PW Consulting: Low Alpha Spherical Alumina Market Set to Grow at 14.02% CAGR, Reaching USD 664.92 Million by 2032

Other |

2026-07-02 04:36:25

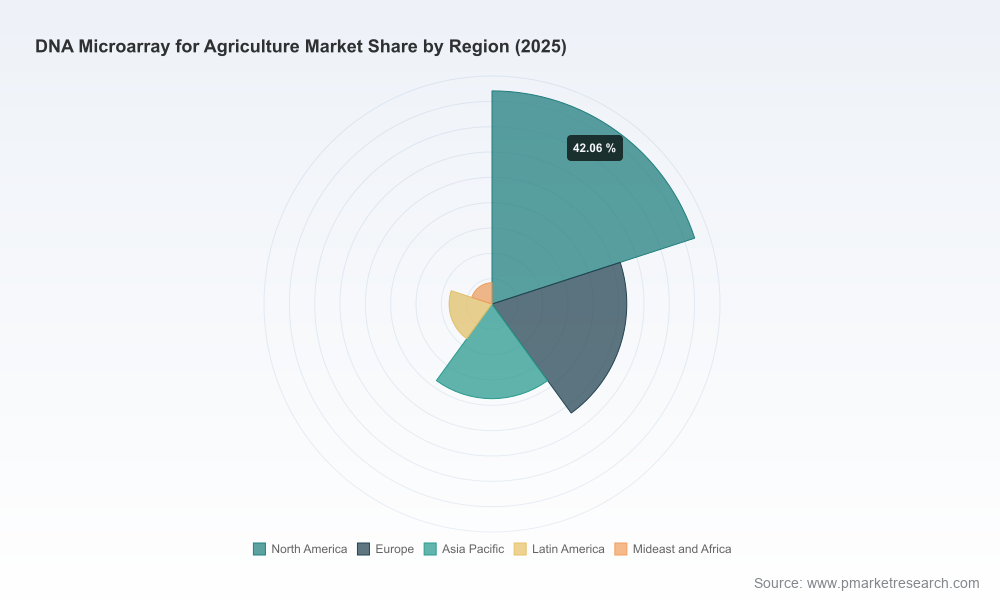

The DNA microarray segment targeting agricultural applications has moved from niche tooling to a reliable, decision‑grade technology for crop and livestock stakeholders. From a reported USD 153.44 Million in 2020, the market expanded to USD 215.0 Million by our base year (2025). With a projected compound annual growth rate (CAGR) of 6.98% through 2032, the market is expected to reach approximately USD 344.79 Million by 2032. That trajectory reflects a sustained demand for high‑throughput genotyping, expression profiling and targeted panels that enable breeding acceleration, trait discovery, pathogen surveillance and on‑farm diagnostics.

DNA Microarray for Agriculture Market

Prioritizing capital and R&D allocation — Buyers and investors must decide which analytical platforms (microarrays vs. sequencing vs. targeted assays) warrant near‑term capex and which require partnership or outsourcing. Our research quantifies the realistic commercial runway for microarray technologies over 2026–2032 and maps where incremental returns can be unlocked.

DNA Microarray for Agriculture Market

Vendor selection and procurement strategy — As institutions move from pilots to scale, procurement teams must align vendor capabilities with throughput, sample types and downstream bioinformatics. The report provides frameworks to assess supplier fit beyond simple price comparisons.

DNA Microarray for Agriculture Market

M&A and alliance scouting — Consolidation and strategic partnerships will accelerate. The study flags the types of assets (service labs, custom array manufacturers, bioinformatics stacks) that are most acquirable and valuation drivers for 2026 dealmaking.

Regulatory and IP positioning — With increasing regulatory scrutiny on genetic resources and data governance, the report helps firms build compliant commercialization pathways for panels and service offerings.

This publication is structured to equip executives, R&D heads and commercial leaders with immediately actionable evidence and tools. Highlights include:

Market sizing and forecast model — Transparent base‑year assumptions, historical trend decomposition (2020–2025) and scenario projections to 2032. The model is delivered in an editable spreadsheet so teams can substitute bespoke assumptions.

Adoption drivers and inhibitor analysis — Quantified impact analysis for key uptake levers (cost per sample, regulatory nudges, breeding cycle economics, and availability of trait markers) and practical mitigations for structural frictions.

Buyer personas and use‑case archetypes — Profiles for plant breeders, seed companies, livestock integrators and agritech service providers outlining decision criteria, procurement cycles and success metrics.

Vendor scorecards and procurement playbooks — Side‑by‑side capability mapping, sample throughput evaluation, service vs. product comparison, and a negotiation checklist tailored for 2026 procurement teams.

Technology and product roadmap — Comparative analysis of array chemistries, probe design strategies, and integration points with sequencing and digital phenotyping platforms.

Commercial playbooks — Go‑to‑market options for incumbents and new entrants, pricing elasticity tests, channel strategies and recommended pilot designs to demonstrate ROI to breeding and production stakeholders.

