What Is Driving Growth in Artificial Intelligence Infrastructure Market Globally?

Networking |

2026-05-11 15:09:22

As PW Consulting’s senior industry analyst, I present a focused market briefing designed to orient corporate strategy for 2026 against the evolving Fructooligosaccharide (FOS) landscape. This is an executive “trailer”: it reveals methodology, directional market sizing and high-impact implications, and demonstrates the analytical depth that underpins our full market study — while intentionally withholding detailed subsegment tables and raw regional splits. Use this note to align near‑term choices (product roadmaps, supply‑chain commitments, M&A posture, clinical investments) to an FOS market expanding at a mid‑single‑digit compound annual growth rate.

Fructooligosaccharide (FOS) Market

Base year and trajectory: Our study uses 2025 as the base year. The FOS market has grown materially since 2020 and is forecast to continue expanding through 2032. Over the 2026–2032 forecast horizon the market grows at a compounded annual rate of 8.25%, reflecting persistent end‑market demand for prebiotic and sugar‑reduction functionalities.

Fructooligosaccharide (FOS) Market

Scale and momentum: After recovering from pandemic-era volatility, the market exhibits sustained expansion into categories that prioritize gut health, clean‑label sugar alternatives, and fortified infant nutrition. The trajectory implies a near‑term imperative for capacity planning and commercial alignment: growth is not uniform across uses, but aggregate momentum is clear.

Fructooligosaccharide (FOS) Market

Concentration and competitive signposts: The market is moderately concentrated — the top three and top five suppliers account for meaningful shares of supply — a structural fact that matters for pricing power, access to premium grades, and negotiation of off‑take terms.

Investment timing. With an 8.25% CAGR through 2032, 2026 is a critical inflection point: firms that secure feedstock agreements, expand validated capacity, or lock preferred supply chains now will capture disproportionate share as formulators accelerate launches.

Portfolio prioritization. Product development teams must choose between (a) premium, clinically differentiated FOS claims, (b) cost‑effective commodity grades for large‑volume food and beverage use, and (c) compliant infant‑nutrition blends. Each path has different capital and regulatory timelines.

Regulatory positioning. GRAS notifications and country‑level approvals materially shift addressable segments. Companies should explicitly model varying regulatory windows and tolerance limits into commercial forecasts and time‑to‑market plans.

M&A and partnerships. Moderate market concentration makes strategic partnerships and targeted acquisitions efficient routes to scale, especially for entrants seeking validated infant‑grade supply, proprietary enzymatic processes, or regional manufacturing footprints.

Health‑first consumption trends remain the primary demand engine. Prebiotic function and the ability to support gut health continue to drive adoption across supplements, functional foods, and beverages.

Sugar‑reduction is a persistent commercial motif. FOS is increasingly used as a partial or full replacer to lower added sugar while contributing mouthfeel and fiber claims — a combination that supports multi‑attribute positioning in new product introductions.

Infant nutrition is strategic but regulated. Historical and contemporary regulatory allowances for FOS inclusion in starter and follow‑on formulas create a defendable pathway into a premium, high‑margin segment — provided safety dossiers and tolerance studies are in place.

Clinical evidence matters. Recent academic and industry trials pointing to metabolic and gut‑hormone benefits elevate the value of clinical programs as a route to premiumization. Firms with proprietary clinical data will enjoy superior label claims and customer pull‑through.

Feedstock and process diversity. FOS is produced from multiple feedstocks and processes (inulin extraction vs enzymatic synthesis). Each route has different operating margins, scale economics, and sensitivity to raw‑material cycles.

Production costs and seasonality. High production costs and seasonal variability in chicory root supply remain the recurrent constraints on scalable inulin‑derived FOS. These dynamics create windows of price volatility and incentivize manufacturers to pursue process efficiencies or alternate raw materials.

Capacity investments. Several established players have signaled capacity expansions. Those moves reduce supply tightness risk longer term but also set the stage for competitive pricing tactics in mature applications.

Beneo: A recognized leader with a strong European production base and a robust pipeline aimed at sugar reduction and infant nutrition. Beneo’s strategic investments in capacity and functional ingredient offerings make it a benchmark for premium positioning.

Meiji Holdings: Strategic commercial playbooks in functional confectionery and supplements demonstrate how brand and channel expertise can accelerate FOS adoption in consumer formats.

Cargill and Ingredion: Large ingredient houses leverage broad portfolios and global distribution to bring FOS into mainstream food and beverage formulations; their scale enables rapid customer trials and co‑innovation.

Tate & Lyle: Recent regulatory filings signal an intent to expand addressable infant and conventional food markets — a development that will be a catalyst for product launches and supply agreements.

Galam, Cosucra, Roquette, Quantum Hi‑Tech and others: These firms represent specialized capabilities — either in clinical differentiation, chicory‑derived supply, resistant‑starch blends, or regional scale — and form the competitive fabric that buyers navigate.

