Automotive Stabilizer Bar Market: Strategic Insights for 2026 Decision-Makers

Between 2020 and 2025 the global automotive stabilizer bar market expanded from roughly USD 2,860 million to USD 3,630 million, reflecting steady demand as OEMs balanced ride comfort, vehicle dynamics and mass reduction programs. Our forward-looking model — anchored on 2025 as the base year — forecasts continued expansion through 2032, reaching an estimated USD 5,225 million under the central case and implying a compounded annual growth rate of 5.3% across the 2026–2032 forecast horizon. For executives planning 2026 investments, supplier contracts, or product roadmaps, these topline trajectories are the context for three urgent questions: where to allocate R&D and capex, which suppliers to partner with or acquire, and how to hedge material and regulatory risk while preserving margins.

Automotive Stabilizer Bar Market

Why this research matters in 2026

2026 is a pivot point. The industry has moved beyond one-off lightweighting experiments and into scaled application of new materials, active suspension modules, and tighter integration of stabilizer bar functionality with vehicle electronics and chassis control systems. At the same time, raw-material volatility and advancing regulatory requirements (particularly within Europe) are forcing OEMs and suppliers to make multi-year sourcing commitments. The combination of steady market growth and accelerating structural change means near-term decisions will lock in supplier and technology positions for the remainder of the decade.

Automotive Stabilizer Bar Market

Our study transforms market momentum into executable insight. Rather than a catalog of figures, the research equips decision-makers to: prioritize investment pathways that maximize ROI under multiple regulatory scenarios; position supply chains to absorb material price swings; and identify acquisition targets or strategic alliances that close capability gaps without overpaying for near-term revenue.

Automotive Stabilizer Bar Market

What the report delivers

- Integrated market model (2020–2032): annualized historical sizing and a segmented forecast model that supports scenario switching across material, vehicle architecture, and regulatory assumptions (interactive Excel).

- Actionable go-to-market playbooks: OEM tender-readiness checklists, commercialization timelines for new stabilizer technologies, and channel strategies for aftermarket and fleet segments.

- Competitive benchmarking and supplier scorecards: differentiated profiles covering product breadth, material expertise, geographic footprint, and innovation capability for key players.

- Cost and supply-chain diagnostics: a cost-build of stabilizer bar variants, break-even matrices for in-house versus outsourced production, and tactical sourcing levers for steel and aluminum exposures.

- Regulatory and technology impact maps: Euro 7 and fleet-emissions trajectories, implications for lightweighting, and the commercial roadmap for active/semiactive stabilizer systems.

- M&A and partnership playbook: target-screening criteria and valuation sensitivities for bolt-on acquisitions and joint ventures.

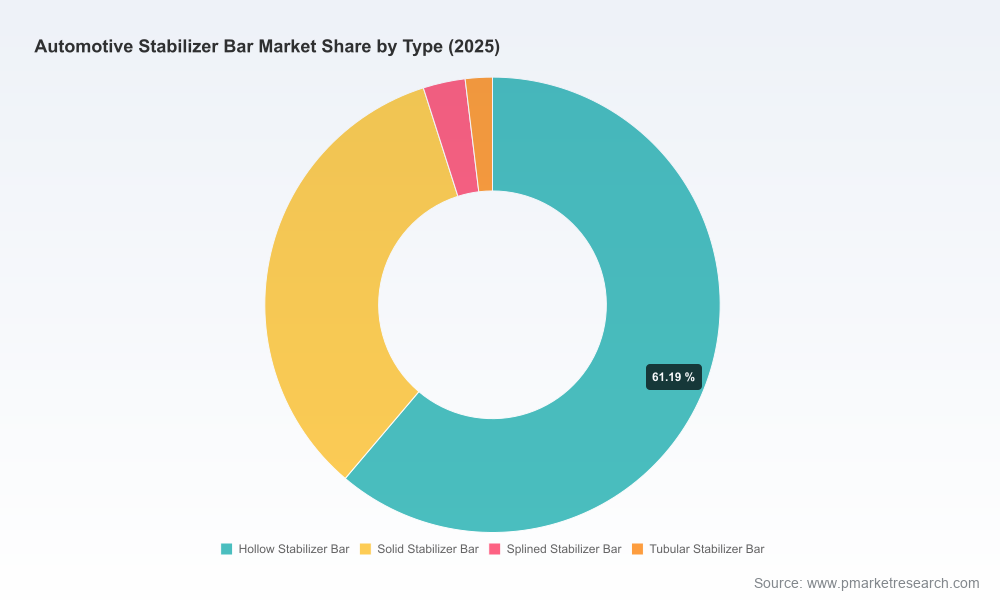

To respect the “trailer” principle of this briefing, core granular splits (by region, application and detailed product type) are intentionally withheld here. The full report contains the complete, model-ready segmentation required for transaction diligence and supply-chain reconfiguration.

