Checking Shoulder Seam Tape On Represent Hoodie

Shopping |

2026-07-07 10:36:54

As global semiconductor volumes rebound and advanced packaging and node transitions accelerate, the chemical polishing slurry (CMP slurry) market is entering a decisive growth phase. PW Consulting’s latest market study (base year 2025) quantifies a clear trajectory: the global market expanded from roughly USD 1.58 billion in 2020 to USD 2.048 billion in 2025 and is forecast to reach approximately USD 3.331 billion by 2032, representing a 7.2% compound annual growth rate over the 2026–2032 forecast window (revenues expressed in USD Million). For 2026 strategic planning, this study is built to convert headline growth into executable choices — supplier positioning, capex prioritization, procurement hedging, regulatory compliance and M&A screening.

Chemical Polishing Slurry Market

Mid-single-digit to high-single-digit growth is driven by the combined effects of continued wafer fab investments, proliferation of advanced packaging, and the migration to tighter process windows that increase slurry consumption and demand for higher-performance formulations. The reported forecast quantifies that demand expansion; however, value capture will be uneven across players depending on technical differentiation, customer intimacy, and proximity to leading foundries and OSATs.

Chemical Polishing Slurry Market

From a buyer’s perspective, market expansion creates leverage but also raises supply risk. The study models multiple demand and price-shock scenarios — including raw material spikes and regulatory cost pass-through — to help procurement teams set contract tenors, CLAs, and contingency inventory targets for 2026.

Chemical Polishing Slurry Market

For producers and investors, the growth path signals attractive ROIC potential for capacity additions focused on specialty slurries, but only when investments are aligned with technical roadmaps (e.g., ceria formulations for selective polishing) and customer co-development agreements.

Key demand drivers examined in the report include wafer fab capex cycles, advanced packaging adoption, and the increasing selectivity and defectivity requirements at advanced nodes that favor mono-dispersed and high-purity chemistries.

On the supply side, raw material dynamics are acute. Notably, cerium oxide experienced a significant price shock in early 2025 — a near-term market reality cited in industry sources — which materially altered input cost curves for ceria-based slurries. Our sensitivity workstreams translate comparable raw-material moves into margin and pricing outcomes for vendors and end-users.

Regulatory and safety compliance has moved from “table stakes” to a strategic differentiator. CMP slurries containing hazardous substances must now be accompanied by full GHS-compliant Safety Data Sheets (SDS), and jurisdictions such as China are enforcing national safety management orders that affect storage, transport and workplace practices. The report contains an operational compliance checklist and cost estimates for meeting these evolving requirements.

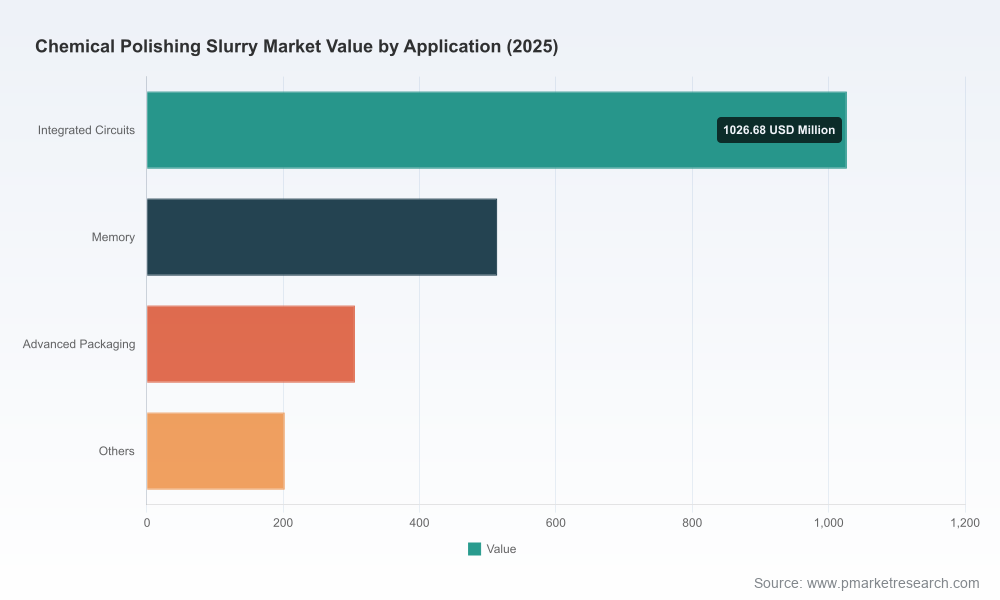

The study segments the market by region, by slurry type (e.g., silica-, alumina-, ceria-based and specialty blends) and by application (integrated circuits, memory, advanced packaging and other polishing use-cases). To preserve strategic value for subscribers and honor the “trailer” approach of this brief, we deliberately omit granular region/application share tables in this introduction. The full report provides a complete, auditable segmentation model, including historical time series (2020–2025) and granular forecasts for 2026–2032, downloadable Excel models, and scenario toggles for custom stakeholder analyses.

The CMP slurry market exhibits moderate concentration. Leading vendors capture a majority of commercial volumes, yet there is room for specialized players that combine technical differentiation with local service. Our competitive analysis synthesizes company profiles, product portfolios, go-to-market models and recent strategic moves to map positioning across the value chain.

