Car Batteries Market 2026: Strategic Outlook and Decision Framework

Executive snapshot

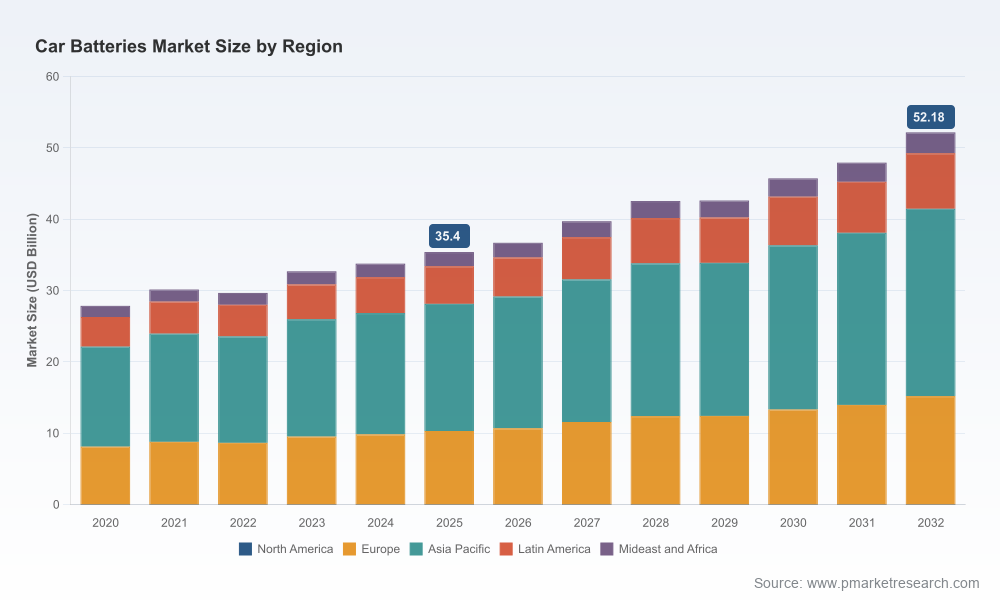

The car batteries market is navigating a complex, capital- and commodity-intensive transition. After recovering from pandemic-era distortions, the global market reached a materially larger base by 2025 and, under current structural drivers, is forecast to continue expanding through 2032 at a mid-single-digit compound annual growth rate (CAGR) of 5.75%. Market concentration is moderate: the top three firms control a meaningful share while the top five account for just over half of the market — a structure that supports both scale advantages and niche opportunity. For corporate leaders planning initiatives in 2026, the relevant questions are no longer whether the market grows, but how to capture higher-value growth pockets, manage raw-material exposure, and align channel and product strategies to evolving vehicle architectures.

Car Batteries Market

Market trajectory: what the macro numbers tell us

Viewed from a commercial planning horizon, the market’s trajectory from 2020 through the base year of 2025 demonstrates resiliency and a gradual step-up in demand and value realization. The base-year context and the forecast to 2032 reflect a market expanding from a solid pre‑pandemic volume into a diversified revenue pool that is increasingly shaped by hybridization, aftermarket dynamics, and battery-architecture segmentation. The market’s projected rise to the mid‑50s (USD Billion) range by 2032 underscores the importance of multi-year strategic bets — particularly around differentiated product lines, supply security, and channel orchestration — to capture disproportionate returns versus peers.

Car Batteries Market

Why this matters for 2026 decision-making

- Strategic timing: 2026 is the inflection year for several supply-side and regulatory dynamics. Decisions on capacity expansion, supplier contracts, and product roadmaps made in 2026 will determine whether a business is a cost leader, a high-margin specialist, or a vulnerable commodity producer by 2028–2030.

- Margin preservation vs. growth capture: With commodity volatility and trade interventions, companies must balance near-term margin protection (hedging, fixed-price contracts, localization) against longer-term growth capture via new chemistries and value-added services (e.g., battery-as-a-service, module integration).

- M&A and partnerships window: Moderate concentration combined with rising capital intensity creates a fertile environment for bolt-on acquisitions, technology-led partnerships, and strategic alliances with OEMs and tier-1 suppliers.

Segmentation and pockets of strategic opportunity (high level)

The market remains heterogeneous. Traditional lead‑acid technologies retain substantial share in legacy applications and replacement channels, while lithium-based architectures are driving much of the innovation agenda, particularly in higher-voltage, start-stop, and electrified drivetrains. Rather than presenting granular percentages, the report emphasizes the strategic implications of segmentation: where to prioritize investment in R&D, channel expansion, manufacturing footprint, and after-sales services to optimize return on invested capital.

Car Batteries Market

Competitive landscape: capabilities and likely strategic plays

The market combines global incumbents with deep manufacturing assets and regional specialists with strong distribution networks. Our competitive analysis in the report focuses on capabilities, strategic intent, and execution risk rather than revenue line-by-line comparisons, yielding actionable takeaways for market entrants and incumbents alike.

- Large integrated manufacturers (scale + channel): Firms with single-site, high-volume manufacturing and broad aftermarket reach are best positioned to defend commodity volumes and capture replacement demand. Expect continued focus on product portfolio optimization (e.g., enhanced AGM lines), channel exclusives, and retailer partnerships to protect share.

