IV Drip Dubai: Accelerate Post-Surgery Recovery & Healing 2026

Health |

2026-03-18 10:32:48

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise, high-value preview of our latest PSIM market study — designed specifically to inform critical enterprise decisions in 2026. This article demonstrates the kinds of evidence-based, operationally-oriented insight you will find in the full report, while intentionally withholding the granular segment tables and proprietary breakdowns that make the study indispensable for procurement, architecture, and M&A planning.

Physical Security Information Management (PSIM) Market

PSIM is no longer a niche integrator function. Between 2020 and 2025 the global PSIM market expanded from a sub‑billion-dollar base to a mature market approaching a clear seven‑figure midpoint in USD millions. Our base-year assessment for 2025 places the market at USD 1,257.0 Million, and the model projects a robust compound annual growth rate (CAGR) of 16.3% across the 2026–2032 forecast horizon. By 2026 the market is forecast to exceed USD 1.46 Billion, and by 2032 it reaches a multi‑billion scale. That trajectory is significant: it reflects accelerating adoption of unified security platforms, migration to hybrid-cloud architectures, and the monetization potential of analytics-driven security operations.

Physical Security Information Management (PSIM) Market

Investment timing and scale: With a mid‑teens CAGR, PSIM vendors and platform integrators are scaling R&D and cloud investments rapidly. Enterprises evaluating refresh cycles for security estates should treat 2026 as a watershed year for negotiating cloud/hybrid terms, lock‑in provisions, and analytics licensing models that will compound costs or savings over the next decade.

Physical Security Information Management (PSIM) Market

Architecture choices: The migration to hybrid and cloud-enabled PSIM capabilities is material. Our analysis shows clear operational cost trade-offs between maintaining legacy, on‑premises orchestration versus leveraging distributed, cloud-managed orchestration — but the optimal choice is highly context dependent (regulatory posture, OT exposure, latency requirements). The full report includes decision frameworks that map workload types and security use cases to deployment patterns.

Vendor concentration and partner strategy: Market concentration remains modest; the top three vendors account for less than a quarter of the market, and the top five under 36%. This fragmentation creates opportunities for regional specialists, systems integrators, and cloud-native entrants — but it also increases the complexity of interoperability and long‑term support commitments for enterprise buyers.

Compliance and data sovereignty: New regulatory levers — notably EU Cybersecurity Certification regimes for critical infrastructure, NIS2‑related OT requirements, and GDPR/ENISA expectations around data locality and processing controls — are forcing PSIM architectures to embed compliance by design. Security architects must bake in certification pathways and contractual guarantees at procurement, not as post‑deployment remediation.

AI and event orchestration: Vendors are embedding AI at two layers — intelligent event correlation for operator prioritization, and automation for routine incident playbooks. Expect improved mean time to detect and respond (MTTD/MTTR) in controlled pilots, but be cautious about over‑reliance on opaque models without auditable decision trails. Our report provides a vendor‑agnostic maturity model for AI adoption in PSIM operations.

Hybrid deployment models: Cloud‑enabled control rooms and remote incident orchestration are now mainstream offers among leading PSIM vendors. However, hybrid models that retain local control for high‑assurance operations while leveraging cloud for analytics and long‑term storage are the dominant real‑world compromise. The study maps cost and risk vectors across these deployment patterns.

Hardware and maintenance complexity: Specialized sensors (for example fiber‑optic and calibrated thermal imaging) remain mission‑critical inputs to PSIM workflows. These devices require firmware discipline and specialized maintenance contracts — an often underbudgeted line item that materially affects total cost of ownership (TCO).

Interoperability stress points: The expanding array of best‑of‑breed VMS, access control, gunshot detection, and environmental sensors exposes integration gaps. Vendors are responding with more open APIs and standardized connectors, but systems integrators will continue to play a crucial role in normalization and lifecycle support.

The PSIM competitive set includes both long‑standing infrastructure incumbents and agile software players. Below I summarize the strategic positioning of the core firms analyzed in the report and recent moves that matter for 2026 planning.

Genetec Inc. (Montreal) — A software platform leader with a unified approach to IP video, access control, and automatic license plate recognition. Recent product moves include cloud‑first PSIM solutions and a global state‑of‑security report that highlights AI and hybrid cloud adoption trends. For enterprises, Genetec signals a strong path for cloud migration while retaining integrated analytics capability.

Honeywell International Inc. (Charlotte) — Historically an integrated systems and hardware provider, Honeywell is advancing a “Maximum Security” PSIM proposition that brings access, video, and intrusion into a single orchestration layer. Strategic partnerships (recently announced with cloud access control providers) indicate a channel‑centric route to hybrid deployments.

NICE Systems Ltd. (Ra'anana) — Focused on unified security management and event orchestration, NICE emphasises orchestration workflows and operator console efficiencies. Their pedigree in contact‑center and operational analytics enhances PSIM situational awareness for complex operations centers.

Milestone Systems A/S (Viborg) — Known for an open video management system (VMS), Milestone’s open architecture supports centralized management and analytics that are frequently paired with third‑party PSIM layers. This openness is attractive for buyers seeking modular supplier stacks.

