Ice Maker Market — 2026 Strategic Preview

As PW Consulting’s senior industry analyst, I present a focused, strategic preview of our full Ice Maker Market study (base year 2025; forecast 2026–2032). This briefing synthesizes the macro trajectory, regulatory headwinds, supplier dynamics and competitive moves that will shape boardroom decisions in 2026. It is deliberately analytical and directional — we expose the structural signals and strategic implications while withholding the granular, segment-level tables and regional splits that are included in the complete report to encourage direct access to our full dataset and models.

Ice Maker Market

Market trajectory at a glance

The global ice maker market has moved from a mid-single-digit billion-dollar base in 2020 to an expanded market by 2025, and our outlook extends that growth into the early 2030s. Across the 2026–2032 forecast window the market expands at a steady mid-single-digit compound annual growth rate (CAGR of 3.73%), reflecting a mature equipment market punctuated by pockets of innovation and regulatory-driven replacement demand. The implication for executives: planning horizons should balance steady base-demand assumptions with episodic uplift tied to regulatory compliance cycles and feature-driven consumer upgrades.

Ice Maker Market

Why this matters for 2026 decision-making

- Capital allocation: manufacturer CAPEX and retrofit cycles will need to be aligned with both efficiency/regulatory milestones and modest volume growth.

- Product roadmaps: feature investments (e.g., smart controls, low-GWP refrigerant compatibility, self-cleaning) must be prioritized against a moderate growth backdrop.

- Supply chain strategy: raw material inflation and compressor cost volatility make supplier diversification and hedging essential.

- M&A and partnerships: the market structure is fragmented, creating targeted consolidation and alliance opportunities.

- Go‑to‑market optimization: distributors and after-sales service are critical to differentiate in a market where product feature parity is increasing.

Key market dynamics and regulatory inflection points

Three categories dominate near-term dynamics: regulation, input-cost pressure, and product/consumer trends.

Ice Maker Market

- Regulatory timing compresses product lifecycles. In major markets, new energy-performance benchmarks and refrigerant restrictions are no longer theoretical — they are operative drivers of replacement and new-build specifications. Compliance timelines for commercial ice makers and prohibitions on certain refrigerants have created a discrete window in which older models are being phased out and compliant replacements are being specified. For manufacturers, this creates both opportunity (replacement demand) and cost (retooling and certification).

- Raw material and component cost pressure. Rising prices for copper, steel, plastics and key components such as compressors are increasing BOM risk. The net effect: margin compression for manufacturers unwilling or unable to pass through higher costs, and a renewed focus on design-for-cost and local sourcing strategies.

- Product evolution and end‑market demand. From healthcare and institutional kitchens to the premium residential nugget segment, buyers are showing differentiated preferences: reliability and hygiene for commercial users; convenience, style and “ice experience” (nugget, chewiness, fast cycles) for consumers. Smart controls, low-maintenance self-cleaning features, and aesthetic finishes are shifting the competitive battleground beyond raw capacity.

Competitive landscape — patterns and positioning

The competitive set is characterized by established commercial OEMs, legacy appliance brands, and agile consumer-tech entrants. Market concentration metrics confirm a fragmented landscape (CR3 ≈ 24.6%, CR5 ≈ 26.2%) — meaning the top suppliers collectively control a modest share, and there is room for scale-seeking moves.

- Hoshizaki America (Peachtree City, GA) — A classic commercial OEM with deep product breadth (crescent, cubelet, flaked and specialty units) and a reputation grounded in durability and North American production capacity. Their strength: channel relationships with foodservice and hospitality and emphasis on efficiency and long-life hardware. Strategic question: how quickly can they translate standards-driven demand into upgraded product streams without overextending service networks?

- True Manufacturing (O’Fallon, MO) — Known for high energy efficiency and modular cube solutions targeted at professional foodservice. Their smart-control features and emphasis on durability position them well for institutional procurement where lifecycle cost matters most. For 2026, expect targeted plays around service contracts and retrofit kits for regulatory compliance.

- Naixer Refrigeration (Guangzhou, China) — A global-minded commercial supplier offering a range from undercounter to high-capacity cube models, with attention to certifications and practical features like self-cleaning. Their trade-show presence and expanding distribution suggest an acceleration into hospitality markets where value + certification is decisive.

- GE Appliances & Frigidaire (United States) — Legacy appliance brands are contesting the consumer countertop and nugget segments by leaning on strong retail channels, branding, and lifestyle design. Recent product updates and expanded finish offerings underscore an approach that treats ice makers as lifestyle appliances, not just utility items.

- Govee Technology (Shenzhen, China) — Represents a new breed of smart-appliance entrant focused on user experience and IoT integration. Recent launches position them to capture consumers seeking smart, low-maintenance nugget machines — a segment that drives premium ASPs and recurring accessory/service revenue.

Recent activity (product launches, colorways, trade-show exhibits) confirms that incumbents and challengers are both investing to capture pockets of premiumization and compliance-driven replacement. These moves are signals: product differentiation will increasingly be the sum of efficiency, serviceability, and brand-driven consumer experience.

