Handheld Marijuana Vaporizers Market Size, Share, Trends, and Forecast by 2033

Other |

2026-06-11 09:26:54

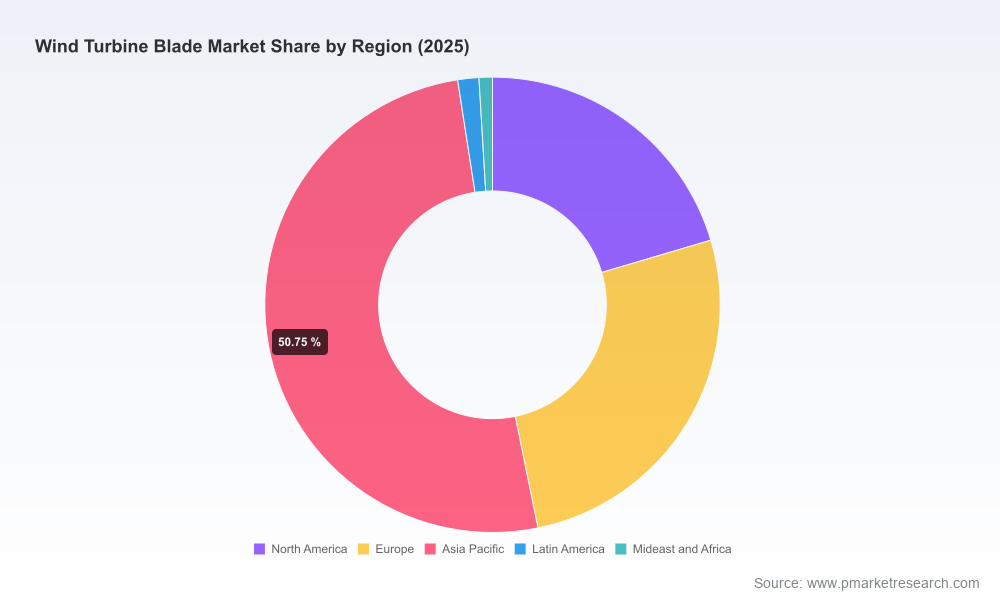

PW Consulting’s latest Wind Turbine Blade Market study arrives at a pivotal moment. After five years of steady expansion, the global blade market expanded from an estimated USD 21.4 billion in 2020 to roughly USD 29.3 billion in 2025 (base year). Our modelling projects continued momentum through the coming decade, reaching an anticipated USD 45.7 billion by 2032 — a compound annual growth rate (CAGR) of 6.53% over the 2026–2032 forecast horizon. For corporate leaders and investors setting 2026 strategies, these headline numbers matter, but the value lies in translating them into portfolio choices, manufacturing footprints, and sustainability-aligned product roadmaps.

Wind Turbine Blade Market

Timing of capital allocation: With a clear mid‑single‑digit CAGR and accelerating demand for larger and more durable blades, 2026 is a year when decisions on factory expansion, tooling investment and partnerships will lock in cost curves for the rest of the decade.

Wind Turbine Blade Market

Regulatory inflection points: Europe’s industry-led landfill ban for decommissioned blades and parallel recyclability commitments are shifting the cost and design calculus for OEMs and suppliers — decisions on materials and end‑of‑life pathways made in 2026 will materially influence compliance risk and resale or secondary-market value.

Wind Turbine Blade Market

Competitive posture: Market concentration remains moderate; the top three firms account for just over a third of industry revenues (CR3 ≈ 35.2%) while the top five approach half (CR5 ≈ 49.8%). These structures create windows for niche challengers, strategic alliances, and roll‑ups, especially in regions where demand outpaces incumbent capacity.

Scale vs. specialization: Growth is driven by both larger turbine platforms (pushing blade length and complexity) and by geographic deployment patterns. Manufacturers who can scale production while accommodating higher-performing composite architectures will capture the best economics.

Materials and manufacturability: Glass and carbon fiber architectures continue to dominate design choices, but the marginal economics of carbon use in longer, higher‑load blades require rebalanced sourcing and new layup processes. Incremental advances in resin systems, infusion methods and mold technologies are reducing cycle times and scrap rates — a 2026 CAPEX plan must reflect these process shifts.

Circularity and regulation: Industry commitments to avoid landfilling blades have moved circularity from corporate social responsibility to an operational imperative. Chemical disassembly pilots and scale‑up pathways (aimed at closing epoxy‑based blade loops) are being tested; firms that invest early in validated recycling alliances will reduce regulatory and disposal cost exposure.

Manufacturing innovation: Additive manufacturing of molds and other tooling is shifting setup timelines and lowering non‑recurring tooling costs. Early adopters can compress ramp times for new blade families and better respond to short‑cycle orders.

