Topical Skin Adhesive Market: Strategic Outlook for 2026 — PW Consulting Brief

Executive summary

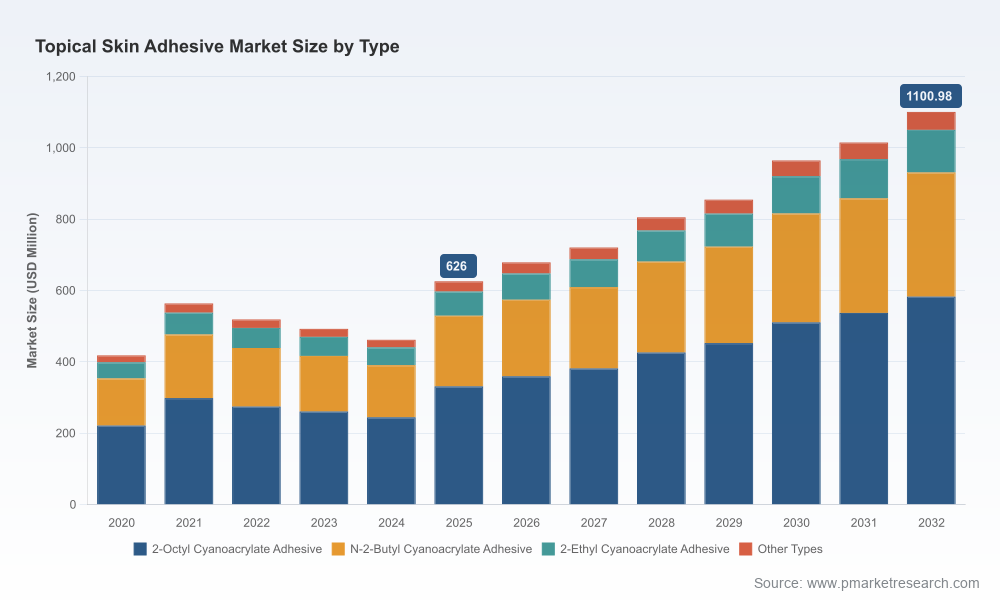

The topical skin adhesive market has emerged from a period of moderate volatility into a renewed growth phase, driven by technological refinements, broadened clinical indications, and a wave of product clearances that are reshaping competitive dynamics. Using 2025 as our base year, the market is estimated at approximately USD 626 million and is forecast to expand at a compound annual growth rate (CAGR) of 8.4% through our 2026–2032 horizon, reaching roughly USD 1.10 billion by 2032. For senior executives and investors preparing strategy in 2026, this market represents a mid-sized, high-margin opportunity with distinct entry barriers — regulatory rigor, clinical evidence, and channel relationships — that favor well-resourced incumbents and focused challengers alike.

Topical Skin Adhesive Market

Why this research matters for 2026 decisions

- Timed investment signals: The rebound observed into 2025 follows multi-year fluctuations. That pattern emphasizes the value of rigorous trend decomposition when allocating R&D and commercial budgets for 2026.

- Regulatory and clearance cadence: Several recent 510(k) clearances demonstrate faster product-cycle pathways for differentiated formulations and delivery systems. Companies that align regulatory timelines with go-to-market readiness can convert approvals into durable share gains.

- Concentration and competitive moat: The market is highly concentrated, which raises the premium on differentiated clinical data, dispenser and procedural ergonomics, and hospital contracting relationships. For acquirers and strategic investors, concentration implies both defensibility and rapid value realization when integrating bolt-on innovations.

- Reimbursement & utilization nuance: Topical adhesives occupy a distinct billing and coding environment; understanding procedural reimbursement dynamics and hospital purchasing levers is essential for commercial tilt and pricing strategy.

Market trajectory: evidence and interpretation

Our time series (2020–2025) shows notable year-to-year variation before settling into a sustained growth trajectory from the 2025 base. This inflection is consistent with a confluence of factors: renewed elective procedural volumes, incremental product innovation (chemistry and delivery), and a stream of regulatory clearances enabling broader indication statements. From a planning perspective, the 8.4% CAGR we project for 2026–2032 is not just a headline number — it reflects modeled adoption curves for next‑generation chemistries, increasing use in emergency and outpatient settings, and gradual expansion of clinicians’ preferences away from sutures for selected low‑tension closures.

Topical Skin Adhesive Market

Importantly, the historical volatility that preceded 2025 underlines two strategic imperatives: preserve optionality in commercial scale-up plans, and invest selectively in evidence generation that shortens adoption cycles when volume rebounds occur.

Topical Skin Adhesive Market

Practical content of the full PW Consulting report

Our full market study is built for decision utility. Key operational elements include:

- High‑granularity market sizing and forward forecasts (2026–2032) by product family and application pathway, presented with scenario sensitivity to adoption rate assumptions.

- Segmentation frameworks (by chemistry, dispenser/delivery, and clinical application) plus adoption curves to prioritize product investments. Note: this brief deliberately omits the detailed subsegment tables; those are available in the full release.

- Deep-dive company dossiers for the leading and emerging suppliers, including commercial footprint, recent clearances, litigation and IP posture, and M&A/partnership activity.

- Regulatory and reimbursement playbooks: stepwise 510(k) strategies, recommended bench and biocompatibility testing matrices, and pragmatic billing guidance for aligning hospital and outpatient pathways.

