes on electrical ruggedness and compatibility within power systems where short-circuit ratings and UL compliance matter to procurement engineers.

- Mersen SA (Paris, France) — Strategy: thermal-protected MOVs and fail-safe disconnection options aimed at industrial and residential safety-conscious buyers. Recent technical literature updates reflect alignment to the latest UL/NEC interpretations — a signal that technical marketing is being used to influence specifications.

- Phoenix Contact (Blomberg, Germany) — Strategy: ultra-narrow pluggable modules and protection for measurement/control layers. Their TERMITRAB series extensions for process automation and hazardous-area connectivity are targeted at industrial Ethernet and fieldbus protection markets.

Recent industry developments to note

- Product launches and portfolio extensions in 2025–2026 show incumbents racing to embed EOL visibility, remote indication and pluggable convenience into mainstream catalogues.

- Technical literature and brochure updates from market players reflect the operational need to reassure buyers on compliance with the latest UL and NEC interpretations.

- Manufacturers targeting process automation and hazardous-area applications are expanding addressable markets beyond traditional power-distribution segments.

Immediate strategic actions for 2026 (recommended playbook)

- Prioritise compliance-led product changes: if your product set lacks clear EOL signalling and remote monitoring, make that a Q1–Q2 design priority to capture spec-based tenders.

- Design for serviceability: simplify installer workflows and create bundled maintenance offers. Professional installation currently adds noticeable per-unit cost; converting this into a managed service can increase lifetime revenue.

- Lock in supply and hedges for key raw materials: plan for material-cost pass-throughs and protect margin via multi-sourcing or vertical integration where scale permits.

- Differentiate via integration: partner with distribution board and switchgear OEMs to create certified integrated SKUs — integration shortens procurement cycles and raises switching costs for buyers.

- Pursue bolt-on acquisitions or alliances if your strategy requires rapid capability expansion: the market’s moderate concentration means M&A can quickly unlock distribution or technical features absent in your base offering.

- Invest in monitoring and digital services: remote indication, fault logging and simple cloud-enabled alerts turn a commodity device into a recurring-revenue asset.

Using the full PW Consulting study

This preview was created to surface the strategic signals that matter for 2026 — unit economics, regulatory timing, supplier moves and service opportunities. The complete PW Consulting SPD Market study contains the granular segmentation and downloadable modelling templates that procurement teams, product strategists and corporate development groups need to act with precision. Our full deliverable includes regional and product-type demand curves, unit-price elasticity testing, supplier due‑diligence templates and an M&A target shortlist calibrated against capability gaps.

Next steps

For teams aligning 2026 budgets and 3‑year roadmaps, we recommend three immediate steps: (1) download the full study to access the granular segmentation and scenario models, (2) run a 90‑day supplier and product compliance audit against UL 1449 and IEC 61643 updates, and (3) convene a cross-functional rapid response team (product, procurement, legal, service) to translate standards-readiness into product and commercial changes before Q3 2026 procurement cycles close.

PW Consulting’s SPD Market study is built to move steering committees from signal recognition to revenue-grade decisions. For access to the full dataset, supplier scorecards and the model kit referenced here, visit our report page or contact our industry practice lead to schedule a tailored briefing for your executive team.

For detailed analysis of this topic, please visit the official page:Surge Protection Device (SPD) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com