PW Consulting: Inorganic Feed Mycotoxins Binders & Modifiers Market to Expand at 5.15% CAGR, Reaching About USD 1.31 Billion by 2032

Health |

2026-07-06 04:26:16

As companies plan budgets, supply chains, and product roadmaps for 2026, the resistant dextrin market presents a juxtaposition of steady growth and intensifying strategic complexity. Our latest PW Consulting research frames that complexity through a practical, execution-focused lens: the market has demonstrated resilience through 2020–2025 and is on a trajectory that warrants immediate strategic responses in 2026. This preview summarizes the high‑level dynamics and the kinds of decisions the full report is designed to support—while preserving the granular intelligence that subscribers rely on to win in market execution.

Resistant Dextrin Market

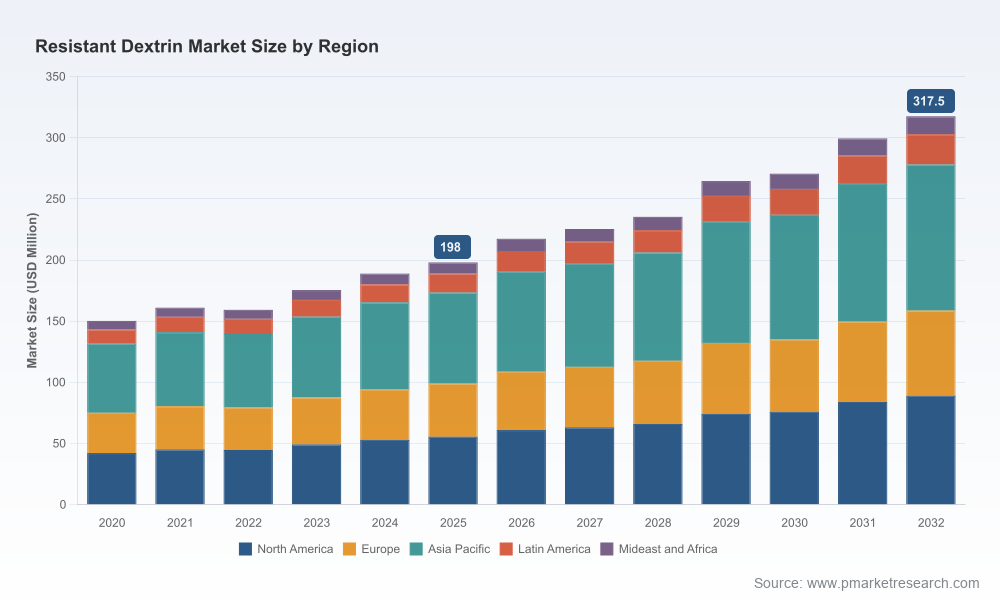

Between 2020 and 2025 the global resistant dextrin market expanded from a modest base to a substantive addressable market. By the report’s base year (2025) the market reached roughly USD 198.0 Million. Our forecast projects continued, compound expansion at a 6.98% CAGR through the 2026–2032 horizon, with the market rising to approximately USD 217.4 Million in 2026 and toward roughly USD 317.5 Million by 2032. That growth path reflects both sustained demand in core food, beverage and nutraceutical channels and an expanding set of applications enabled by new regulatory recognitions and clinical substantiation.

Resistant Dextrin Market

Cost and input volatility — Input cost volatility has become a strategic operating constraint. Raw material supply economics tightened in 2025, with corn‑starch feedstock pricing reaching record levels mid‑year. These cost moves impact producers and formulators differently depending on procurement scale, hedging sophistication, and the availability of alternative starch sources.

Resistant Dextrin Market

Regulatory and clinical signaling — 2025–2026 activity has raised the bar for functional claims and market access. Several leading soluble fiber products have secured recognized dietary fiber status and third‑party prebiotic verification, materially expanding permissible claims in formulations (notably in reduced‑calorie beverage and food categories). This kind of certification reshapes commercial conversations and accelerates product development cycles for brands that can capitalize on validated health claims.

Consolidation vs. fragmentation — The industry sits in a middle state of concentration. A handful of established ingredient houses control a meaningful share of supply, yet there remains room for regional producers and private‑label suppliers to gain footholds through cost leadership and niche product formats. Market concentration metrics indicate that the top 3–5 firms account for a dominant portion of global volumes, creating both barriers to new entrants and targeted opportunities for strategic partnerships.

Application evolution — Demand is broadening beyond staple food ingredient roles to higher‑margin nutraceutical and functional beverage avenues, driven by consumer interest in gut health and sugar reduction. This shift favors suppliers that can offer clinically backed, label‑friendly solutions and flexible product formats (powders, liquids, agglomerates) tailored to formulators’ needs.

