Top 36 Sites To Buy, Old Github Accounts In This Year (pdf)

Fitness |

2026-07-03 14:41:31

PW Consulting’s latest industry primer on the Endoscopic Cold Light Source market is designed as an executive-level briefing for 2026 planning cycles. This preview synthesizes the essential market dynamics, competitive postures, regulatory inflection points, and near‑term technology vectors that will determine where returns are made and risks must be managed. It is intentionally diagnostic: we expose the critical levers and strategic implications while reserving full segment-level detail for the complete report.

Endoscopic Cold Light Source Market

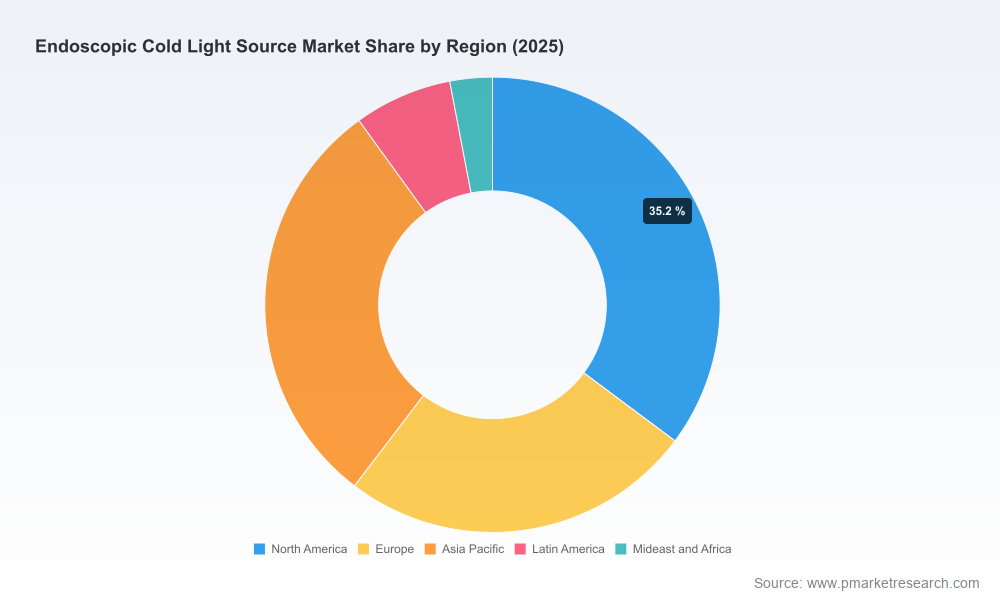

The endoscopic illumination segment sits at the intersection of medical-imaging innovation, minimally invasive surgery growth, and procurement-driven cost discipline. Our model—anchored to a 2025 base year—pegs the endoscopic cold light source market at USD 250.0 Million in 2025 and forecasts steady growth through the coming decade. The market expands to approximately USD 364 Million by 2032 under a compound annual growth rate of 5.5% across the 2026–2032 forecast window. That trajectory reflects both structural demand (shifts toward outpatient, minimally invasive procedures) and technology substitution (LED displacing legacy bulb technologies and influencing total cost of ownership).

Endoscopic Cold Light Source Market

For 2026 strategy, this market is not a backwater: it is a high‑velocity component of broader endoscopy and surgical-imaging value chains. The commercial outcomes firms capture here reverberate across camera systems, processor sales, consumables, service contracts, and clinical workflows.

Endoscopic Cold Light Source Market

Technology substitution and unit economics. LED-based cold light architectures continue to displace older lamp technologies. The shift is driven by lower lifetime operating costs, more consistent fiber-optic illumination, and new capabilities (e.g., fluorescence/NIR support) that are increasingly expected by clinicians. Procurement teams should recalculate lifecycle costs rather than focusing on headline unit price.

Clinical expectations and integrated imaging stacks. Manufacturers that bundle cold light sources with processors and advanced imaging modes (NBI™, BLI, fluorescence/ICG) achieve stickier customer relationships. Regulatory approvals for camera systems are increasingly explicit about light‑source compatibility in 4K or fluorescence setups—creating implicit certification and sales advantages for vertically aligned solutions.

Reimbursement and site-of-care shifts. Expanded outpatient reimbursement programs are moving procedure volumes away from high‑cost inpatient settings, accelerating demand for compact, energy‑efficient, and low‑maintenance cold light sources optimized for ambulatory environments.

Regulatory gating and interoperability requirements. CE and FDA pathways now place greater emphasis on verified compatibility across subsystems—light source, camera, and endoscope—which favors vendors able to demonstrate system-level performance and traceable verification.

Market structure — fragmented but consolidating. The market concentration metrics indicate a sector that is not dominated by a single incumbent; the top three and five players account for less than one-third of market share. That structure creates both partnership opportunities and M&A potential for firms seeking share uplift through scale or complementary portfolios.

Market sizing & rigorous forecasting: historical series (2020–2025), a detailed 2026–2032 forecast, and sensitivity bands (base, upside, downside) aligned to clinical adoption and regulatory scenarios.

Decision-ready playbooks: actionable go‑to‑market frameworks for new entrants and incumbent defense strategies—pricing levers, bundling options, leasing vs. capital sale modeling, and service contract design.

