How Is the Medical Cannabis Market Transforming Alternative Healthcare Treatments?

Networking |

2026-05-11 05:32:47

PW Consulting's latest Thionyl Chloride Market briefing is designed as an operationally focused strategic tool for executives, procurement leads, and corporate strategists who must make consequential decisions in 2026. Built on a 2025 base year and a seven-year forecast horizon (2026–2032), the study synthesizes historical performance (2020–2025), a rigorous forecast (CAGR 4.8% through 2032), and targeted scenario analysis to convert complex chemical-market dynamics into actionable options. This introduction outlines the report’s strategic value, highlights the market drivers and supply-side mechanics that will shape the near term, and previews the competitive posture of incumbents — while intentionally preserving the granular segment tables and price schedules for readers who access the full report.

Thionyl Chloride Market

Thionyl Chloride has moved from a specialist reagent into an ingredient of strategic commercial relevance. The market recorded steady expansion through the historical window and reached a measured size in the 2025 base year. Under current assumptions — accounting for demand elasticities across end markets, regulatory adjustments, and feedstock constraints — the market is projected to grow at a compound annual growth rate of 4.8% over 2026–2032, producing material upside for suppliers who can align capacity, purity profiles, and logistics to emerging demand pockets.

Thionyl Chloride Market

Regulatory simplification impacting battery logistics: A key policy change in China — the removal of prior licensing for lithium thionyl chloride (Li‑SOCl2) batteries containing up to 1 kg of the chemical, effective January 1, 2026 — materially alters cross-border trade dynamics for battery makers and their upstream suppliers. The change reduces administrative friction and shortens lead times for a set of primary battery applications, with attendant implications for order cadence and inventory strategies.

Thionyl Chloride Market

Feedstock and synthesis constraints: Industrial production remains materially tied to classical synthesis routes (notably reactions involving SO3 and sulfur dichloride intermediates). Sulfur dichloride, supported in part by refining byproducts, remains the primary feedstock; its availability and the economics of its downstream chlorination steps will continue to determine marginal cost and run-rate decisions for producers.

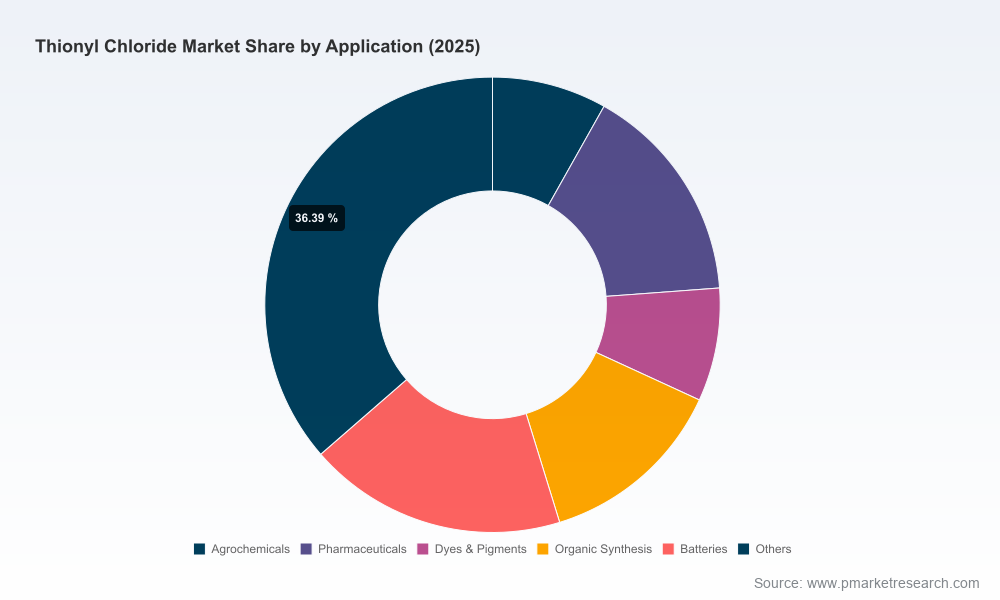

Demand composition is shifting: Growth is being driven by a combination of traditional chemical‑synthesis demand, specialty reagent needs, pharmaceutical-grade procurement, and battery-related applications. The cross-sector nature of demand increases the value of flexible production and grade-differentiation capabilities.

Supply-side resilience in 2026 will be a function of three operational dimensions: feedstock access (sulfur dichloride availability), purification and quality control (to serve pharmaceutical and battery-grade specifications), and logistics/regulatory agility (especially for cross-border battery components). Producers that have invested in multi-feedstock tolerance or backward integration into sulfur chlorination will enjoy margin protection during feedstock squeezes. Conversely, single-route producers are exposed to price and allocation volatility.

From a risk perspective, the interplay between commodity chlorination inputs and specialty-grade processing creates bifurcated operational profiles. Margins and commercial leverage accrue to suppliers who can switch between technical and reagent/pharma grades with limited conversion expense, or who can segment volumes into long-term offtake contracts to stabilize utilization rates.

Batteries: Li‑SOCl2 chemistry continues to be a durable niche for high‑energy primary battery applications. The recent regulatory relaxation in China lowers market friction and can accelerate production cycles for battery OEMs and their upstream suppliers.

