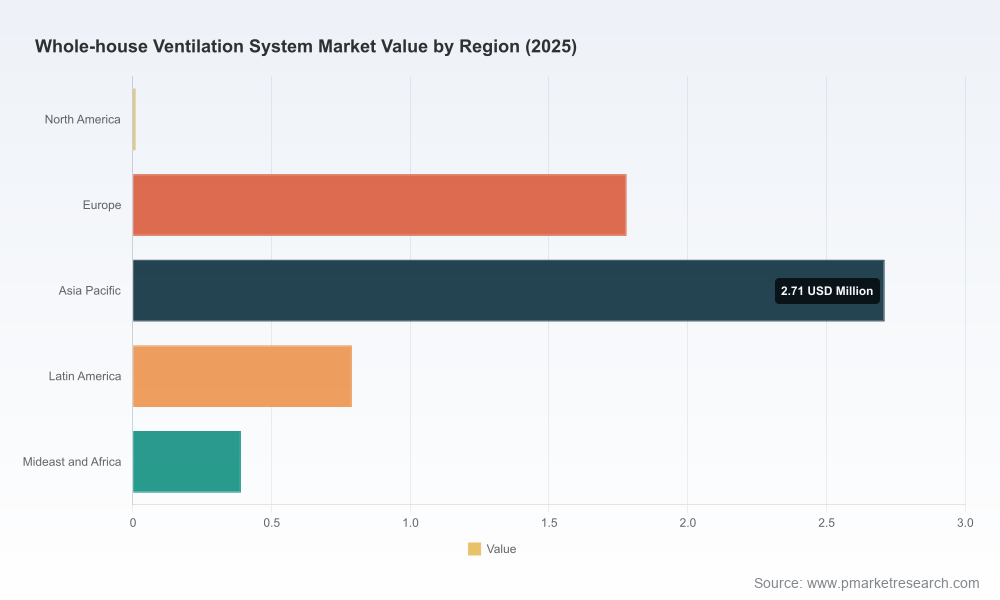

Whole‑house Ventilation System Market — Strategic Briefing for 2026 Decision‑Makers

As building codes tighten and indoor air quality (IAQ) rises on the strategic agenda of builders, developers, and end‑users, whole‑house ventilation systems have moved from niche energy‑saving measures to core components of residential and multifamily mechanical design. This PW Consulting briefing synthesizes the strategic implications of that transition for C‑suite and product leaders preparing plans in 2026. Our independent market model (base year 2025; historical series 2020–2025; forecast window 2026–2032) shows a sustained expansion at a compound annual growth rate of 6.52%, taking the market from its 2025 base toward materially larger volumes by the end of the forecast period. What follows is a concise, actionable orientation that demonstrates the report’s analytical depth while preserving the granular intelligence reserved for report subscribers.

Whole-house Ventilation System Market

Market trajectory in plain terms — why 2026 is a pivotal planning horizon

Three forces converge to make 2026 a decision point for market entrants and incumbents alike: regulatory tightening, rising buyer expectations for verifiable performance, and the economics of whole‑building energy strategies.

Whole-house Ventilation System Market

- Regulation is explicit and accelerating. Recent code updates and acceptance tests — including mandated limits on exhaust‑only approaches in certain jurisdictions and new acceptance test protocols that verify HRV/ERV airflow, sensible recovery, and fan power — change the procurement calculus for builders and specifiers. National and regional standards such as ASHRAE 62.2 remain the technical baseline, while state and local adoptions are creating differentiated demand pockets.

- Buyers now require demonstrable outcomes. Owners and multifamily operators are increasingly specifying systems with certified performance and fault indications. Acceptance testing and visible diagnostics are shifting purchasing decisions toward systems that can demonstrate measurable recovery and low parasitic fan loads under real conditions.

- System economics favor integrated solutions. Rising attention to decarbonization, all‑electric building strategies, and comfort/IAQ liabilities in warranty periods has pushed contractors and developers to consider whole‑house ventilation as part of the HVAC and building envelope value chain rather than as an add‑on.