Commercial diligence assets: competitor scorecards, channel and OEM partner maps, procurement negotiation checklists, and a supplier risk heat map for key components.

Regulatory & reimbursement compendium: a curated set of regulatory precedents and reimbursement updates relevant to light-source compatibility and outpatient procedure expansion that impact purchasing decisions in 2026.

Technical and clinical adoption analysis: technology adoption curves, unit economics comparing lamp vs LED lifecycles, and clinical workflow impact assessments for fluorescence-capable illumination.

M&A and partnership screening tools: an investability matrix to prioritize targets by strategic fit, integration complexity, and return horizons, plus a shortlist of diligence questions tailored to LED and illumination IP.

The competitive set is composed of large, diversified players and specialized optics/illumination firms. Each has a distinctive strategic posture that buyers and partners should read carefully:

Karl Storz SE & Co. KG (Tuttlingen, Germany). Their recent product catalog updates emphasise laser‑free POWER LED platforms with extended service life and multi‑modal illumination (white light, NIR/ICG, BLI). These moves signal a focus on high-end, system-compatible light sources that appeal to hospitals and imaging-forward specialists. Expect Karl Storz to continue leveraging clinical partnerships and strong channel relationships to push adoption of its LED platforms.

Olympus Corporation (Tokyo, Japan). Olympus pairs integrated LED light sources with video processors and proprietary imaging modes. Their advantage lies in ecosystem lock‑in: office and procedural customers seeking a verified processor-to-light-source experience will find Olympus appealing. Competitive responses should anticipate bundled offers and trade-in incentives that protect installed bases.

Stryker Corporation (Kalamazoo, USA). Product design that prioritizes intraoperative ergonomics and safety (auto-lighting, scope-sensing safeguards) is Stryker’s differentiator. Their position is strong in OR-focused specialties where real‑time visibility and device safety are prioritized; rivals should match feature parity or emphasize cost/value propositions.

Richard Wolf, ConMed, B. Braun, Medtronic, Smith & Nephew, Fujifilm. These firms compete through specialty focus (e.g., orthopedics, laparoscopy), channel breadth, and integration into broader surgical portfolios. Their strategies range from focused product upgrades to deeper OEM integrations and service-based offerings. For corporates, these players represent logical partners or acquisition targets depending on the desired capability buildup.

Product & tech refreshes (late 2025). Karl Storz’s announcements of POWER LED Rubina and companion platforms underscore the pace of product refresh cycles and the premium placed on multi-modal illumination and long LED service life. Product lifetimes in the tens of thousands of hours materially alter hospital maintenance budgets and service contract structure.

Regulatory clarifications (2025–2026). FDA 510(k) summaries and CE marking practice have increasingly required compatibility verification across camera and light-source pairings, particularly for 4K and fluorescence-enabled systems. Companies that can demonstrate system-level validation will enjoy faster adoption curves in cautious procurement environments.

Reimbursement shifts. Changes in outpatient reimbursement profiles are re‑shaping hospital strategy for capital allocation. Devices that reduce procedure time, setup complexity, and lifecycle costs are more likely to be prioritized for ambulatory surgery centers and office-based settings.

Revisit total cost of ownership models. Procurement teams should require lifecycle analyses that account for LED longevity, fiber-optic transmission stability, and service contracts. Do not evaluate light sources on unit price alone.

Prioritize interoperability and verification. Product managers must ensure compatibility test suites and documentation meet the evolving regulatory expectations for 4K/fluorescence systems—this is a de‑risking exercise for sales cycles in regulated markets.

Match offerings to site-of-care economics. Design compact, lower‑power variants for ambulatory settings and feature-rich, system-integrated options for tertiary centers. Differentiated pricing and service models will be required to capture both segments.

Hunt for strategic pockets, not just scale. Given the market’s moderate concentration, targeted M&A (technology augmentation, channel access, IP) or OEM partnerships can produce disproportionate returns versus broad scale plays.

Embed clinical evidence into commercialization. Leverage demonstration projects that show workflow gains, procedure time reductions, or improved diagnostic yield from fluorescence/NIR-capable illumination—these outcomes accelerate purchasing decisions.

Our full study provides the granular inputs executives need to make capital, product, and partnership decisions in 2026: validated market sizing, competitive benchmarking, regulatory risk matrices, and commercial playbooks. Clients gain access to an empirical view of market growth drivers, the clinical and procurement KPIs that buyers use, and practical templates for pricing and total cost of ownership discussions.

This preview outlines the strategic contours and must‑do actions. The detailed regional, type and application splits, along with transaction‑level scenarios and company valuation comparables, are contained in the full report. For teams preparing budgets, product roadmaps, or M&A theses for 2026, the full dataset and the accompanying advisory session will materially reduce execution risk and shorten time‑to‑market.

Request the full report to access the complete segmentation tables, forecast model, and downloadable decision tools tailored for purchasing, product, and corporate development teams.

Schedule a briefing with PW Consulting to align the market intelligence with your 2026 strategic planning timeline—our workshops convert insights into a prioritized action roadmap.

PW Consulting’s Endoscopic Cold Light Source Market study is positioned to be a practical instrument for executives in 2026—one that turns macro trends into executable strategy while preserving the finer segmentation intelligence for the full report where it belongs.

For detailed analysis of this topic, please visit the official page:Endoscopic Cold Light Source Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com