Weight Scales Market: Insights, Key Players, and Growth Analysis 2025 –2032

Games |

2026-07-07 04:36:22

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused industry primer drawn from our latest Induction Cooktop Market research. This briefing highlights the strategic value of the full report for executive decision-making in 2026: where to prioritize investment, how to structure competition playbooks, and which operational levers reduce risk and accelerate growth. Consider this a trailer — we reveal the broad market trajectory, competitive dynamics, and the types of actionable insights included, while reserving the granular segment-level datasets for the full study.

Induction Cooktop Market

The induction cooktop market is moving from early-adopter substitution toward mainstream household and commercial penetration. On a base-year 2025 foundation, the market’s historical acceleration from 2020 through 2025 has set the stage for steady expansion into the next decade. Our topline model projects continued growth at a compound annual growth rate (CAGR) of 5.6% over the forecast window, translating into a clear increase in aggregate industry revenue by 2032. This trajectory is driven by electrification policy tailwinds, improved product economics, and a wave of product-level innovations that broaden addressable use cases.

Induction Cooktop Market

Historical momentum: The market expanded meaningfully between 2020 and 2025, reflecting accelerating consumer adoption and stronger commercial procurement.

Induction Cooktop Market

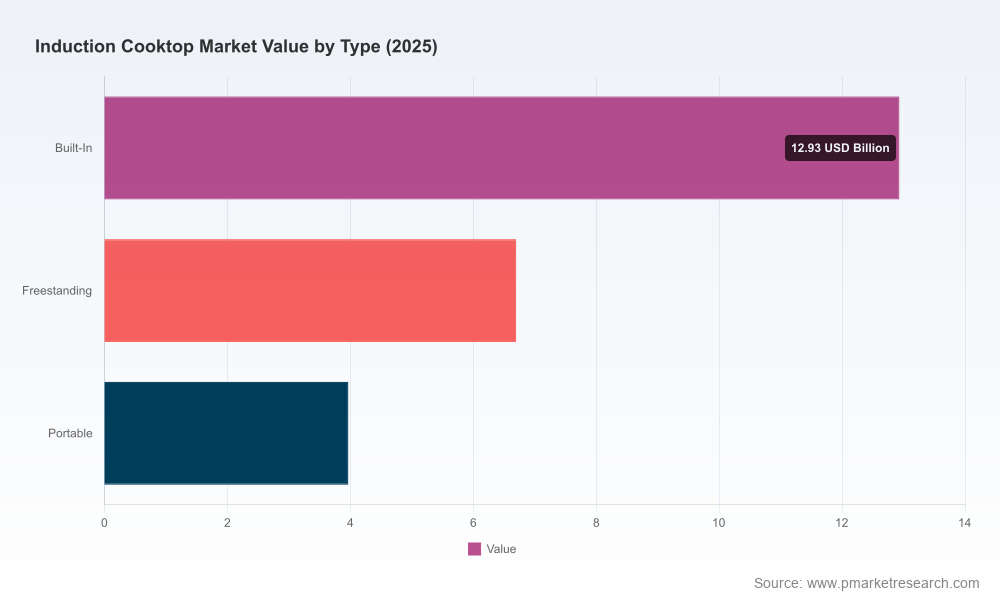

Base-year scale: In 2025 the market reached a substantial USD 23.6 Billion (revenue units in Billion USD), providing a material revenue pool for incumbent and new entrants alike.

Forward view: Our forecast shows the market continuing to expand through 2032 to an estimated USD 34.7 Billion, with 2026 representing the first full-year of the next growth phase and 2029–2031 offering compounding upside as product maturity and policy incentives intensify.

Consolidation signal: Market concentration (CR3 at ~36% and CR5 at ~45%) indicates a marketplace where global brands command real influence but meaningful whitespace exists for focused challengers and regional specialists.

Policy and incentives are moving from signal to deployment. Rebate programs and government procurement guides are lowering consumer acquisition costs and shortening payback horizons for buyers. For 2026 planning, this changes the economics of channel investments and promotional mixes.

Product breadth is expanding beyond traditional residential touchpoints. Innovations that address outdoor cooking, high-output professional kitchens, and portable use cases are increasingly viable. Firms that align R&D and go-to-market (GTM) with these adjacent use cases will capture incremental growth without cannibalizing core lines.

Supply-chain fragilities are now strategic risk. Key upstream components remain concentrated in specific geographies, creating a source of cost and lead-time volatility that must be actively hedged through inventory strategy, dual sourcing, or nearshoring options.

Consolidation and partnership opportunities are time-sensitive. With mid-sized players holding substantial regional strength and leading OEMs focusing on premium features and connectivity, 2026 is an opportune year to evaluate bolt-on acquisitions, licensing deals, or co-development partnerships to accelerate scale.

Our analysis profiles the leading global and niche participants that shape product innovation, distribution reach, and brand equity. The competitive field mixes appliance giants, premium European manufacturers, and specialist commercial suppliers. The following summaries synthesize strategic positioning without disclosing the proprietary segment-level metrics included in the full report.

GE Appliances (Louisville, KY, USA — https://www.geappliances.com): A scale incumbent offering induction lines with integrated connectivity and precision controls. Their strength is wide distribution and cross-category channel leverage. Strategic implication: competitors should anticipate aggressive trade incentives and bundled product promotions in home-package plays.