- Technology-focused incumbents: Established players investing in advanced lead‑acid variants and hybrid-ready chemistries will pursue OEM qualification, premium aftermarket segments, and co-development with vehicle manufacturers to sustain margins.

- Regional specialists and contract manufacturers: These players exploit cost advantages and localized market knowledge. Their strategic playbook commonly includes aggressive service networks, fast time-to-market for regulatory changes, and opportunistic OEM partnerships.

- Tier-1 and systems suppliers: Automotive component suppliers are integrating thermal management and battery-system competencies, targeting OEMs seeking turnkey electrical architectures. Their advantage is systems-level integration and established OEM relationships.

Company highlights (illustrative, strategic implications)

- East Penn Manufacturing: Global footprint and deep flooded/AGM production capability. Recent product-line refreshes and a dedicated EV/hybrid navigation section signal a dual focus on defending traditional volumes while preparing for electrified architectures.

- GS Yuasa & Furukawa Battery: Japanese technology orientation with strengths in high-performance lead‑acid and hybrid applications, making them natural partners for OEM electrification programs.

- Exide & Kung Long Batteries: Regional powerhouses with cost-efficient manufacturing and entrenched replacement channels — ideal platforms for rapid aftermarket expansion and contract manufacturing.

- Clarios, Robert Bosch, Denso, EnerSys: These firms bridge systems-level capabilities, OEM integration, and aftermarket distribution; expect continued investment in module systems and thermal management to support higher-margin vehicle electrification projects.

Supply-side dynamics and regulatory noise — what keeps CFOs awake

Raw-material and trade-policy upheavals have become central to go-to-market calculus. Several supply-side shocks and regulatory moves have already reshaped sourcing strategies and cost planning:

- Commodity cycles: Lithium carbonate experienced a significant rebound into early 2026 following mid‑2025 lows, a reminder that price decks can shift rapidly and materially — impacting lithium‑based battery cost assumptions and project-level IRRs.

- Trade barriers and export controls: Large tariffs, export controls on critical battery components, and quota regimes for key inputs have increased the premium on diversified sourcing and local content strategies.

- Raw-material policy: Changes in cobalt export policy and other resource restrictions highlight geopolitical exposure in supply chains and increase the value of vertical integration or long-term offtake agreements for essential inputs.

Risk matrix and mitigation playbook

Our report includes a practical risk matrix linking operational, market, and regulatory threats to mitigations that are executable within 6–18 months. Highlights include:

- Supply risk mitigation: multi-sourcing, strategic stockpiles, and supplier co-investments to secure critical components.

- Price risk management: structured hedging strategies, index-linked contracts, and pass-through clauses for key materials.

- Regulatory hedges: dual‑jurisdiction production footprints and compliance playbooks to manage tariff and export-control volatility.

- Technology risk: modular product architectures and staged R&D investments to preserve optionality between lead‑acid and lithium chemistries.

What the full PW Consulting report delivers (actionable, not academic)

The research package is designed for commercial and operating leaders who must translate market signals into executable plans. Key deliverables include:

- Market sizing and scenario-based forecasts with sensitivity to commodity price and policy shocks.

- Supply-chain maps and risk heatmaps that identify concentration points and candidate mitigations.

- Competitive capability profiles and playbooks for market entry, expansion, and consolidation.

- Go-to-market templates for aftermarket scaling, OEM qualification pathways, and channel partnership structures.

- M&A and partnership screening frameworks, with shortlists for bolt-on acquisitions and JV candidates tailored to buyer objectives (scale, technology, or distribution).

- Operational levers: capital expenditure models, site-location decision tools, and ramp profiles for capacity investments.

How leading firms should use this intelligence in 2026

Use the analysis to convert uncertainty into repeatable decisions. Practical first moves include:

- Run a 90‑day supply-security audit focused on high‑impact materials and single-sourcing risks; establish contingent sourcing contracts where exposure is highest.

- Prioritize product development investment using a stage‑gate that values OEM qualification potential and aftermarket margin elasticity.

- Revisit channel economics: quantify retailer vs. service-center strategies and deploy pilot programs to test value-added services such as warranty extension and battery-health analytics.

- Define capital-allocation guardrails that preserve optionality — staged capacity build with trigger events tied to clear commercial milestones.

Closing: the strategic edge

The car batteries market offers a blend of defensive and offensive opportunities through 2032. Defensive moves protect legacy volumes and margin, while offensive plays — in advanced chemistries, systems integration, and aftermarket services — create asymmetric upside. Our 2026-focused guidance is straightforward: secure supply, preserve optionality, and attack higher-margin pockets with differentiated product and channel strategies. The summary above provides the directional map; the full PW Consulting report contains the granular scenarios, supply‑chain nodes, and competitive scorecards required to build and execute a year‑by‑year plan.

Next steps

If your team is preparing budgets, investment memoranda, or strategic roadmaps for 2026, the full report is designed as a working dossier — not a passive read. It contains the datasets, supplier lists, and playbooks necessary to move from strategy to execution. For access to the complete segment-level analysis, scenario models, and supplier intelligence, refer to PW Consulting’s full Car Batteries Market report.

For detailed analysis of this topic, please visit the official page:Car Batteries Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com