AxxonSoft Inc. (Moscow) — Offers distributed PSIM software with strong video analytics and event automation, suitable for geographically dispersed estates. Their approach reduces reliance on centralized infrastructure, appealing to certain industrial and transport operators.

Advancis (Munich) — Vendor‑neutral PSIM with a focus on building and security management integration. Recent product releases emphasize identity management and vendor neutrality, which is relevant for complex enterprise estates with heterogeneous systems.

videoNEXT Federal, SureView Systems, Prysm Software (United States) — These players serve focused markets such as federal agencies, law‑enforcement integrated operations, and advanced analytics. Tactical partnerships and integrations (for example real‑time gunshot alerting and federal‑grade orchestration) are expanding the addressable market for higher‑assurance deployments.

Genetec’s 2026 State of Physical Security report and its earlier cloud PSIM launch indicate an aggressive push toward hybrid/cloud delivery and AI‑enabled operations.

Honeywell’s partnership announcements reflect traditional systems vendors leveraging cloud access partners to accelerate channel‑based cloud adoption.

SureView’s integration with third‑party real‑time detection systems (e.g., gunshot detection) underscores the commoditization — and commercialization — of public‑safety integrations within PSIM workflows.

Advancis’ feature upgrades for identity management demonstrate the ongoing premium on vendor‑neutral orchestration and identity correlation across multi‑vendor estates.

Strategic decision matrices that link security use cases (e.g., campus threat response, critical infrastructure OT protection, urban safety programs) to optimal PSIM architectures and procurement vehicles.

Vendor capability heatmaps and interoperability risk assessments — not as static scorecards but as playbooks for integration and lifecycle contracting.

TCO models that include equipment refresh, firmware and sensor maintenance, cloud consumption, and human capital costs for 3‑ and 7‑year horizons.

Regulatory compliance checklists keyed to regional certification needs (EU Cybersecurity Certification pathways, NIS2 impacts on OT environments, GDPR/ENISA data‑sovereignty controls) and contractual clauses to embed in vendor agreements.

M&A and partnership screening filters for corporates and integrators: how to judge target technology debt, data architectures, and field service footprints.

Use the macro trajectory and CAGR as a basis to stress‑test multi‑year security budgets and to renegotiate supplier SLAs with future migration pathways in mind.

Map high‑value pilot projects (hybrid control rooms, AI‑assisted incident playbooks) to operational KPIs and supplier milestones; insist on auditable AI outcomes and data locality guarantees.

Prioritise vendor‑neutral integration pilots where regulatory regime or OT exposure raises the cost of vendor lock‑in. Our report includes checklists and partner selection criteria to operationalize this approach.

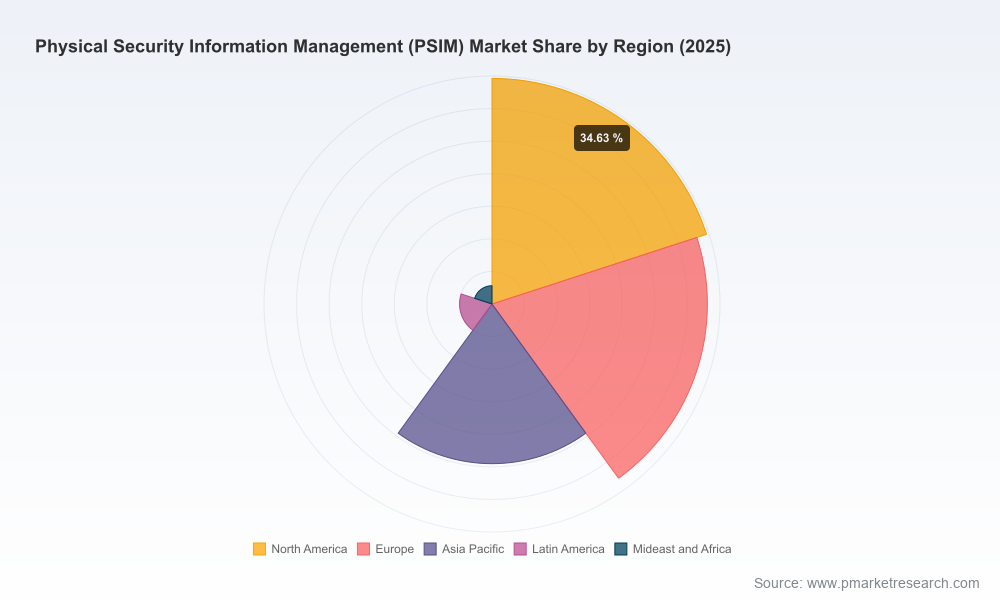

This article is a strategic preview: it surfaces the macro growth dynamics, regulatory vectors, competitive moves, and the operational trade‑offs that will dominate PSIM decisions in 2026. To preserve the investigative and commercial value of the study — and to protect the detailed segmented intelligence that drives tactical vendor selection and procurement bargaining power — we have intentionally omitted the granular regional, component, and deployment splits from this preview.

For enterprise architects, security heads, and M&A teams seeking the full dataset (including audited segment breakdowns, vendor scorecards, TCO worksheets, and playbook templates), please consult the full PW Consulting PSIM market report available through our research portal. It contains the detailed, actionable intelligence you need to make high‑confidence decisions in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Physical Security Information Management (PSIM) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com