Cabot Microelectronics Corporation (Aurora, Illinois, USA) — A global leader in high-purity fumed silica dispersions and custom CMP slurry solutions. Cabot’s scale and longstanding relationships with wafer fabs position it as a go-to supplier for high-volume ILD/oxide polishing programs. See product overview: https://www.cabotcorp.com/solutions/applications/digitalization/chemical-mechanical-planarization

Fujimi Incorporated (Nagoya, Japan) — Producer of the PLANERLITE series targeting ILD/STI, tungsten and barrier applications. Fujimi’s strength lies in process know-how and optimized chemistries for selectivity and low defects. Company product lines: https://www.fujimi.com/product-category/cmp-chemical-mechanical-planarization/

Entegris, Inc. (Billerica, Massachusetts, USA) — Offers dielectric and specialty slurries including ceria formulations for advanced nodes. Entegris has recently invested to expand proximity to foundries, reflecting a broader industry shift towards local capacity. Product catalog: https://www.entegris.com/shop/en/USD/products/chemistries/specialty-chemicals/slurries

Beijing Grish Hitech Co., Ltd. (Beijing, China) — A supplier of colloidal silica-based CMP slurries for semiconductors and LEDs, with a broad product series and growing presence in Asia. Catalog release insights: https://grish.com/product/cmp-slurry/

JSR Corporation (Tokyo, Japan) — Developer of mono-dispersed colloidal silica slurries with a focus on selective layer polishing and low-defectivity formulations. More: https://www.jsrmicro.com/cmp-slurry

Ace Nanochem Co., Ltd. (Youngcheon, South Korea) — Specializes in nanomaterial-based oxide slurries, edge/backside stock slurries, and custom colloidal silica blends. http://www.acenanochem.com/

Jizhi Electronic Technology Co., Ltd. (Wuxi, China) — Regional specialist focused on oxide CMP slurries for STI and metal applications, offering local technical support for delta fabs. https://jeez-semicon.com/

We track market concentration metrics and competitive shares (CR3/CR5) to identify white space for entrants and acquisition targets. For subscription users, our vendor heatmaps, patent portfolios and customer overlap matrices reveal where premium pricing and margin pools will accrue through 2032.

October 2025 — Entegris announced an expansion of CMP slurry production capacity in Taiwan to be closer to leading foundries, a strategic move that reduces logistics lead time and enhances co-development with major customers.

March 2025 — Beijing Grish Hitech released an updated product catalog adding new particle-size grades for semiconductor and LED applications, signaling wider product breadth among regional suppliers.

Early 2025 — Cerium oxide input prices experienced a pronounced uptick, underscoring the vulnerability of ceria-based formulations to upstream raw material volatility. Our report models cost-pass-through timing and margin impact by slurry type.

Throughout 2025–2026 — Regulatory enforcement around hazardous chemical storage and GHS-compliant SDS documentation has tightened in multiple jurisdictions; the report provides a compact compliance playbook and estimated implementation costs for operations teams.

Proprietary market sizing and forecast model (2020–2032) with downloadable Excel outputs and scenario toggles (demand growth, raw material shocks, regulatory cost overlays).

Segment-level insights by product chemistry, application, and region (subscriber access); a buyer’s toolkit for procurement (RFP templates, contract clause language for price variance and quality SLAs).

Supplier benchmarking (technical scorecards, capacity maps, patent & R&D intensity, time-to-requalification estimates) and an M&A heatmap identifying targets that close capability gaps.

Regulatory and HSSE compliance checklist tailored to GHS and notable national frameworks, plus a cost-estimation module for adopting required SDS and storage controls.

Risk register and contingency playbooks (raw material hedges, dual-sourcing pathways, in-region buffer inventory sizing, and accelerated qualification strategies for new suppliers).

Executive summary decks, one-page briefings for board reviews, and an investment memo template for capex and JV proposals.

Short-term (0–12 months): lock in raw-material options and conditional capacity reservations. Run cost-pass-through scenarios to recalibrate pricing frameworks and procurement tenors.

Medium-term (12–36 months): prioritize co-development agreements with foundries and OSATs for next-generation chemistries; localize production where logistics and regulatory complexity create a competitive advantage.

Operational: invest in in-line analytics and quality automation to reduce defectivity and rework costs — a technical advantage that supports premium pricing.

Regulatory & HSSE: implement a standardized SDS lifecycle and storage compliance program to avoid costly shutdowns in jurisdictions with tightened hazardous-chemical rules.

Corporate strategy: use M&A selectively to acquire specialized chemistries or local market access rather than broad-brush capacity additions; our M&A heatmap identifies candidates aligned to these goals.

This introduction is designed as a strategic preview. The full PW Consulting Chemical Polishing Slurry Market report contains the granular segmentation tables, supplier share matrices, downloadable forecast models and executable playbooks that procurement, operations and corporate development teams will use to finalize 2026 plans. For full access to the datasets, scenario models and supplier heatmaps, please visit the report landing page (subscription required) to download the complete study and supporting toolkits.

For detailed analysis of this topic, please visit the official page:Chemical Polishing Slurry Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com