Raw material volatility: Fiber and resin price swings continue to be the dominant cost levers. Procurement strategies that combine long‑term offtakes, localized sourcing, and alternative feedstock options will be rewarded.

Logistics and installation limits: Longer blades improve energy yield but amplify transport, storage and installation complexity. Investment choices around near‑turbine assembly, hub port facilities and transport innovation will determine net project economics.

Capacity allocation: A rising share of demand is for larger-format blades and offshore platforms. Executives must decide whether to retrofit existing lines, build dedicated large‑blade facilities, or secure supply through OEM partnerships or acquisitions.

Incumbents and vertical players: Established turbine OEMs and dedicated blade suppliers coexist with clear strategic differences. Some firms supply blades primarily to internal turbine programs while others scale as independent composite manufacturers serving multiple OEMs. Each model presents tradeoffs in margin, capacity utilization and exposure to cyclical turbine orders.

Strategic moves to note: Recent industry activity illustrates the strategic playbook for 2026. One leading blade supplier strengthened its European footprint through a strategic acquisition of a manufacturing site, a composite manufacturer celebrated a major production milestone, and an OEM launched a new offshore platform while industry associations implemented landfill restrictions. These developments signal accelerated consolidation, industrial scale‑up and regulatory enforcement that will rewire supplier relationships.

Opportunities for entrants and challengers: Moderate market concentration leaves room for regional specialists, low‑cost producers and technology disruptors. Winning requires clear differentiation — whether through proprietary composite layouts, superior recyclability credentials, or unmatched local logistics and service models.

Policy tightening: Rapid rollout of end‑of‑life restrictions could increase near‑term disposal costs and require unplanned CAPEX for recycling partnerships or redesigns.

Commodity shock: A sharp move in fiber or resin pricing could compress margins for contractors with short procurement hedges; conversely, favorable raw material trajectories could accelerate market share gains for low‑cost producers.

Technological disruption: Breakthroughs that materially reduce mold lead times or enable scalable, non‑epoxy recyclable blade systems would re‑rank supplier competitiveness and render some legacy assets stranded.

Prioritize modular CAPEX that preserves optionality: Invest in flexible tooling, modular assembly cells, and convertible factory layouts that can shift between blade families without costly rework.

Secure upstream supply through tiered risk contracts: Combine multi‑year offtakes for key fibers with regional spot capacity to balance price and availability risk.

Lock in recyclability pathways now: Partner with chemical disassembly projects and pilot commercial recycling solutions to avoid sudden compliance costs and to create secondary raw‑material value streams.

Reassess M&A and partnership targets: Evaluate strategic acquisitions or minority stakes in regional blade makers, tooling specialists and recycling ventures to accelerate market entry and de‑risk supply.

Embed scenario planning into product roadmaps: Use three‑state scenarios (baseline growth, accelerated offshore adoption, and fast‑regulatory tightening) to stress test R&D priorities and capacity investments.

Actionable forecasts with base year 2025 and a detailed 2026–2032 projection framework, including sensitivity testing across demand drivers and material cost pathways.

Supply‑chain maps and critical node heatmaps highlighting single points of failure, logistics pinch points and substitute supplier matrices.

Competitive scorecards that evaluate capability across manufacturing scale, technology, recyclability, and commercial reach for the leading players.

Investment playbooks for greenfield vs. brownfield capacity choices, including CAPEX/OPEX modelling and break‑even scenarios under alternative demand profiles.

Regulatory risk assessments and compliance roadmaps for material stewardship, end‑of‑life treatment and procurement policies across key jurisdictions.

Deal flow diagnostics and M&A target shortlists based on strategic fit and integration economics.

To preserve actionable value for report subscribers, we have refrained from publishing granular regional and application splits, detailed supplier pricing curves, or full segment tables in this summary. These datasets and the proprietary scoring algorithms that underpin our supplier rankings are included in the full PW Consulting report and are essential for transaction‑level decision‑making.

By 2026, the blade market will increasingly reward organizations that combine manufacturing dexterity, material intelligence and regulatory foresight. The headline growth trajectory — from an approximately USD 29.3 billion market in 2025 toward a forecasted USD 45.7 billion by 2032 at a 6.53% CAGR — underlines the scale of opportunity. But access to that upside will be determined by near‑term operational choices: where you locate capacity, how you contract for fiber and resin, which recyclability pathways you operationalize, and how you position against both incumbent OEMs and agile composites specialists. PW Consulting’s full study equips executives with the datasets, playbooks and deal‑level analysis necessary to convert these macro trends into defensible market position and improved unit economics. For teams preparing budgets, investor decks or M&A pipelines in 2026, this is the strategic intelligence that should inform your next move.

For detailed analysis of this topic, please visit the official page:Wind Turbine Blade Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com