Optical Fiber Fusion Splicer Market — Strategic Preview for 2026 Decision-Makers

As fiber deployment accelerates across telecom, cloud, and enterprise infrastructures, the optical fiber fusion splicer market is entering a phase where product differentiation, procurement timing, and supply-chain resilience will determine winners and losers. PW Consulting’s upcoming market study (base year 2025, historical window 2020–2025, forecast horizon 2026–2032) synthesizes historical performance with forward-looking scenario analysis to equip executives with the strategic intelligence required for high-stakes decisions in 2026.

Optical Fiber Fusion Splicer Market

Macro trajectory: what the headline numbers tell us

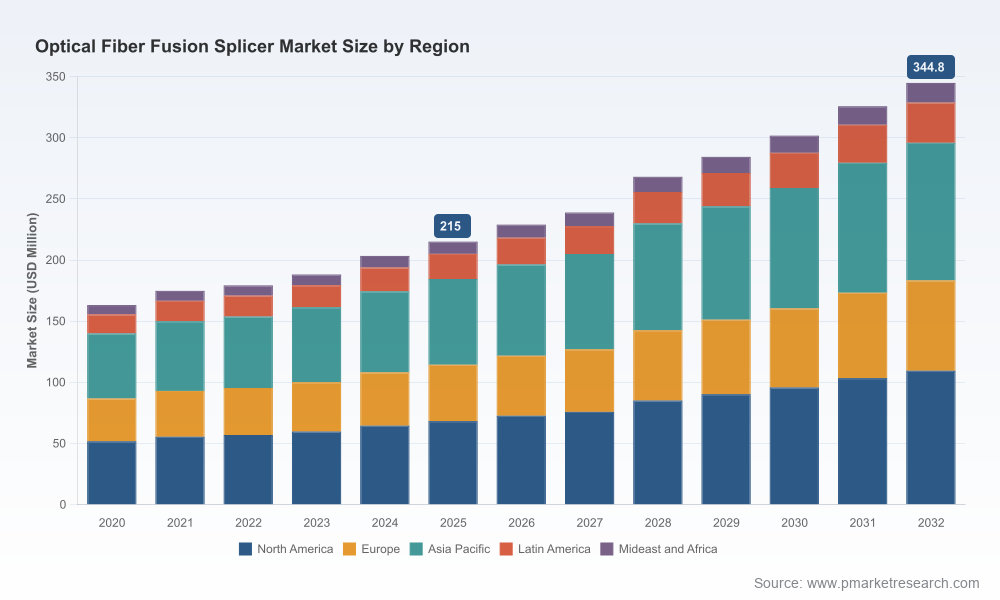

The market’s expansion over the past half-decade demonstrates durable demand dynamics. From an estimated market size just north of USD 160 million in 2020, the market grew to roughly USD 215 million by 2025. Our baseline forecast sees continuation of this trend into the next planning cycle, with the market crossing the mid‑USD 200 millions threshold in 2026 and projecting to approach the mid‑USD 300 millions by the early 2030s. A steady compound annual growth rate of roughly 6.0% underpins this trajectory, reflecting sustained investment in fiber-rich architectures (long-haul, metro, and high-density data center deployments), rising maintenance/repair activity, and incremental replacement driven by automation and performance improvements in splicing technologies.

Optical Fiber Fusion Splicer Market

Why 2026 is a pivotal decision year

- Procurement windows are compressing. Public- and private-sector procurement signals—illustrated by government sources-sought activities in early‑to‑mid 2026—indicate aggregated demand that could move buying cycles forward. Capital planners must weigh near-term purchases against expected product upgrades that reduce life‑cycle costs.

- Product feature bifurcation. Market value is being driven less by unit volume and more by advanced capabilities: automated alignment, mass/ribbon fusion throughput, ruggedized field operation, and cloud-enabled telemetry for asset management. Buyers who lock into a suboptimal technology family risk higher TCO over a 3–5 year horizon.

- Supply-chain and tariff noise. Classification rulings and classification uncertainties around portable splicers are creating near-term customs and sourcing complexity. Companies with diversified sourcing and pre‑approved supplier lists will have a competitive advantage in rapid deployments.

Report utility: what leaders will gain (and why they should request the full study)

PW Consulting’s study is designed for operators, OEMs, infrastructure investors, and procurement leaders who need executable guidance rather than academic descriptions. The report delivers:

Optical Fiber Fusion Splicer Market

- Proprietary demand-forecast model calibrated to 2020–2025 outturns and stress-tested across three macro scenarios for 2026–2032.

- Cost-to-serve maps and installed-base replacement curves that link splicer technology choices to field labour, training, and service-contract economics.

- Competitive benchmarking and product feature matrices that align vendor capabilities with buyer use-cases (from long-haul carrier maintenance to hyperscale data center high-density splicing).

- Procurement playbooks for 2026: timing recommendations, contracting structures, and clauses to mitigate tariff and customs risk.

- Supply-chain risk heatmaps and mitigation frameworks that translate disruption into quantifiable program-level contingency budgets.

