Budesonide Inhaler Market Overview: Key Drivers and Challenges

Other |

2026-03-09 05:29:05

As companies plan capital allocation and product strategies for 2026, the tire changers market presents a clear growth trajectory and a compact competitive topology that reward decisive, data-driven moves. PW Consulting’s latest study — based on a 2025 base year, a historical review from 2020–2025 and a forecast window covering 2026–2032 — quantifies the sector’s expansion and delivers the operational tools executives need to convert market momentum into durable advantage. At the macro level, the global market expands at a compound annual growth rate of 6.8%. Total industry revenue grows from just over USD 1.47 billion in 2025 to roughly USD 2.31 billion by 2032 (USD Million basis). These headline dynamics underpin a story of accelerating product sophistication, aftermarket monetization and differentiated route-to-market economics that we explore below.

Tire Changers Market

Capital intensity vs. return predictability: Equipment manufacturers and large service chains face choices between scaling manufacturing, expanding field service footprints, or monetizing software and consumables. The market CAGR and near-term forecast create a predictable backdrop that supports multi-year CapEx and R&D commitments — but only when paired with the right commercial model.

Tire Changers Market

Product evolution is accelerating: Leverless heads, hybrid center-clamp/swing-arm architectures and higher-torque, faster-cycle table-top units are moving from premium niches into mainstream shop kits. The consequence is compressed product life cycles and the need for modular engineering and manufacturability design choices that speed upgrades without ballooning costs.

Tire Changers Market

Regulatory and trade shocks matter more: New 2025 U.S. import tariffs on automotive equipment — combined with machine- and shop-safety standards under OSHA and fleet maintenance criteria (e.g., CVSA influences) — change total landed cost and compliance obligations. Manufacturers, importers and large fleets must update sourcing and compliance playbooks to avoid margin erosion and operational downtime.

Our research is designed for executives and practitioners who need to act in 2026. The report is intentionally operational and includes:

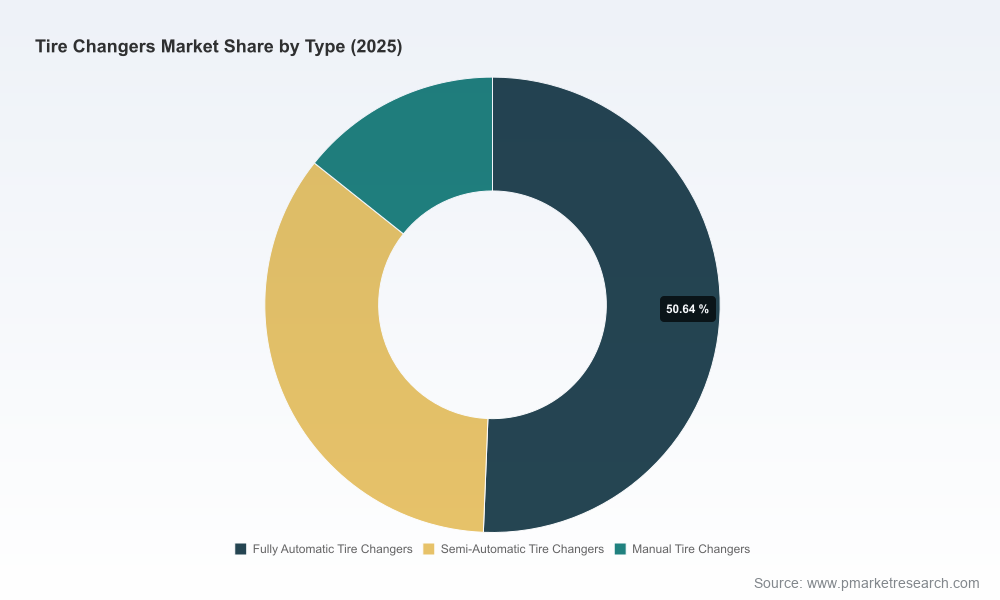

The market exhibits moderate concentration: the top three firms account for roughly the mid-forties percent of industry revenue while the top five push into the low sixties percent range. That profile creates a dual competitive dynamic — established players maintain scale advantages in distribution and brand trust, while mid-market and niche specialists compete on feature differentiation, price-performance and aftermarket relationships.