The competitive picture is shaped by a mixture of global ingredient conglomerates, regional specialty producers, and bulk suppliers. Key incumbents combine brand strength with scale and regulatory footprints—factors that translate into preferred supplier status for many major food and beverage manufacturers. Notable strategic positions include:

Tate & Lyle (UK): Global distribution reach and an established portfolio of soluble fiber platforms. Their play is classic ingredient house: leverage global customer relationships and co‑innovation to sustain premium positioning.

Matsutani Chemical Industry (Japan): A technical leader with multiple product formats and strong formulations competency—advantages in Japan and export markets where product consistency and format variety are decisive.

Roquette (France): Demonstrating a clear move from commodity supply to clinical differentiation—recent capacity expansion and third‑party prebiotic verification have sharpened their commercial value proposition for health‑positioned applications.

Shandong Bailong Chuangyuan and Niran Bio (China): Volume and cost competitiveness, with an emphasis on bulk supply to food and beverage processors; relevant for price‑sensitive channels and regional distribution networks.

US players (Cargill, Ingredion, Grain Processing, Anderson Advanced Ingredients): Integrated manufacturing and deep customer relationships across bakery, confectionery and beverage sectors—these firms compete on formulation support, supply reliability and integrated sales channels.

Capacity and capability: Roquette’s 2025 expansion increased specialty fiber output in Europe, easing local supply constraints for food manufacturers seeking shorter supply chains and faster time to market for new SKUs.

Clinical/claim differentiation: Roquette’s NutraStrong™ prebiotic verification (2026) and expanded regulatory recognition have reopened commercial windows in reduced‑calorie and health‑positioned beverages—areas of rapid NPD activity.

Price pressure from feedstock: Mid‑2025 corn‑starch price spikes have elevated the importance of procurement strategy, cost pass‑through analysis, and alternative raw‑material sourcing in supply agreements.

Supplier strategy — For formulators and brands, the priority is to reconfigure supplier portfolios to balance cost, claim potential and supply security. This includes negotiating volume‑flex contracts, qualifying multiple formats from different geographies, and securing clinical/labeling support for co‑developed claims.

Product positioning — Brands should target applications where validated fiber claims can command price premiums or unlock incremental distribution channels (e.g., reduced‑calorie drinks, digestive health supplements). Fast followers risk commoditization; first movers with validated claims gain outsized shelf and marketing advantages.

Cost and pricing playbook — Ingredient inflation requires dynamic pricing frameworks tied to feedstock indices, multi‑year hedging where appropriate, and scenario modeling that incorporates margin sensitivity and consumer price elasticity across channels.

M&A and partnership screening — Buyers should prioritize targets with complementary capabilities: regional production footprints, proprietary processing formats, or clinical dossiers that materially de‑risk claims. The market’s concentration means strategic acquisitions can accelerate share gains, but disciplined valuation is critical given input cost cyclicality.

Our complete market study is built for strategic execution teams and includes:

Integrated market model: a validated bottom‑up demand model spanning 2020–2032 with scenario variants. (Note: detailed regional and application splits are included in the full report and intentionally omitted from this preview.)

Commercial playbooks: go‑to‑market templates for brands, formulators and ingredient suppliers, including sample contract language for price indexation and supply security clauses.

Regulatory and claims matrix: jurisdictional guidelines, claim pathways and third‑party verification options—directly linked to product innovation roadmaps.

Competitive benchmarking: capacity maps, capability heatmaps and a CR‑based concentration analysis that identifies where incumbent advantage is structural versus contestable.

M&A scoring tool: proprietary due‑diligence checklist and valuation sensitivity templates calibrated for resistant dextrin economics.

Procurement: Re‑baseline supplier risk assessments with mid‑2025 feedstock shocks and contract repricing scenarios; consider strategic reserves and dual‑sourcing for critical SKUs.

R&D: Prioritize prototypes that leverage verifiable fiber claims and optimize for manufacturing formats your supply base can reliably deliver—reduce late‑stage reformulation risk.

Corporate development: Use our M&A scoring to identify targets that close capability gaps (clinical dossiers, formats, regional scale) rather than simply adding volume.

Sales & Marketing: Align trade strategies with validated claims and channel economics; invest selectively in brand campaigns where differentiated health claims can drive SKU rationalization and higher sell‑through.

Our analysis combines granular commercial modeling with on‑the‑ground supplier and customer interviews. We translate macro forecasts into line‑level decisions—contracts, product specs, and M&A screening tools—that procurement, R&D and BD leaders can use immediately in 2026 planning. The full report contains the segmented data, supplier scorecards, and downloadable models that are intentionally absent from this preview to preserve the actionable value for subscribers.

If your 2026 planning requires defensible supply strategies, a prioritized innovation roadmap, or target screening for acquisition or partnership, the full PW Consulting Resistant Dextrin Market report provides the operational intelligence you need. Access the complete dataset, supplier scorecards, and executable playbooks through our research portal—designed for executive teams that must convert market signals into decisive action.

For detailed analysis of this topic, please visit the official page:Resistant Dextrin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com