To honor the “trailer” principle: this preview highlights the report’s high-value outputs without reproducing the granular segment tables, regional splits, seller market-shares, or price curves that constitute the full commercial intelligence package. Those segment-level datasets and the interactive model are available via the PW Consulting report portal.

Competitive landscape: what to watch among established vendors

The fusion splicer market today combines legacy optical equipment makers with specialized instrument manufacturers. Overall market structure is best characterized as fragmented: several established firms offer differentiated technology stacks and channel footprints, enabling multiple paths to scale without a single dominant integrator. The competitive picture is shaped by the following vendor archetypes and recent moves:

- Precision core-alignment leaders (e.g., Fujikura, Sumitomo, Furukawa): these firms continue to invest in low-loss core alignment algorithms, field reliability, and models that address both telecom and enterprise service needs. Their portfolios span portable single-fiber units to mass-fusion and core-alignment systems used in demanding long-haul and carrier environments.

- Ribbon and high-density specialists (e.g., INNO Instrument): focused on data center and MPO-heavy environments, they compete on speed, simultaneous-fiber handling, and ergonomics for high-throughput environments.

- Channel and systems integrators (e.g., OFS Fitel, AFL): these players leverage OEM partnerships and branded offerings to provide bundled solutions—including splicers, consumables, and field service—that appeal to enterprise buyers and contractors.

Recent activity underscores strategic emphases across the cohort. In May 2026, AFL launched a mass-fusion model that automates fiber placement and reduces operator intervention—an explicit response to demand for higher throughput and lower training costs in large-scale installs. Concurrently, public-sector procurement signals from agencies seeking sources for fusion splicers highlight the growing importance of qualifying to government buying channels. Regulatory developments—such as customs classification rulings—introduce operational friction that favors suppliers with established global trade compliance teams.

Strategic implications and recommended actions for 2026

Executives should convert market momentum into durable advantage through targeted moves in procurement, product development, and partnership strategy. Key imperatives for 2026 include:

- Time purchases around product refresh cycles. Given the pace of incremental innovation—automation, auto-placement, and telematics—buyers with flexible procurement windows can achieve lower TCO by aligning acquisitions to vendor refresh schedules.

- Prioritize throughput and lifecycle economics over unit price. High-density and mass-fusion solutions deliver outsized field productivity gains. Calculate ROI using operator time, mean-time-to-repair, and training amortization rather than comparative unit cost alone.

- Lock in diversified supply agreements. Tariff classification rulings and customs uncertainty mean single-supplier or single-origin strategies carry execution risk. Consider framework agreements with multiple qualified suppliers to preserve deployment speed.

- Invest in field enablement and telemetry. Cloud-enabled splicers and connected maintenance platforms create operational leverage: remote diagnostics reduce truck rolls and support better asset utilization—an area where OEMs are increasingly differentiating their offerings.

- Watch procurement signals and compliance pathways. Government sources-sought and solicitation activity can be an early indicator of surge demand. Align certification and bid readiness to capture near-term public contracts.

Risk vectors that will shape supplier and buyer strategies

Three risk categories merit continuous monitoring in 2026:

- Regulatory and trade noise. Customs classifications and import duties can materially affect landed cost; buyers should model alternative sourcing and duty-management strategies.

- Technology obsolescence and lock-in. Choosing a splicer family without considering firmware upgrade paths, spare parts availability, and interoperability risks creating replacement waves earlier than anticipated.

- Channel and labour constraints. Skilled splicing technicians remain a limiting factor in many markets. Automation that reduces operator dependence will alter competitive dynamics and bidding strategies for large rollouts.

What the full PW Consulting study includes (operational checklist)

The complete report delivers a compact, actionable dossier for 2026 planning cycles, including:

- Excel-native forecast models (2026–2032) with scenario toggles and sensitivity tables.

- Vendor scorecards, product-feature matrices, and recommended procurement language for performance SLAs.

- Service and training cost models tied to regionally-adjusted labour curves (note: full regional breakdowns and application slices are in the paid report annexes).

- M&A and partnership playbook, identifying where tuck‑ins will accelerate go-to-market scale versus organic development.

- Regulatory and customs risk register with mitigation playbooks and contact points for rapid escalation.

Closing perspective

For leaders deciding capital allocation and vendor strategy in 2026, the fusion splicer market presents both risk and opportunity. Market expansion is steady and technology-driven, but rewards will accrue to organizations that tightly couple procurement timing to product roadmaps, diversify supply and compliance strategies, and extract operational efficiency through connected, high-throughput splicing systems. PW Consulting’s full study provides the granular regional, application and vendor-level intelligence required to convert these strategic imperatives into executable plans—without which, well-intended investments run the risk of being outpaced by both technology and policy shifts.

To access the full dataset, interactive forecasting model, and vendor playbooks referenced in this preview, please visit the PW Consulting report page for the Optical Fiber Fusion Splicer Market. The full package contains the segment-level analytics and annexes omitted here to preserve the value of the proprietary research.

For detailed analysis of this topic, please visit the official page:Optical Fiber Fusion Splicer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com