Market dynamics shaping supplier economics

Three structural forces are simultaneously reshaping the economics of stabilizer-bar manufacturing:

- Material substitution and cost volatility: Steel remains the backbone of stabilizer systems given its manufacturability and fatigue performance, while high-strength steels and ductile iron continue to address legacy OEM requirements. Meanwhile, aluminum adoption for lightweight platforms is accelerating, but price swings and fabrication complexity increase the cost of change. Strategic purchasers must therefore treat material choice as a portfolio decision — not a one-time engineering choice.

- Functional convergence: Stabilizer bars are evolving from purely passive components into integrated elements of active suspension and vehicle-dynamics systems. Suppliers that can pair mechanical expertise with mechatronic modules or partner credibly with electronic control vendors will have preferential access to OEM platform programs.

- Regulatory and fleet pressures: Emissions and CO2 targets are indirectly driving stabilizer specifications through weight budgets and EV-specific load cases. Regulatory timelines create cliffs and windows for product upgrades; companies that anticipate these windows can capture incremental value with minimal price erosion.

These dynamics are embedded in our scenario modelling and cost curves. They also influence market concentration: the top three suppliers account for a material share of the market, and the top five expand that concentration further — a structural backdrop that creates both consolidation opportunities and differentiation pathways for tier-2 and specialist suppliers.

Competitive landscape: what to watch

The sector combines large integrated suppliers with specialized regional players. Leading firms offer contrasting strategic positions that inform partner or target selection:

- ZF Friedrichshafen AG — integrated systems provider with a clear strategy to pair stabilizer products with active damping and e‑chassis capabilities. Recent joint-venture activity to secure electrified driveline and motor competencies signals an intent to vertically integrate electrified chassis modules.

- Kongsberg Automotive — focused on OEM-integrated solutions for passenger and light commercial vehicles, with strengths in supply continuity and program engineering.

- Sogefi Group — a materials and manufacturing specialist that extends into heavy-duty applications, offering a pragmatic route for OEMs seeking established fatigue performance and scale.

- thyssenkrupp AG — strong in materials innovation; recent launches emphasize high-strength aluminum series aimed at EV platforms, reflecting a classic fast-follower-to-leader technology pivot.

- Mubea Group — precision engineering and program management capabilities make it attractive as a supply partner for high-volume passenger platforms.

- ADDCO, Tinsley Bridge, SwayTec — differentiated niche and aftermarket specialists with performance positioning and rapid go-to-market agility that OEMs and aftermarket channels value for program risk mitigation.

Recent market signals include strategic JV announcements to secure electrified drivetrain components, public procurement solicitations that create non-OEM demand windows, and product launches focused on corrosion resistance and high-strength aluminum. Collectively, these developments compress the runway for suppliers who delay material or functional upgrades.

Strategic moves we recommend for 2026

For executives planning capital deployment or organizational pivots next year, prioritize these moves:

- Invest selectively in lightweight architectures: Fund targeted aluminum and advanced-steel demonstrators that address EV loadcases and NVH requirements. Structure investments as staged pilots to preserve optionality against metal-price volatility.

- Build mechatronics partnerships: Secure partnerships or minority stakes with control-electronics firms to offer OEMs integrated stabilizer-plus-control modules; this materially improves negotiating leverage on platform awards.

- Hedge raw-material exposure: Negotiate indexed contracts, consider financial hedges, and diversify supplier geography for critical inputs to reduce single-point cost shocks.

- Use aftermarket and fleet channels as test beds: Deploy corrosion-resistant and performance-tuned SKUs in controlled fleet programs or aftermarket pilots to validate lifetime claims and accelerate learning curves.

- Pursue bolt-on M&A to fill capability gaps: Target small, profitable firms with niche materials processing or active-stabilizer IP rather than top-line scale acquisitions; this improves margins without excessive integration risk.

Commercial playbooks and KPIs

Execution matters. We recommend a focused set of leading KPIs tied to program economics rather than product features alone:

- Time-to-prototype and time-to-first-sample (measured in stages and gated approvals)

- Cost-per-unit trajectories across material substitution scenarios

- Weight reduction per dollar of engineering investment

- Warranty claim rates and in-service durability outcomes for pilot fleets

- OEM program wins and attachment rates (functional wins per program bid)

These KPIs feed the dashboard used in our board-level briefings and are included in the report’s implementation annex.

Conclusion — positioning for a multi-speed market

The stabilizer bar market is neither purely a commodity nor wholly boutique engineering: it is becoming a hybrid where mechanical excellence, material strategy and electronic integration determine winners. With a measured CAGR of 5.3% in our forecast window, the market offers scale — but value capture will come from the firms that combine material science, system integration and agile go-to-market execution.

To explore the full, transaction-ready intelligence set — including regional and application splits, the interactive forecast model, supplier scorecards and a prioritized target list for acquisition and partnership — access the full Automotive Stabilizer Bar Market report and the downloadable Excel model on our research portal. The model is designed to be used at the board level for 2026 budgeting, for due diligence in M&A, and for supplier negotiation playbooks that lock in future cost and capability advantages.

For detailed analysis of this topic, please visit the official page:Automotive Stabilizer Bar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com