Risk assessment and mitigation — Supply chain sensitivity, single‑source dependencies, and contingency strategies for reagent shortages or IP disputes.

Note: The report intentionally refrains from publishing the granular region‑by‑region and application‑by‑application tables in this preview; detailed segment tables and country‑level breakdowns are included in the full report available on the source webpage.

The supplier ecosystem combines large life‑science conglomerates, specialist array manufacturers and service laboratories. The competitive map is heterogeneous: global platform providers market standardized arrays and related reagents, while specialist firms focus on custom designs and integrated service offerings for breeding programs.

Agilent Technologies (Santa Clara, CA; https://www.agilent.com) — Known for plant‑specific gene expression and exon microarrays, Agilent’s portfolio targets whole‑transcriptome analyses and species‑tailored expression profiling. Their strength lies in probe design expertise and established lab workflows that appeal to academic breeding programs and crop research centers.

Thermo Fisher Scientific (Waltham, MA; https://www.thermofisher.com) — Offers Axiom and Eureka genotyping arrays that emphasize high‑throughput screening for crop improvement. Thermo Fisher’s ecosystem advantage includes sample‑to‑data automation and scale, which suits commercial seed companies aiming to accelerate marker‑assisted selection at scale.

Illumina Inc. (San Diego, CA; https://www.illumina.com) — While widely known for sequencing, Illumina also supplies genotyping arrays for major crops. Their products integrate into broader genomics pipelines, offering a compelling value proposition where microarray data is used in tandem with sequencing and imputation strategies.

Arrayit Corporation (Sunnyvale, CA; https://www.arrayit.com) — A specialist in custom DNA and protein microarrays, Arrayit caters to clients requiring bespoke panels optimized for agricultural gene expression and genotyping. Their appeal is flexibility—rapid turnarounds for tailored assay design and niche crop or livestock targets.

Eurofins Genomics (Ebersberg, Germany; https://eurofinsgenomics.eu) — Positioned as a service provider with genotyping and expression platforms, Eurofins supplies portfolio services for plant breeding and agrigenomics customers seeking outsourced testing and integrated analytics.

For 2026 decisions, firms should evaluate vendors across four dimensions: (1) technological fit for the target species and traits; (2) scalability and total cost of ownership; (3) data lifecycle support including bioinformatics; and (4) commercial flexibility (custom design vs. catalog products). Our full vendor matrices provide weighted scoring against these criteria to simplify shortlisting.

The market’s 6.98% CAGR reflects a blend of steady adoption by conservative enterprise buyers and acceleration in targeted use cases. Key dynamics to consider:

Complementarity with sequencing — Microarrays remain attractive where targeted, cost‑efficient screening is required. Companies should treat arrays as complementary tools within a broader genomics toolkit rather than binary alternatives.

Value capture is shifting to services and analytics — As raw assay costs compress, margins and differentiation increasingly derive from bioinformatics, interpretation, and integration services that translate signals into breeding decisions.

Regulatory and data governance constraints — Ownership of genomic datasets and compliance with access‑and‑benefit frameworks will shape partnership structures and commercialization routes.

Fragmented buyer landscape — Diverse species, breeding timelines and regional regulatory regimes mean go‑to‑market strategies must be tailored. Standardized global products will coexist with highly customized local solutions for years to come.

Near term (0–12 months): Run focused pilots that compare array designs against low‑cost sequencing for target breeding objectives; adopt a vendor scorecard to select 1–2 preferred suppliers; lock in data standards and sample logistics contracts.

Medium term (12–36 months): Invest in bioinformatics capacity and data management to monetize accumulated genotype data; negotiate partnership terms that include IP delineation and data usage rights; explore managed‑services arrangements to avoid heavy upfront instrumentation costs.

Long term (36+ months): Consider bolt‑on acquisitions or strategic partnerships to secure differentiated panels or analytics; develop internal capabilities for probe design to reduce dependence on third‑party custom shops; build multi‑year procurement pipelines to achieve price stability at scale.

Key performance indicators to monitor include turnaround time per sample, actionable marker discovery rate, downstream trait adoption velocity in breeding programs, and revenue per sample for service providers. These KPIs map directly to time‑to‑value and should be integrated into any pilot acceptance criteria.

This preview outlines the strategic landscape and the types of operational playbooks that will matter in 2026. The full PW Consulting report provides the granular datasets, regional and application splits, vendor scorecards, and downloadable financial models that underpin the synthesis presented here. Those resources are designed so that strategy teams can plug the models into internal scenarios and derive precise investment cases.

For decision‑makers preparing budgets and R&D roadmaps in 2026, the central takeaway is pragmatic: DNA microarrays for agriculture are neither a passé technology nor a universal solution. They occupy a durable, evolving niche where focused, well‑executed deployments—backed by analytics and services—can materially accelerate breeding and surveillance outcomes. Use the market trajectory and operational frameworks in this preview as the starting point; the full report provides the granular inputs required to convert strategy into measurable results.

For detailed analysis of this topic, please visit the official page:DNA Microarray for Agriculture Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com