Pharmaceuticals and fine chemicals: Growing demand for high‑purity reagents sustains a parallel market for pharmaceutical-grade Thionyl Chloride. Buyers prioritize traceability, certificate-of-analysis conformity, and supplier auditability; these attributes are becoming purchase determinants beyond price alone.

Industrial synthesis and agrochemicals: Traditional industrial uses will remain steady, with periodic cyclical pressure tied to raw-materials and agricultural sector patterns.

The market exhibits moderate concentration: the three largest suppliers account for a meaningful minority of global capacity, while the top five extend that share but leave substantial room for regional specialists and niche providers. That structure creates a competitive terrain where national champions and contract-focused regional suppliers coexist with global specialty players.

LANXESS AG (Cologne, Germany): Strong position in high‑purity chlorinating agents and a recognized supplier to Li‑SOCl2 battery supply chains. Their differentiation is built on high‑purity process capabilities and long-term relationships in specialty battery applications.

Jiangxi Selon Industrial Co. Ltd. (China): A fine‑chemical producer focused on pharmaceutical and agrochemical customers. Their scale in domestic markets and cost competitiveness make them a natural partner for manufacturers looking to localize supply in Asia.

Shandong Kaisheng New Materials Co. Ltd. (China): Positioning as a specialty materials supplier with expertise in organic‑synthesis intermediates. Their value proposition is flexibility and proximity to downstream chemical clusters.

Transpek Industries Ltd. (India): A regional bulk supplier with integrated manufacturing capabilities; appealing to buyers seeking reliable volume supply and customized intermediates.

CABB Group (Germany): Known for chlorinating agents and industrial‑grade products — strong in agrochemical ingredient supply chains and B2B partnerships.

Merck KGaA (Germany) and Sigma‑Aldrich (Merck KGaA; U.S.): Reagent and laboratory‑grade suppliers. Their market strength is trust in quality, certification, and global distribution networks for smaller volume, high‑purity applications.

Bodal Chemicals Ltd. (India): Competes on price and regional distribution for pesticides, pharmaceuticals, and fine chemicals.

Strategically, buyers will find different value propositions: multinational specialty producers offer quality and certification advantages; regional producers offer cost and proximity; reagent suppliers offer traceability and servicing for high‑value R&D customers. For suppliers, options include capacity expansion targeted at battery-grade volumes, M&A to close geographic gaps, or premiumization into pharmaceutical-grade niches.

The full report is structured to translate market analysis into operational steps. Highlights include:

Validated market sizing and 2026–2032 forecast model (base year 2025), with driver-level decomposition and sensitivity runs under alternative regulatory and feedstock scenarios.

Buy‑side playbook: procurement levers, contract design templates, and inventory optimization heuristics for short‑term regulatory shifts (including the China battery rule change).

Supplier benchmarking module: capacity maps, capability matrices (purity grades, emissions profile, hazardous‑goods logistics), and commercial positioning analyses for the leading suppliers.

Regulatory landscape and trade‑flow mapper: treatment of Li‑SOCl2 batteries, licensing regimes, and export‑control stress tests with mitigation frameworks.

Scenario planning and stress cases: two downside scenarios (feedstock shortage; stricter emissions control) and two upside cases (accelerated battery adoption; pharmaceutical demand surge), each with playbooks.

M&A and partnership playbook: valuation heuristics for bolt‑on acquisitions, JV structuring for regional market entry, and diligence checklists tailored to chemical‑safety and environmental liabilities.

Note: To preserve the report’s commercial value for subscribers, detailed regional splits, per‑application dollar allocations, and transaction‑grade price curves are available only in the full product.

Procurement: Reassess contractual mix to favor flexible terms that allow grade switching and volume ramps. Negotiate capacity options with suppliers that can certify pharmaceutical and battery grades to reduce dual‑sourcing friction.

Supply chain: Reconfigure logistics lanes in light of the Chinese licensing change. For firms exposed to high‑volume Li‑SOCl2 battery flows, prioritize suppliers with streamlined export procedures and bonded‑warehouse capabilities to expedite fulfilment.

Operations and R&D: Invest in purification and analytical capacity if targeting pharmaceutical‑grade markets; these investments create sustainable premium margins and market differentiation.

M&A / Partnerships: Target regional producers with strong local customer lists and compliance track records. Small bolt‑on acquisitions can accelerate entry into regulated end markets faster than greenfield expansion.

Risk Management: Hedge exposure to key feedstock inputs via vertical contracts or futures where available. Build contingency plans for rapid feedstock substitution and modular processing to mitigate plant downtime.

For 2026 decision-making, the central implication is clear: opportunity will accrue to companies that combine technical capability (high‑purity processing), regulatory dexterity (logistics and trade compliance), and tactical commercial agility (flexible contracting and offtake structures). The market growth projected at a 4.8% CAGR through 2032 is meaningful but not runaway — it rewards targeted investments and operational differentiation rather than indiscriminate expansion.

If your organization is evaluating capacity investments, supplier consolidation, or strategic entry into Li‑SOCl2 battery supply chains in 2026, PW Consulting’s full Thionyl Chloride Market report provides the granular, transaction‑ready intelligence and tools required to model outcomes and execute. Access the complete dataset, price curves, and segmented demand analytics on the report webpage to move from strategy to implementable action.

For detailed analysis of this topic, please visit the official page:Thionyl Chloride Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com