Active Protection System Market: Insights, Key Players, and Growth Analysis

Other |

2026-06-29 03:35:28

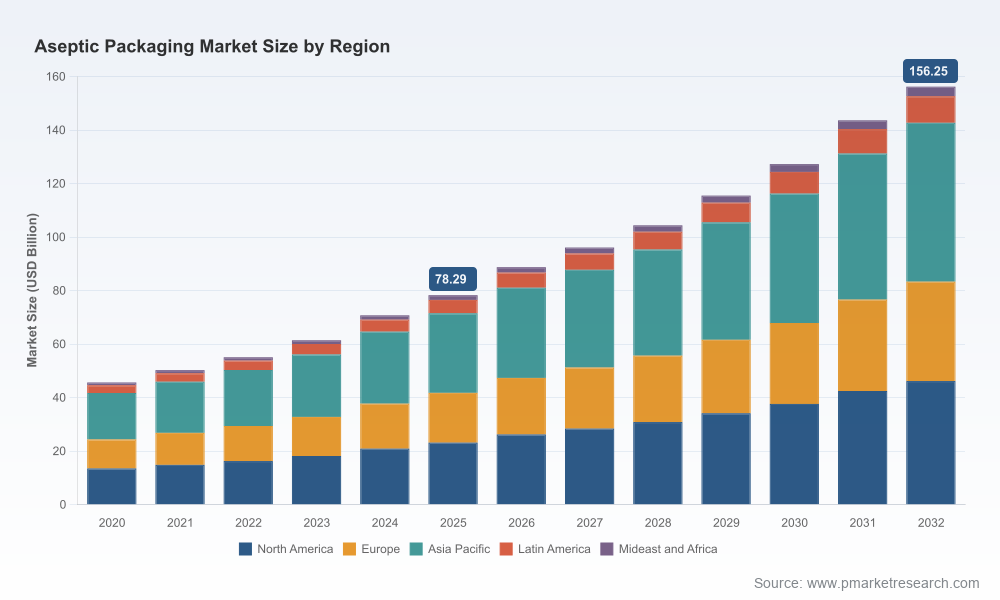

PW Consulting’s latest sector preview highlights why aseptic packaging sits at the intersection of fast market growth, regulation-driven engineering change, and renewed commercial opportunity. The global aseptic packaging market has expanded rapidly — from an estimated USD 45.67 Billion in 2020 to USD 78.29 Billion in our 2025 base year — and is projected to reach roughly USD 156.25 Billion by 2032. Between 2026 and 2032 we model a compound annual growth rate (CAGR) of approximately 10.5%, a dynamic pace that requires executives to convert foresight into concentrated action in 2026.

Aseptic Packaging Market

Regulatory inflection: Mandatory recyclability and design‑for‑recycling rules in major markets (notably the EU’s PPWR regime coming fully into effect in 2026–2028) force rapid technical choices that affect packaging architecture, raw material sourcing, and capex plans.

Aseptic Packaging Market

Sustainability as a commercial pivot: Brand owners are migrating capital and marketing spend toward packaging formats that can demonstrably reduce lifecycle carbon and improve recycling outcomes — creating premium positioning opportunities for vendors with compliant, high‑yield solutions.

Aseptic Packaging Market

Technology and materials substitution: Investments in aluminum‑free barrier technology, mono‑material approaches, and advanced aseptic fillers are shifting the tradeoffs between cost, recyclability, and shelf life.

Market scale and velocity: With market size roughly doubling from 2020 to our 2032 forecast and mid‑single to double‑digit growth in key product families, 2026 will be a high‑leverage year for strategic capex, capacity expansion, and M&A to secure share in high‑growth subsegments.

Robust top‑down sizing and scenario models that track the market from 2020 through 2032, enabling stress tests of price, material cost, and regulatory outcomes against base and upside cases.

Commercial playbooks by customer archetype (global beverage brands, regional dairy groups, pharmaceutical contract packers) that translate market momentum into GTM actions and margin levers.

CapEx decision templates: build versus buy worksheets, payback sensitivity, and greenfield vs brownfield heuristics tailored to aseptic filling and converting.

Supplier and equipment scorecards that rate technology providers across performance, sustainability compliance readiness, geographic footprint, and aftermarket service economics.

Regulatory compliance checklists and design guidelines that map PPWR and similar regional rules to tangible product redesign pathways (e.g., aluminum reduction, mono‑material conversions, and labelling updates).

Supply‑risk heatmaps for critical inputs (coatings, barrier films, sterilization consumables) coupled with mitigation playbooks — from dual sourcing to hedging contracts.

Note on content scope: this preview intentionally highlights strategic implications and methodology while withholding detailed, granular subsegment tables and country‑level projections to preserve the incentive to consult the full report for transaction‑grade data and downloadable models.

Tetra Laval S.A. — A longstanding leader in aseptic carton and filling systems. Recent announced investments in paper‑based barrier pilot capacity signal a strategic bet on aluminum minimization and higher recycling yield. For 2026, watch how pilot outputs influence spec sheets offered to dairy and beverage customers and whether pilot scale accelerates commercial retrofit opportunities.

