Fruit & Vegetable Processing Market Growth Accelerates as Food Waste Reduction Becomes a Priority

Food |

2026-06-05 15:38:41

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused preview of our comprehensive Sliding Door Hardware Market study — the actionable intelligence designed to inform capital allocation, product roadmap decisions, sourcing strategies, and M&A prioritization in 2026. The global market, using 2025 as the base year, sits at an inflection point: after consistent recovery through 2020–2025 it is positioned to expand at a compound annual growth rate (CAGR) of 5.2% across the 2026–2032 forecast window. By the end of that period the market reaches a materially larger scale compared with the 2025 baseline, reflecting durable demand drivers in residential retrofits, commercial specification, and growing adoption of space-saving hardware in dense urban construction.

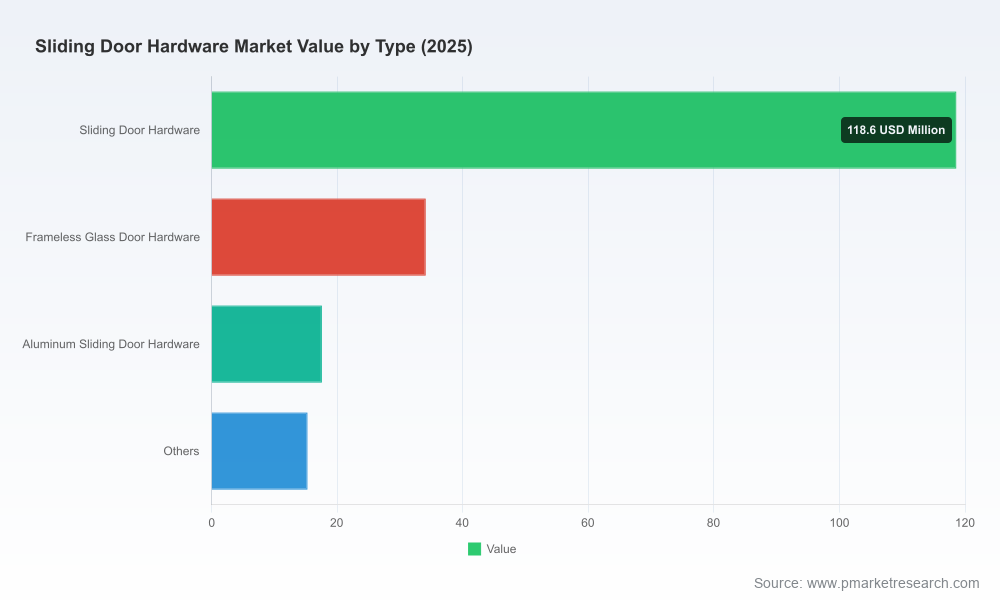

Sliding Door Hardware Market

Timing precision: 2026 will be the first full year in which several regulatory and standards changes (effective 2025) begin to impact procurement specifications, warranty liability constructs, and product design criteria. Our study translates those cascading effects into purchasing frameworks you can apply to 2026 budgets and RFPs.

Sliding Door Hardware Market

Resource planning: volatile raw-material and extrusion costs observed in 2024–2025 — including stainless steel and aluminum movements — are already altering supplier margins and lead-time profiles. The report models margin sensitivity under alternate raw-material scenarios so supply-chain and procurement leaders can set hedging and inventory policy for 2026.

Sliding Door Hardware Market

Competitive signalling: the market’s top-tier concentration metrics reveal a fragmented landscape with room for consolidation and product-led differentiation. We show where scale matters and where niche engineering capabilities create defensible margins — essential when prioritizing M&A targets or greenfield investments next year.

We designed this research as a practical toolkit for executives, product teams, and commercial leaders. Key deliverables include:

A validated market-sizing model (base year 2025) and a transparent forecast engine covering 2026–2032, with scenario toggles for high/low raw-material and regulatory impact.

Strategic segmentation framework: type, application, and regional layers mapped to buyer personas and specification drivers — presented as a decision matrix that links product features to procurement criteria (we intentionally withhold granular segment tables in this preview; full datasets are available in the complete report).

Supply-chain heatmap and supplier scorecards that evaluate cost-to-serve, lead-times, quality variance, and nearshore/onshore capacity options — enabling immediate supplier rationalization or dual-sourcing plans for 2026.

Regulatory and standards readiness checklist — a crisp playbook translating updated testing and certification requirements into product design and QA checkpoints for your 2026 launches.

Commercial playbooks: value-based pricing levers, specification playbooks for architects and contractors, channel prioritization, and go-to-market templates for premium vs. cost-competitive SKUs.

Investment and M&A dashboard: target scoring using growth, margin, technology, and integration complexity axes — plus modeled returns under debt and equity funding scenarios relevant for 2026 deal markets.

An interactive Excel model and accompanying narrative that connects assumptions to outcomes, so leadership teams can run “what-if” analyses during strategic planning cycles.

