Encephalitis Treatment Market Size, Share, Technological Trends, and Forecast by 2033

Other |

2026-06-23 10:35:57

As PW Consulting’s senior industry analyst, I present a focused strategic preview of our full Adipic Acid Market study — the essential briefing for executives and strategy teams preparing decisions in 2026. This preview synthesizes the macro trajectory, competitive dynamics, regulatory inflection points and actionable strategic options that will determine competitive advantage across the adipic acid value chain over the 2026–2032 forecast period.

Adipic Acid Market

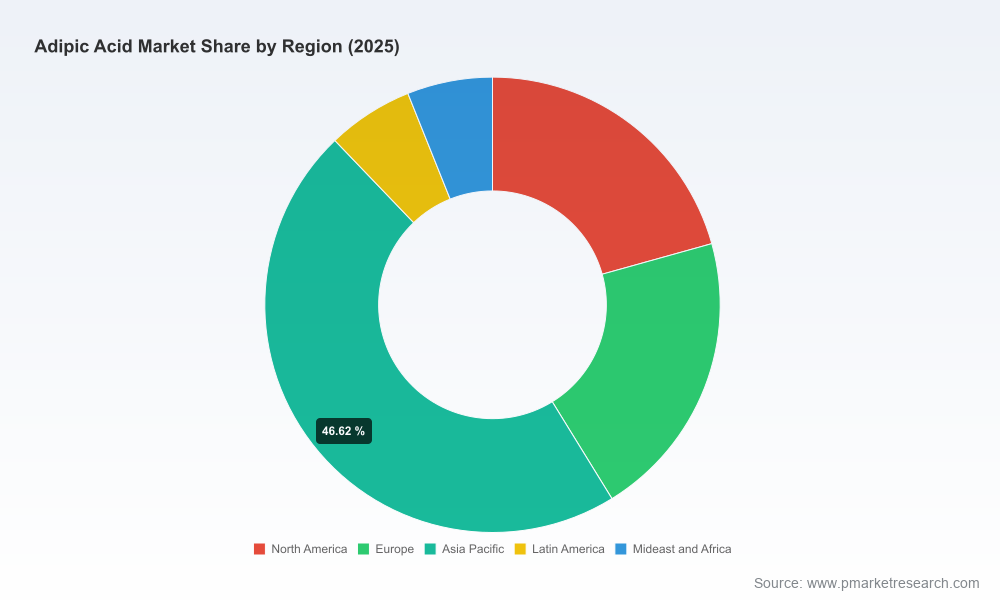

The adipic acid market is on a stable, mid-single-digit growth path. Our base year is 2025 and the model layers five years of historical performance (2020–2025) against a scenario-driven forecast spanning 2026–2032. The market in 2025 stands at approximately USD 5,150 Million (reported in USD Million), and at the headline level our models point to a compound annual growth rate (CAGR) of roughly 4.2% through the 2026–2032 forecast window. That rate reflects a balanced combination of demand expansion in downstream polymers and increasing cost and regulatory pressures that constrain near-term margin expansion.

Adipic Acid Market

Our scenario framework maps three credible paths for 2026–2032: a base case consistent with the 4.2% CAGR, a downside case that reflects sustained raw-material inflation and trade frictions, and an upside case driven by accelerated adoption of high-value, low-emissions product streams and circular feedstock initiatives. Each scenario is parametrized in the full study with supply/demand curves, price sensitivity matrices and regional demand overlays so leadership teams can quantify profit pools by portfolio and geography.

Adipic Acid Market

Adipic acid demand remains closely coupled to the performance of a small set of polymer and additive markets. End-use growth is steady, driven by durable demand in engineering plastics and certain specialty plasticizer applications. However, the pace of value capture is uneven: higher-margin specialty and food-grade niches are growing faster than commodity applications, but they require distinct manufacturing footprints, quality systems and regulatory approvals.

For 2026 decision-makers this implies two tactical priorities: first, protect volume through reliable supply agreements and flexible logistics; second, shift incremental investments toward segments with superior margin expansion and regulatory resilience. Our full analysis quantifies margin spreads across those end-use buckets and models the breakeven investment in quality upgrades and certification pathways.

Raw-material cost volatility and intermittent technical outages are the dominant near-term supply risks. Early 2026 developments illustrate the dynamic: several large producers have publicly adjusted prices to reflect rising input costs, and localized production restarts have produced temporary force majeure events. Those events create short-term dislocations that increase price volatility and create windows of commercial opportunity for sellers with available capacity.

Market concentration remains moderate. The top-three producers account for just over a quarter of global production, with the top-five approaching the low-30s percentage range — a structure that supports price coordination tendencies but also leaves space for agile midsize players to exploit niche positions or geographic arbitrage. The competitive map in the full report shows site-level concentration, lead times, and the destinations most exposed to specific supplier disruptions.

Regulation and trade policy are now central strategic variables. Notably, the Climate Action Reserve’s protocol introduces stringent baseline requirements for N2O abatement for projects under certain frameworks, raising the bar for new capacity and brownfield upgrades. Simultaneously, formal trade scrutiny into imports from specific origins has been initiated by regulators in major markets, creating the possibility of anti-dumping duties or quota-like remedies.

For strategy teams this means that capital allocation decisions must include compliance investment and trade-case contingency. Our report quantifies the incremental capital intensity and operating cost implications of high-efficiency N2O abatement installations, and presents a decision tree for plant upgrades versus import hedging strategies under different regulatory outcomes.

The industry is populated by a mix of integrated petrochemical players, speciality chemical houses and dedicated intermediates producers. Each archetype pursues different priorities:

In the report we provide concise strategic profiles of the principal producers, noting their site footprints, capability differentiation (e.g., food-grade, high-purity, integrated polyamide chain), and recent corporate moves that impact capacity or commercial posture. Recent market events — a broad price increase announced by a major producer in January 2026 and a force majeure declared during a plant restart by another supplier in March 2026 — are analyzed for their likely second-order effects on contract renegotiations, spot market behaviour, and short-term inventory strategies.

Based on our modelling and on-the-ground intelligence, the most attractive near-term value creation paths are:

Two structural shifts make the intelligence in this study especially valuable for 2026-era decisions. First, the interplay between decarbonisation policy and trade enforcement means capital and commercial strategies must be jointly optimised — not considered in isolation. Second, episodic supply disruptions and rising feedstock cost volatility have elevated the value of operational flexibility and niche positioning.

Our analysis converts these forces into quantified trade-offs: we show the incremental margin impact of a supplier price rise, the investment breakeven for an N2O abatement retrofit under regulatory stress scenarios, and the value of moving X% of revenues into premium-grade product lines (detailed outputs available in the full report). These are the kinds of transaction-grade insights that inform board-level capital allocation and procurement strategies in 2026.

This preview is designed to demonstrate the strategic depth and practical orientation of our full Adipic Acid Market study. Senior leaders seeking to convert market intelligence into executable plans in 2026 will find the complete report — with detailed models, supplier scorecards, and step-by-step implementation roadmaps — indispensable.

For bespoke briefings, scenario customisation, or to request the full dataset and model access, contact our advisory team at PW Consulting. We can prepare a condensed executive workshop that maps these findings directly onto your portfolio and delivers a two-year operational plan aligned to your risk appetite.

For detailed analysis of this topic, please visit the official page:Adipic Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com