Amcor plc — Strong in aseptic plastic bottles and extended‑shelf‑life (ESL) solutions. Their portfolio advantage lies in combining barrier engineering with form‑factor innovation; brand owners seeking alternative to cartons will look to Amcor for bottle‑centric ESL solutions that balance shelf life and recyclability.

SIG Combibloc Group AG — Competitive in flexible aseptic bag‑in‑box and carton systems, with targeted product launches into new categories (e.g., camel milk) and capacity expansions in the Americas. SIG’s aluminum‑free rollouts are a live example of a vendor turning regulatory stress into a commercial differentiator.

Elopak AS — Focused on aseptic cartons for dairy and chilled‑stable beverages; Elopak’s strong relations with regional dairy cooperatives make them an essential partner for companies seeking rapid compliance with recyclability mandates.

Greatview Aseptic Packaging — A cost‑competitive supplier with significant scale in rolled and blank‑fed cartons, particularly in Asian markets. Their pricing model and manufacturing footprint will be central to private label and regional beverage strategies in 2026.

DS Smith plc — Provides sterilised transit and secondary packaging solutions that intersect with aseptic supply chains; an important play for brands optimizing overall system recyclability and transport sterilization risks.

Sealed Air Corporation — Advancing flexible pouch formats and aseptic pouch componentry; attractive for liquid food and niche pharmaceutical liquid dosing where reduced material mass and ease of transport are priorities.

Sidel Group — Key supplier of aseptic fillers and PET lines; their equipment roadmaps determine how quickly bottle and PET‑based aseptic fills can be made cost‑competitive and compliant with evolving recycling rules.

Market concentration is moderate: our CR3 and CR5 metrics indicate that the top three and top five producers account for a significant but not overwhelming share of market revenue (CR3 ~42%, CR5 ~45%). This leaves room for regional champions, niche innovators, and new entrants pursuing aluminum‑free barriers and mono‑material formats.

EU PPWR and similar policy movements transform design constraints into product roadmaps. By August 2026 compliance timelines become binding for market access in Europe — requiring fast decisions on aluminum layer minimization and mono‑material adoption.

Aluminum‑free cartons and improved paper‑based barrier systems are moving from pilot to early commercial stages. Vendors that standardize on these solutions stand to capture procurement mandates from large brand owners keen to meet recyclability KPIs.

Filling equipment and aseptic line compatibility remains a gating factor: the cost and downtime to retrofit or replace fillers, sterilizers, and downstream packers should be modelled in any 2026 capex decision. Sidel, Tetra Pak, and others will be the focal points for equipment sourcing negotiations.

Raw material dynamics — from specialty coatings to barrier films — will continue to create periodic cost volatility. Developing preferred supplier agreements and design‑for‑supply clauses will reduce program risk.

Immediate (0–3 months): Run a compliance gap analysis against PPWR and other regional rules; categorize SKUs into ‘no‑regret’ redesigns, ‘managed transition’ SKUs, and ‘strategic holdouts’ (pharma or high‑value beverage applications that require bespoke solutions).

Near term (3–6 months): Initiate pilot partnerships with suppliers offering aluminum‑free or mono‑material solutions; secure pilot capacity with preferred fillers/systems to measure yield, OEE impact, and true total cost of ownership.

Medium term (6–12 months): Reassess capacity and location strategy using PW Consulting’s capex templates; prioritize brownfield retrofits in high‑growth demand corridors and consider targeted acquisitions to fill technology or regional footprint gaps.

Commercial & procurement: Introduce sustainability‑linked contracting for packaging suppliers, and redesign commercial terms to reflect the value of recyclability, reduced end‑of‑life cost, and extended shelf‑life benefits.

Risk management: Lock dual sourcing for critical coatings and barrier films and adopt hedging or inventory buffering for key sterilization consumables.

We translate the market’s top‑line momentum (historic expansion and a projected CAGR of ~10.5% through 2032) into decision‑grade financials and program roadmaps — from product R&D gating criteria to factory modernization sequencing.

Our supplier scorecards and negotiation playbooks are designed to cut RFP cycles and reduce retrofit downtime risk, while our regulatory checklists convert ambiguous policy language into operational deliverables and compliance milestones.

Finally, our M&A screen and JV criteria identify targets (technology holders, regional converters, or equipment specialists) whose acquisition would accelerate time to market for recyclable aseptic solutions.

For senior leaders preparing capital allocation, commercial repositioning, or M&A plans in 2026, the choices made this year will determine competitiveness across a market projected to roughly double within a decade. This preview surfaces the high‑value tradeoffs; the full PW Consulting Aseptic Packaging Market study provides the granular subsegment tables, country‑level forecasts, and downloadable financial models required to execute with confidence. Access the full report and companion toolkits on our PW Consulting report page to convert these strategic imperatives into executable programs.

For detailed analysis of this topic, please visit the official page:Aseptic Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com