Dry Eye Syndrome Market Overview: Key Drivers and Challenges

Other |

2026-03-18 07:04:39

As the mining equipment industry enters a pivotal investment cycle in 2026, PW Consulting’s latest market research frames the opportunity and risk landscape with a rigorous, decision-focused lens. The global mining equipment market reached USD 158,470 Million (base year 2025) and, under our central-case assumptions, is expected to grow at a compound annual growth rate (CAGR) of 5.8% through the 2026–2032 forecast window. By the end of that horizon the market size is projected to reach approximately USD 235,600 Million. These headline metrics capture a market that is both large and resilient — but materially reshaped by technology adoption, raw-material cost dynamics, and shifting regulatory regimes.

Mining Equipment Market

Capital allocation and fleet renewal: Companies that front-load selective investments in electrification and automation will capture outsized productivity gains and total-cost-of-ownership (TCO) improvements. The 2026 budgeting round is the last practical window to stage pilots in time for meaningful fleet roll-outs before the second half of the decade.

Mining Equipment Market

Aftermarket and service economics: With equipment lifecycles stretching and reliability expectations increasing, aftermarket parts, predictive-maintenance services, and digital subscriptions are becoming primary profit engines. Executives should be optimizing service networks and telemetry capabilities now to preserve margin in an increasingly commoditized OEM market.

Mining Equipment Market

Supply-chain resilience and input-cost risk: Steel-cycle dynamics, tariffs and the evolving EU carbon-adjustment measures materially alter input-cost trajectories and sourcing incentives. Procurement strategies adopted in 2026 will determine cost-savings and risk exposure through 2028–2029.

M&A and distribution plays: Scale remains a competitive lever. The market shows meaningful concentration at the top (CR3 ~52%; CR5 ~65%), which creates both defensive and opportunistic rationale for bolt-on acquisitions, dealer consolidation, and strategic partnerships.

Robust market-sizing and scenario forecasts: our models capture historical trends (2020–2025) and provide three outlook scenarios (base, upside, downside) for 2026–2032. The executive summary presents implications for capital budgeting and break-even timelines under each scenario.

Decision-grade frameworks: a set of playbooks for electrification pilots, automation roll-outs, and aftermarket monetization — each with checklist-based go/no-go criteria, sample partner-term sheets, and an investment phasing template calibrated to TCO assumptions.

Supply-chain diagnostics and procurement levers: line-item risk assessments for critical inputs, mitigation playbooks (e.g., dual sourcing, strategic inventory, local sourcing economics), and negotiated-contract templates for multi-year steel and components supply.

Vendor benchmarking and competitive positioning: a vendor scorecard that compares technology roadmap, service footprint, OEM-dealer network strength, and aftermarket economics — presented to enable diligence teams to prioritize targets or partners.

Commercial and M&A diligence tools: standardized valuation sensitivities, synergy capture matrices, and an integration-risk heatmap tailored for deals in the mining equipment space.

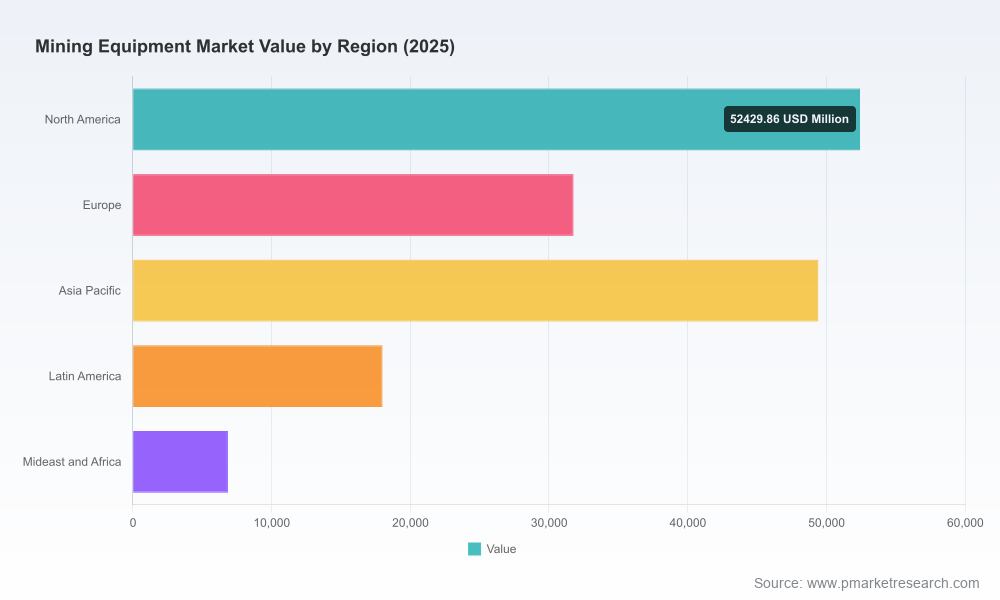

Note: the report contains granular regional, type and application split forecasts and proprietary unit-volume scenarios. To preserve strategic value for subscribers, those detailed segment tables are not reproduced here.