For a leader mapping 2026 strategy, these trends mean that product attributes (measured recovery efficiency, low fan power, ease of commissioning and serviceability) and go‑to‑market capabilities (specifier relationships, installer training, and integration partnerships) will determine winners and losers — perhaps more than narrow component cost advantages.

Whole-house Ventilation System Market

Competitive structure and implications for strategic choices

The whole‑house ventilation market remains fragmented. Our concentration metrics confirm limited dominance by a small set of players, with market concentration measures indicating that no single vendor group controls a commanding share. In practice, this fragmentation translates into both risk and opportunity: established HVAC and home‑comfort brands can leverage distribution scale, while nimble specialist vendors can build technical differentiation and identify regional niches.

- Scale advantages are real but not decisive. Large HVAC manufacturers bring channel access, warranty infrastructure, and name recognition that speed specification in new construction. However, they must prove their performance claims in measurable terms to win retrofit and high‑performance builds.

- Niche technical leadership opens routes to premium positions. Vendors that excel in cold‑climate heat recovery, robust enthalpy exchangers, or low‑maintenance designs can carve defensible positions in regions and product segments where those attributes matter most.

- Certification and testing are the new hygiene factors. HVI and jurisdictional acceptance tests are becoming purchase pre‑conditions. Vendors that pre‑qualify models and package commissioning and fault‑indication support will shorten sales cycles and reduce installation contingency costs for contractors.

What this means operationally for manufacturers and suppliers

We distill five practical strategic priorities for 2026 action plans:

- Product roadmaps tied to measurable performance: Prioritize reductions in fan power per delivered airflow, improved sensible recovery across operating conditions, and fault‑indicator / commissioning interfaces. These features directly address code acceptance testing and buyer risk aversion.

- Modularity and retrofit readiness: Design form factors, mounting options, and control interfaces that simplify cross‑platform retrofits. The ability to position a product for both new construction (where codes drive adoption) and retrofit (where installer economics drive adoption) expands addressable opportunity.

- Channel and specification plays: Invest in builder and HVAC contractor training, develop spec packages for high‑volume builders, and create bundled solutions with HVAC OEMs and controls suppliers. Short‑term pilots with multifamily developers can rapidly demonstrate total cost of ownership upside.

- Certification, testing, and field validation services: Build lab certifications and add field acceptance support to reduce perceived buyer risk. Providing documented compliance with evolving acceptance tests accelerates approval in code‑sensitive markets.

- M&A and partnership discipline: Use targeted acquisitions to add regional distribution, specialized engineering (e.g., enthalpy exchangers or cold‑climate optimization), or digital commissioning services rather than pursuing undifferentiated scale.

Channel and commercial playbook — practical steps for 2026 go‑to‑market

Winning in 2026 requires more than a compelling product. It requires a commercial model aligned to specifier workflows and installer economics:

- Segment your route‑to‑value: prioritize new construction in jurisdictions with code adoption momentum, while layering retrofit pilots in high‑visibility projects (passive house, net‑zero projects) that create reference installations.

- Enable the installer: provide commissioning kits, simple diagnostic UIs, and service manuals that reduce first‑time install time. Offer training programs that retake specification control away from commodity channels.

- Integrate digitally: build or partner for simple sizing tools, online commissioning logs, and warranty registration that make performance verifiable across the product lifecycle.

- Price for outcomes: consider bundled contracts with performance guarantees tied to airflow and power metrics for large multifamily customers who value predictable operating costs.

Competitive landscape — where incumbents sit and the likely vectors of competition

Our competitive mapping profiles the primary vendors shaping product and commercial expectations. Each presents a distinct position from which to compete or partner:

- Carrier (Charlotte, North Carolina) — leverages HVAC leadership to position energy‑efficient HRV/ERV systems as part of broader indoor air quality portfolios. Strength: channel scale and integrated product positioning.

- Zehnder America (South Bend, Indiana) — known for ComfoAir ERV/HRV lines with a focus on whole‑house freshness and efficiency. Strength: high‑end product engineering and brand recognition in performance segments.