Material cost dynamics: 2024–2025 saw an uptick in stainless steel usage for corrosion-resistant components and a rise in aluminum extrusion pricing. These inputs will continue to exert near-term pressure on BOMs and will force trade-offs between durability and unit-cost in mid-market products. Our report quantifies the impact of +/- X% raw-material swings on typical product families.

Standards and certification: updated ANSI/BHMA and ISO testing requirements implemented around 2025 increase the bar for soft-close performance and vibration durability. For manufacturers and specifiers, this translates into redesign cycles and higher test-costs — but also an opportunity to differentiate through certified reliability in healthcare and multi-family segments.

Urbanization and product form-factor: the acceleration of space-saving sliding solutions in dense residential projects is not a fad — adoption is measurably higher in high-density markets. Product teams should treat minimalist, concealed and low-force systems as strategic bets for premium urban portfolios in 2026.

Procurement realities: lead-time reduction and improved quality were highlighted in recent product catalog updates by major vendors, underscoring the competitive value of supply-chain optimization. Our supplier scorecards show which firms have shortened lead-times through inventory localization and modular kit strategies.

The industry shows a moderate level of concentration with the top three firms controlling roughly a quarter of market share and the top five just over thirty percent — a footprint that implies both competitive pressure at scale and substantial opportunity for midsize specialists. Key competitor archetypes emerging from our analysis:

European system integrators (example: Häfele, Germany — https://www.hafele.com) — strong in full-system offerings, top-hung and bottom-rolling platforms, and durability-focused engineering for mixed residential/commercial portfolios. They compete on completeness of solution and channel partnerships.

Heavy-duty, specification-led suppliers (example: P.C. Henderson, UK — https://www.pchenderson.com) — tend to win large commercial and industrial projects where load capacity and robustness are the priority; their engineering capability suits large-door applications and specialized tracks.

Precision and premium-innovation players (example: Sugatsune, Japan — https://www.sugatsune.com) — focused on concealed hardware, low-force soft-close and furniture-grade fittings; these vendors capture high-margin residential and interior-architecture segments.

Regional manufacturers with product breadth (examples: KN Crowder, Pemko, Koil India, SeaLink Hardware, RW Hardware, Hager Companies, Klein) — their competitive vectors vary from North American-made value propositions and compliance focus to cost-effective volume supply. Recent product launches and catalog refreshes signal continued investment in operational efficiencies and new application-specific systems.

Our competitive intelligence package maps each listed firm to capability clusters (engineering R&D, channel reach, compliance readiness, cost position), a must-have for scenario planning whether your 2026 objective is to partner, acquire, or defend.

Product portfolio rationalization: prioritize engineering resources toward low-force, certified soft-close systems and modular kits that reduce installation labor. Use our ROI model to identify which SKUs to sunset vs. double-down on entering 2026.

Sourcing strategy: establish dual sourcing for critical stainless and aluminum components with clear escalation triggers tied to input-price thresholds. We provide supplier scorecards and a recommended two-tier sourcing timeline to operationalize this in Q1–Q2 2026.

M&A and partnership scouting: target firms that provide either (a) specification-heavy engineering capabilities for commercial projects, or (b) niche high-margin concealed hardware technologies. Our target-scoring matrix ranks candidates by integration complexity and accretion timing aligned to a 2026 deal calendar.

Go-to-market optimization: equip sales with specification playbooks and HVAC/architectural liaison kits to convert architect-led projects. Pricing tactics should reflect the incremental value of certified performance — not just commodity cost.

CEOs and corporate development teams: leverage the M&A dashboard and concentration analysis to define inorganic growth thresholds and markets where scale unlocks margin expansion.

Product and engineering leads: adopt the standards-readiness checklist and scenario model to time product revalidation and CAPEX for updated testing protocols.

Procurement and supply-chain heads: use the supplier heatmap to rebalance inventories and renegotiate contracts with indexed protections for raw-material swings.

Sales and marketing: implement the specification playbooks and buyer-persona mappings to shorten sales cycles in the architect and contractor ecosystems.

This report is a field-tested bridge between high-level market directionality and executable 90–180 day initiatives. It equips leadership teams with a validated 2025 baseline, a transparent 2026–2032 forecasting engine (5.2% CAGR), and the practical playbooks needed to convert insight into captured margin and defended revenue. Importantly, this preview intentionally omits detailed segment tables and certain granular datasets to protect the competitive integrity of our work and to encourage direct engagement with the full deliverable.

Access to the full report grants you the granular datasets, interactive models, supplier scorecards, and bespoke advisory time with our analysts to tailor the findings to your balance sheet and strategic plan. For PW Consulting clients and strategic partners, we also offer workshop sessions to integrate the model into your 2026 planning cadence.

To receive the complete study and schedule a briefing, please visit the source page linked in our distribution or contact your PW Consulting account lead.

For detailed analysis of this topic, please visit the official page:Sliding Door Hardware Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com