Recent milestones to monitor: Regulatory filings and GRAS notices, public clinical highlights, and product launches have accelerated over the last 24 months and materially affect who can supply what, where, and on what claims.

Prioritize regulatory clarity: Map current approvals and pending GRAS outcomes against your commercialization calendar. Adjust launch sequencing to align with confirmatory tolerance studies and labeling permissions.

De‑risk feedstock: Negotiate multi‑year offtakes, explore blended sourcing (inulin + enzymatic), and consider backward integration where feasible to stabilize costs.

Invest in clinical differentiation selectively: Target one or two high‑value clinical endpoints (e.g., metabolic outcomes, infant tolerance) rather than broad but shallow programs.

Design tiered product offers: Build a two‑track portfolio — a price‑competitive grade for mainstream reformulation and a premium, evidence‑backed grade for differentiated launches.

Use M&A tactically: Acquire or partner to secure infant‑grade supply, proprietary process IP, or regional agility rather than broad horizontal consolidation.

Scenario test capacity decisions: Model revenue and margin sensitivity using the 8.25% CAGR baseline and upside/downside demand ropes; include regulatory timing and raw‑material shocks in stress cases.

Proprietary market-size model (2020–2032) with downloadable scenario workbooks and sensitivity levers tied to regulatory, clinical, and commodity drivers.

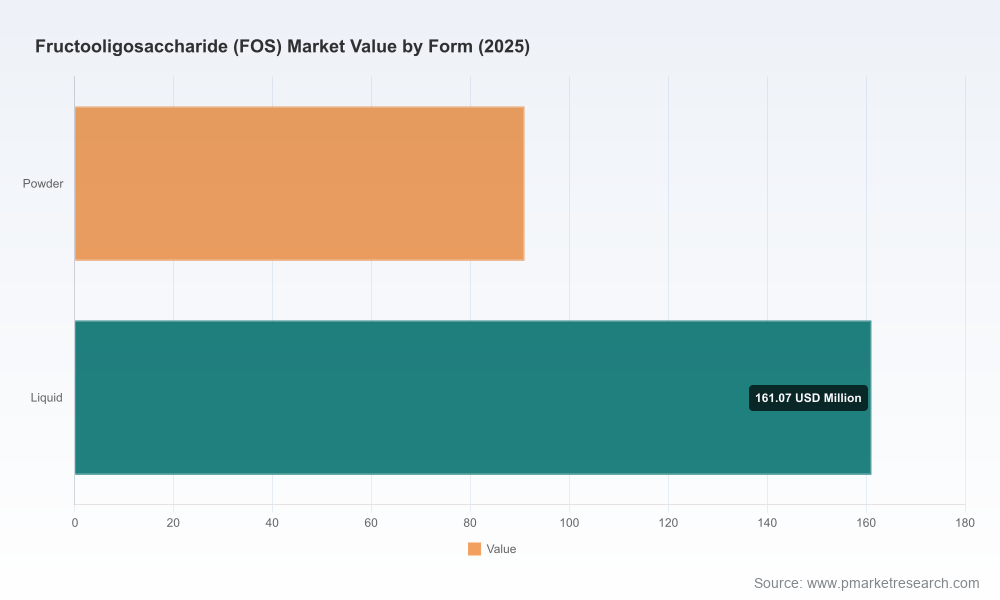

Granular demand forecasts by form, application and region (note: this executive trailer omits the detailed split tables); the full report includes unit and value flows to support capex and commercial planning.

Supplier scorecards and capacity maps that cross‑reference production technologies, validated food‑grade / infant‑grade status and commercial lead times.

Price and margin benchmark curves, cost‑build breakdowns, and a supply‑chain risk matrix (including feedstock seasonality and contract strategies).

Regulatory appendix summarizing GRAS outcomes, tolerance thresholds for infant formulas, key country approvals, and recommended compliance tactics for claim substantiation.

Actionable strategic options and investment cases (M&A targets, partnership screening criteria, and go/no‑go decision trees) that translate insight into capital and commercial choices for 2026–2027.

The FOS market presents a classic opportunity window for 2026: measurable, above‑trend growth, combined with structural supply constraints, accelerating regulatory clarity, and rising value for clinical proof. The single most important strategic posture is to convert market visibility (the 8.25% CAGR and clear growth horizon) into durable commercial advantage — by securing supply, selectively funding evidence generation, and tailoring product tiers to real customer economics.

This briefing intentionally withholds the full disaggregated tables and granular regional/application figures. For teams preparing capital decisions, product roadmaps, or M&A mandates in 2026, the full PW Consulting FOS Market report supplies the operating model, datasets and recommendation matrices required to convert market intelligence into executable strategy. Contact PW Consulting to request the complete report, data model, and a tailored executive briefing to align your 2026 action plan.

For detailed analysis of this topic, please visit the official page:Fructooligosaccharide (FOS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com