Samsung Electronics (Suwon, South Korea — https://www.samsung.com): Technology-first approach with Flex Zone and power-boost features. Samsung competes on user experience and ecosystem integration. Strategic implication: winning requires differentiated software/UX or unique hardware advantages.

Miele & Cie (Gütersloh, Germany — https://www.miele.com): Premium positioning focused on durability and long-term reliability. Their moat is brand and quality perception in affluent segments. Strategic implication: mid-tier brands can defend growth by quantifying total cost of ownership and service economics.

Whirlpool Corporation (Benton Harbor, MI, USA — https://www.whirlpoolcorp.com): Multi-brand strategy across price tiers with advanced controls and cleanability features. Strategic implication: scale manufacturing and cross-brand platforming create cost advantages; challengers should consider precision targeting where Whirlpool’s scale is less relevant.

Electrolux Group (Stockholm, Sweden — https://www.electroluxgroup.com): Innovative surface treatments and product aesthetics (e.g., scratch-resistant coatings). Strategic implication: differentiation on durability and long-term finish can justify premium pricing in retail channels.

BSH Hausgeräte (Munich, Germany — https://www.bsh-group.com): Multi-brand engineering across Bosch, Thermador, and Gaggenau with options for high output and full-surface cooking. Strategic implication: strong engineering depth means competitors must match performance or own distinct adjacent use-cases.

The Vollrath Company (Wisconsin, USA — https://www.vollrathfoodservice.com): Focused on commercial-grade solutions for professional foodservice. Strategic implication: commercial channel expertise and service coverage are barriers to entry for general appliance players.

Recent product launches demonstrate how incumbents are stretching category boundaries: Frigidaire’s MatteGuard surface (Mar 2026) targets long-term aesthetic durability; JennAir’s temperature-controlled induction model (Aug 2025) showcases increased cooking precision; and Fire Magic’s built-in outdoor induction (Feb 2025) opens a new product adjacency for built-in outdoor kitchens. These developments underscore parallel paths of value creation: functional differentiation (performance, control), durability (materials and finish), and new use cases (outdoor, portable, commercial).

Regulatory catalysts: The US Department of Energy’s long-term messaging on induction efficiency, buyer’s guides (e.g., Global LEAP Awards 2025), and utility rebate programs (for example, programs offering up to several-hundred-dollar incentives starting in 2026) materially improve consumer purchase economics. These policy levers accelerate market penetration and alter channel economics.

Supply-chain exposure: Ceramic glass and induction coils remain largely sourced from concentrated geographies, creating import dependency that increases lead-time and pricing risk. Manufacturers should model scenarios that include component scarcity and assess the ROI of strategic inventories or alternative suppliers.

Adoption barriers: Perception friction (cooking performance vs. gas), aftermarket service capabilities, and upfront price remain adoption frictions. Successful players will pair product improvements with service guarantees, financing options, and targeted education campaigns tied to energy-savings messaging.

This study is designed for decision-makers who need executable insights, not just descriptive charts. Highlights of the report include:

Robust market model: Annualized revenue series from 2020–2025, base-year 2025 benchmarking, and a detailed forecast for 2026–2032 with sensitivity scenarios mapped to policy, component cost, and adoption-rate levers.

Segment-level playbooks: Actionable GTM and product strategies for each major product type and application. (Note: precise segment-level tables and regional splits are intentionally omitted from this primer and available in the full report.)

Competitive scorecards: Feature-by-feature benchmarking, channel effectiveness analysis, and a grid of likely strategic moves for incumbents and challengers.

Deal and partnership intelligence: M&A screen with prioritized targets, licensing and co-development candidates, and valuation heuristics tailored to the induction sub-economics.

Supply-chain playbook: Risk maps for critical components, cost-to-hedge analytics, and supplier diversification strategies that quantify trade-offs between cost, lead time, and capacity.

Commercial models and ROI calculators: Channel-level margins, promotional elasticity, and break-even models for rebate-driven promotions and subscription/aftercare offers.

Implementation roadmaps: 90–180 day tactical plans for pricing, product launches, service expansion, and regulatory engagement — directly usable by product, sales, and operations teams.

Prioritize rebate-linked GTM pilots. Use available utility and government incentives to reduce consumer acquisition costs and test scalable promotional mechanics tied to energy-efficiency claims.

Hedge supply risk with a targeted dual-sourcing program for critical glass and coil suppliers, while assessing nearshoring pilots for high-demand SKUs where lead times are mission-critical.

Layer product differentiation with service and software. Combine improved physical attributes (durability coatings, high-output modules) with connected features and service offerings to lift lifetime revenue per customer.

For 2026 corporate planning, this market is neither speculative nor saturated — it is a maturing sector with measurable scale and defined pathways to incremental value creation. The full PW Consulting Induction Cooktop Market report turns the headline CAGR and market-size projections into executable programs: where to invest, who to partner with, when to consolidate, and how to protect margins in the face of component concentration and regulatory shifts. If you are evaluating product strategy, M&A opportunities, or supply-chain resilience in 2026, this report will provide the prioritized actions and financial templates to make decisions with confidence.

To access the complete dataset, regional and application segmentation tables, and the operational playbooks referenced here, visit our report page for subscription access and bespoke consulting engagements.

For detailed analysis of this topic, please visit the official page:Induction Cooktop Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com