- Go‑to‑market playbooks and pricing sensitivity models tailored to hospital group purchasing organizations (GPOs), ambulatory surgery centers (ASCs), and emergency care networks.

- Actionable M&A screening tool and a prioritized list of technology gaps for licensing or acquisition to accelerate scaled entry.

Competitive landscape — who matters and why

The competitive field is polarized between global medtech leaders and niche innovators. A handful of firms dominate commercial activity and account for the majority of on‑market sales; however, recent entrants and chemistry innovators are carving differentiated positions through faster polymerization, enhanced viscosity profiles, and novel adhesive chemistries that address clinician ergonomics. Below are the strategic profiles that should guide competitive response planning.

- Ethicon, Inc. — Market leadership is anchored in a strong brand; the incumbent’s portfolio is the reference product in many operating rooms. Their strategic advantage lies in clinical trust, integrated surgical portfolios, and distribution breadth. Mitigation strategies for competitors must include demonstrable clinical outcomes and cost‑of‑use comparisons in OR workflows.

- Advanced Medical Solutions Ltd. — Competes through a combined product and delivery-system approach. Proprietary dispensers that simplify dosing and application can be decisive in adoption. Partnerships with device OEMs or bundled supply contracts with surgical services teams are high‑impact countermeasures.

- Medline Industries, LP — Leverages OR services and supply chain relationships to drive adoption, emphasizing efficiency and total case time reduction. Their playbook illustrates the importance of contracting and hospital-level clinical champions.

- Medtronic plc — Presents a broad wound‑closure portfolio, integrating adhesives into holistic surgical solutions. Their strength is in cross‑selling and leveraging clinical channels outside traditional adhesive buyers (e.g., specialty surgery divisions).

- Chemence Medical, Inc. — Focuses on high‑viscosity chemistries and fast polymerization. Technical differentiation around speed and handling can unlock emergency-department and prehospital use cases.

- Cohera Medical, Inc. — Positions adhesives within a broader tissue‑sealing franchise; success here highlights the commercial value of multi‑indication platforms.

- B. Braun Melsungen AG — Institutional sales strength across hospitals and international markets; advantage lies in procurement relationships and complementary consumables.

- Meril Life Sciences Pvt. Ltd. — Demonstrates a cost‑competitive play for price‑sensitive markets and emerging geographies; localization and regulatory agility are central to their strategy.

- OptMed, Inc. — Emerging challenger with a distinct chemistry (methylidene malonate) and recent FDA clearance for an expanded product. This is a textbook example of how differentiated formulation plus successful regulatory navigation can create rapid commercial traction.

Recent developments that change the playing field

Several 510(k) clearances in the 2024–2025 window have shifted the frontier of product capability and widened clinician choice. These regulatory wins accelerate the commercialization timeline for novel chemistries and delivery systems. Organizations that presciently align clinical trials and hospital pilots to these clearance events will translate approvals into growth more quickly than those that treat clearance as the end‑point rather than a commercial starting gun.

Regulatory, reimbursement and adoption dynamics

- Regulatory baseline: Tissue adhesives for topical skin approximation are regulated as Class II devices under 21 CFR 878.4010(a), requiring 510(k) clearance and conformance with special controls (biocompatibility, sterility, performance testing). Annual device registration and listing remain non‑negotiable operational requirements.

- Evidence bar: The special controls guidance implies a minimum evidence threshold that favors manufacturers with in‑house regulatory and testing capabilities, or those who can partner with contract research organizations to run robust bench and clinical comparators.

- Reimbursement nuance: Adhesives are not typically billed as a direct analogue to skin graft CPTs; hospitals require tailored billing and coding strategies to capture value. Aligning value propositions to OR efficiency and supply‑cost reductions is often more effective than seeking ad‑hoc line‑item reimbursement.

Actionable roadmap for 2026

- Prioritize a phased commercialization plan that ties incremental production scale to validated uptake in pilot accounts rather than full‑scale launches.

- Invest selectively in clinical evidence that maps to measurable hospital KPIs (procedure time, infection rates, re‑closure events) to shorten procurement cycles.

- Evaluate partnerships for dispenser technology or surgical‑service bundling rather than only competing on price.

- For investors: screen targets for regulatory readiness and demonstrated clinician preference signals — these materially shorten the time to revenue post‑acquisition.

Methodology and our confidence lens

Our evaluation synthesizes historical market activity from 2020–2025, primary interviews with hospital procurement and clinical leads, and regulatory and product clearance monitoring. The base year is 2025; forecasts run 2026–2032. Our scenarios explicitly test adoption velocity across outpatient, emergency, and surgical domains, and we present sensitivity analyses in the full report to illustrate downside and upside paths.

Closing — the strategic opportunity

By 2026, the topical skin adhesive market will be both an innovation battleground and a high‑value battleground for procurement influence. The combination of steady CAGR, concentrated market shares, and a stream of new product clearances makes strategic timing critical: early movers who secure clinical champions and demonstrate OR efficiencies will convert approvals into durable market positions. Conversely, late entrants face an uphill climb unless they bring truly differentiated chemistries, delivery systems, or cost structures.

To access the complete dataset, subsegment tables, regional and application breakouts, and our model assumptions and forecast workbooks — including the detailed competitive scorecards and M&A screening tool — visit the full PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Topical Skin Adhesive Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com