- Panasonic (Osaka, Japan) — markets WhisperComfort ERV and related systems emphasizing quiet operation and broad residential fit‑and‑finish. Strength: brand trust and appliance channel reach.

- Broan‑NuTone (Hartford, Wisconsin) — integrates ventilation into the home‑appliance ecosystem with product variants suited to whole‑house exchange. Strength: retail and contractor distribution.

- RenewAire (Madison, Wisconsin) — balances ERV engineering for residential IAQ with a track record in balanced ventilation systems. Strength: technical specialization.

- Lifebreath (Ontario, Canada) — designs for cold climates with HRV/ERV systems optimized for low‑temperature performance. Strength: climate‑specific engineering.

- EXINDA (China, with US/Canada operations) — competes on HVI‑certified ERVs that meet North American standards, offering potentially lower cost entry points. Strength: price/standard compliance play.

- Trane (Davidson, North Carolina) — integrates whole‑house ventilation with broader HVAC systems and controls. Strength: enterprise HVAC relationships and service infrastructure.

- STIEBEL ELTRON (Germany) — markets central ventilation systems with enthalpy exchangers suited to whole‑building thermal recovery. Strength: premium heat recovery engineering.

- Aereco (Ireland) — offers hybrid, room‑by‑room demand control systems that optimize ventilation based on occupancy and pollutant loads. Strength: demand‑control innovation and specification appeal.

Competition will play out along three axes: measurable performance, installer economics, and channel control. Incumbents with distribution and brand can defend by bundling services; specialists can win by offering demonstrably superior recovery or climate‑specific advantages.

What PW Consulting’s full report delivers — operational, transactionable insight

Our subscriber report is built for executives who must make procurement, product, and M&A choices in 2026. Highlights include:

- Robust market sizing and scenario forecasts (2020–2032) with clear assumptions, sensitivity testing, and a base‑case CAGR of 6.52% that informs capacity and go‑to‑market timing.

- A regulation and standards matrix mapping jurisdictional adoption timing, acceptance test requirements, and compliance pathways for architects, MEP engineers, and building owners.

- Technology and product taxonomy that quantifies the value of recovery efficiency, enthalpy performance, fan power, and diagnostic functionality for different buyer segments.

- Actionable go‑to‑market playbooks for manufacturers, distributors, and service providers, including product bundles, installer enablement programs, and specification kits for builders.

- Competitive profiles with vendor positioning, capability gaps, and M&A candidate shortlists for buyers targeting consolidation or capability acquisition.

- Practical commercial tools — sample spec language, acceptance‑test readiness checklists, installer cost models, and a retrofit decision calculator that translate strategy into deployable tactics.

Note: the full report contains the granular segmentation and regional breakdowns that underpin these conclusions. Those subsegment tables and regional analytics are intentionally reserved for report recipients to preserve competitive value; the summary above is intended to demonstrate the report’s scope and immediate utility for 2026 planning.

Risk map and near‑term watchlist for executives

Key risks that should figure into boardroom discussions and 2026 capital allocation include supply chain shocks for core components, accelerated regional code adoptions that stress production ramp capacity, and the reputational costs of failing to support field acceptance testing. Our report provides a prioritized mitigation matrix and procurement timelines that align production planning with code adoption curves.

Final synthesis — why this analysis matters for 2026 decisions

In markets where codes and measurable outcomes increasingly drive procurement, having a clear, operational view of demand drivers, performance expectations, and competitive posture is no longer discretionary. The whole‑house ventilation market’s steady growth trajectory and its low to moderate concentration create openings for well‑timed product investment, targeted partnerships, and selective acquisitions. PW Consulting’s market model and playbooks convert regulatory change and technical trends into executable moves for manufacturers, distributors, and institutional buyers preparing 2026 budgets and three‑year strategic plans.

For executives who require the full set of subsegment tables, regional forecasts, and vendor benchmarking data to finalize capital allocation and product roadmaps, the complete PW Consulting report delivers those decision‑critical artifacts and the tactical templates needed to act immediately.

For detailed analysis of this topic, please visit the official page:Whole-house Ventilation System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com