Hunter Engineering Company — U.S.-based innovator known for table-top, center-clamp and hybrid leverless products (e.g., Maverick® Pro series). Recent launches (late 2025 and earlier in 2025) signal a push into higher-torque, faster-cycle changer designs and integrated inflation systems — a competitive move into premium workshop automation.

Coats Company, LLC — American manufacturing pedigree and a portfolio that spans rim-clamp and swing-arm architectures. Recent product enhancements and a refreshed brand/platform strategy (SEMA 2025) emphasize commercial wheel capability and smart-shop integrations, reinforcing Coats’ differentiation in heavy-use and fleet segments.

BendPak Inc. — Competitive on affordability and practical professional-grade lineups (Ranger and APEX), targeting independents and cost-sensitive service centers with bundled solutions (lifts, balancers) that reduce procurement friction.

European specialists (Hofmann, Cormach, Ravaglioli, Nexion) — Emphasize integration across wheel service (balancers, alignment) and high-performance changers, often leaning on OEM relationships and workshop systems integration as a key selling point in mature markets.

Asia-based OEMs (ACE Machine Tools and others) and U.S. specialist vendors (Derek Weaver, Atlas) — Provide a spectrum of automatic/touchless and ruggedized lower-cost alternatives; important for regional sourcing strategies and price-competitive offerings.

Tariff regime: The 2025 introduction of layered U.S. tariffs on imported automotive equipment changes landed costs, particularly for China-origin supply. Firms must model alternative sourcing, nearshoring and pricing adjustments to maintain margins.

Safety & compliance: OSHA requirements for machine guarding and associated standards for turntables and bead breakers are influencing product design and aftermarket training programs. CVSA out-of-service criteria further push fleet operators toward compliant equipment to minimize downtime risk.

Raw materials & manufacturing posture: Steel-intensive frames remain the dominant bill-of-materials for many OEMs. Decisions to localize welding, stamping and finishing can mitigate tariff exposure but require careful capital planning and labour strategy.

Manufacturers: Prioritize modular platforms and upgradeable electronics so that new features (leverless heads, automated inflation, software diagnostics) can be field-upgraded rather than requiring full replacements. This reduces churn and creates recurring software/service revenue pathways.

Distributors and dealers: Develop bundled service contracts and financing options to lower buyers’ upfront cost barriers, and train sales teams to sell total cost of ownership improvements rather than equipment price alone.

Fleet & large-service operators: Re-evaluate procurement strategies under tariff and compliance scenarios; consider strategic spot-buying combined with long-term service agreements to lock in maintenance uptime and predictable costs.

Private equity & corporate development teams: Use the report’s M&A screening to identify tuck-in targets that accelerate feature roadmaps (e.g., leverless technology firms) or expand service footprints in key geographies where tariffs raise competitive entry barriers.

R&D organizations: Redirect part of incremental R&D spend to automation, diagnostics and digital services — these areas produce higher annuity-like returns and strengthen lock-in effects with end-users.

The full PW Consulting study is organized for immediate operational use: scenario models that let you stress-test investment cases under tariff and demand shocks; a ranked opportunity matrix to prioritize product-market bets; ready-to-use procurement and pricing templates; and a competitive playbook that translates recent product moves into likely tactical responses. Importantly, the report’s appendices contain the granular segmentation by region, product type and application that operational teams need to finalize CapEx and commercial plans — those split-level tables are purposefully withheld from this preview to preserve the follow-through value of the complete dataset.

For leaders deciding budgets, product roadmaps or M&A activity in 2026, treating the tire changers market as a commodity mistake ignores the differentiated returns available through product innovation, service transformation and intelligent sourcing. Our research captures the macro growth path (6.8% CAGR; USD Million basis), the competitive contours (moderate top-end concentration), and the regulatory and supply inflections that will determine winners and laggards. If you need the calculation-ready models, supplier and country-level scenarios, or the prioritized action list mapped to your company type (OEM, distributor, fleet or investor), the complete report and toolkits provide immediate next steps.

Contact PW Consulting to access the full dataset, scenario models and tailored briefings designed to make 2026 decisions both faster and more certain.

For detailed analysis of this topic, please visit the official page:Tire Changers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com