What PW Consulting’s full study delivers (practical contents)

The full report is designed for boards and strategy teams who need executable intelligence rather than descriptive reporting. Highlights include:

- Robust market-size and growth models (historic 2020–2025 and baseline 2026), with scenario variants to stress-test demand against regulatory and material-cost shocks.

- Price-and-cost sensitivity matrices and BOM-impact models for common architectures (commercial modular, undercounter, countertop nugget) to inform margin-protection tactics.

- Regulatory-compliance playbook with timeline maps, certification pathways, and retrofit vs. replace decision frameworks for key jurisdictions.

- Competitive capability heat maps and channel economics for commercial and consumer routes-to-market.

- Supplier risk dashboard: concentrated component exposures (compressors, heat exchangers, controls), supplier relocation scenarios, and inventory policy recommendations.

- Go-to-market and after-sales service templates — from distributor incentive designs to subscription-based ice-as-a-service pilots.

- M&A and partnership screening criteria aligned to strategic pathways: scale play, tech acquisition, or channel extension.

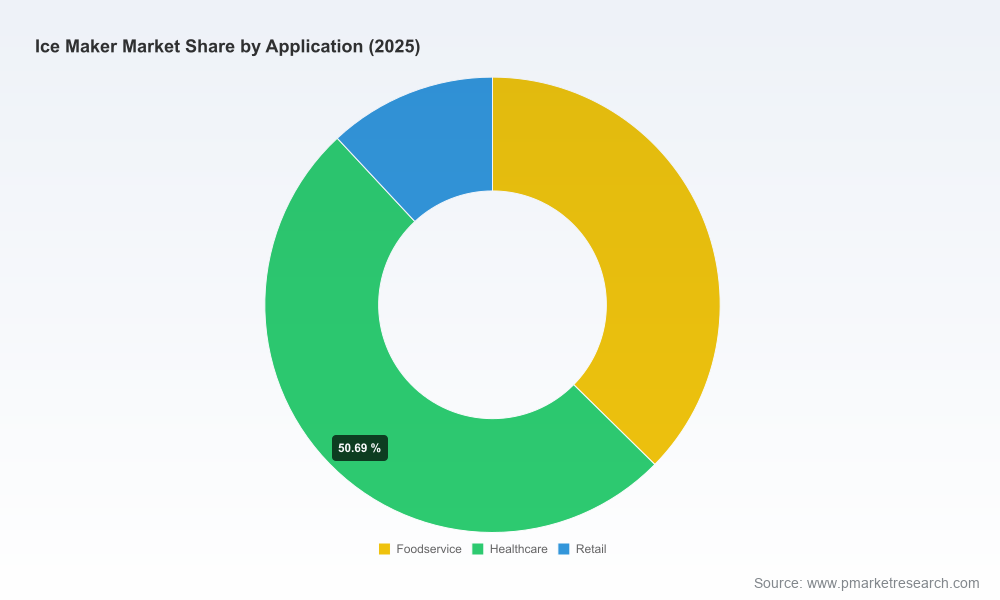

Note: to preserve the value proposition of the full study, granular regional and application-level splits (the tables and datasets that many competitors cite) are deliberately excluded from this preview. Those detailed segment breakouts and the underlying excel models are available in the full deliverable.

Practical 2026 playbook — recommended executive actions

- Prioritize compliance-driven upgrades. Map installed base by model generation and capacity bands against regulatory timelines; prioritize retrofit kits and certified replacements to capture mandated replacement cycles.

- Implement a refrigerant-transition roadmap. Accelerate qualification of low-GWP refrigerant architectures and make supply commitments for compliant compressors and heat-exchanger vendors.

- Design for cost and serviceability. Revisit BOMs to reduce copper/plastic sensitivity and standardize serviceable modules for faster field repairs—this improves uptime and supports premium service contracts.

- Differentiate with software-enabled features. Smart diagnostics, predictive maintenance and consumer app experiences create upsell and recurring revenue opportunities, especially in the nugget/residential segment.

- Selective channel and product portfolio pruning. Rationalize SKUs that compete on price alone; focus investments on segments with clear ASP expansion or where replacement cycles are regulatory-driven.

- Evaluate targeted M&A and distribution partnerships. Given fragmentation, small, accretive acquisitions or exclusive distributor agreements can buy scale and accelerate market access.

Closing perspective

2026 will be a pivotal year for ice maker market participants — not because of explosive volume growth but because regulatory timing, component-cost volatility, and product premiumization converge to create asymmetrical opportunities for those who act deliberately. Manufacturers that align product architecture, supply chain design and go-to-market with the regulatory calendar and evolving customer expectations will convert modest market growth into outsized returns.

For teams preparing capital plans, product-roadmap prioritization, or M&A screens, PW Consulting’s full Ice Maker Market study offers the detailed segment economics, scenario models and supplier-level diagnostics necessary to make informed, defensible decisions. Access the full report and interactive models through our research portal to unlock the segment-level findings and proprietary excel tools referenced in this preview.

For detailed analysis of this topic, please visit the official page:Ice Maker Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com