The upper tiers of the industry combine global OEMs with deep service networks and a set of specialist vendors focused on underground, drilling, or mineral-processing niches. Scale confers advantages in R&D spend, financing solutions, and global aftermarket reach — key determinants of winning positions as electrification and automation concentrate value in software and services.

Caterpillar Inc. — continues to lead in heavy surface equipment and is integrating legacy lines into a platform offering that emphasizes autonomous haulage, payload optimization and lifecycle services. Its product cadence and financing options make it a first-order player for large-scale operators seeking integrated solutions.

Komatsu Ltd. — combines product breadth with targeted distribution expansion. Recent dealership acquisitions underline a strategy of closer regional presence and service density in strategic mining corridors.

Hitachi Construction Machinery — is notable for coupling hardware with near-real-time analytics offerings. Digital fleet and remote-insight products are a differentiator for operators prioritizing uptime and remote supervision.

Sandvik and Epiroc — both double down on underground and drilling technologies. Their product innovations are increasingly directed at automation and long-reach drilling, creating cost and safety advantages for deep-mine projects.

Liebherr, Volvo CE, Volvo and other large OEMs — continue to iterate on electrified heavy vehicles. Volvo CE’s 2026 serially produced electric articulated hauler marks an inflection in commercially available zero-emission payload solutions.

Sany and selected Chinese OEMs — gain share through competitive pricing and accelerating electrified-product portfolios, especially for regional and cost-sensitive projects.

Metso and specialist vendors — maintain leadership in mineral processing and exploration tooling. Firms like Boart Longyear and MacLean deliver niche capabilities that matter for early-stage resource development or underground conversion projects.

Serial production of electric articulated haulers signals that electrification is transitioning from prototype to deployable fleet assets. Expect operator RFPs in 2026 that include fossil-free energy and charging infrastructure requirements.

New large-shovel introductions and automated drilling modules indicate incumbent OEMs are pushing performance-based contracts and payload guarantees — shifting risk toward creators of integrated telematics and analytics solutions.

Dealership expansions and selective acquisitions remain the pragmatic route to increasing aftermarket penetration. Targets with dense regional service footprints will command a premium in any M&A process this year.

Input-costs and regulatory measures create immediate tactical imperatives. Steel prices showed limited recovery early in 2026 and tariffs remain a distortion in some major markets. Meanwhile, carbon-border adjustments and tightened safeguards in regions such as the EU change the pass-through math for imported assemblies and spare parts. Global steel demand is expected to modestly rise in 2026 following a contraction in 2025, which implies a gradual normalization of lead times rather than an abrupt cost reset.

Availability of high-quality metallics and labor-market tightness for skilled assembly add another layer of constraint that benefits firms with advanced scrap-blending capabilities, long-term supplier contracts or localized production strategies.

Short-term (0–12 months): run electrification pilots focused on total-site energy and charging integration; secure multi-year purchase agreements for critical inputs; audit aftermarket service coverage and prioritize expansions that yield break-even within 18 months.

Medium-term (12–36 months): roll out scaled fleets where pilot data show >8–12% TCO improvement; integrate telematics platforms across assets for predictive-maintenance contracts; explore bolt-on acquisitions to densify dealer networks in high-utilization regions.

Strategic/longer term (36+ months): transition commercial offers toward outcomes (availability, payload per day), embed software-based monetization, and lock in supply partnerships or partial vertical integration for critical subcomponents.

For leaders making 2026 capital and strategic choices, the rate of technology adoption and the ability to manage input-cost volatility will determine market share shifts through 2032. PW Consulting’s full Mining Equipment Market report provides the granular segment forecasts, vendor scorecards, and operational playbooks required to make those choices with confidence. The executive-level frameworks above are drawn directly from that work — they are intentionally prescriptive while withholding the detailed tables and segment-by-segment figures that form the basis for deployment decisions. To access the complete dataset, playbooks and modelling templates that operationalize these recommendations, please visit PW Consulting’s report portal.

For detailed analysis of this topic, please visit the official page:Mining Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com