IV Bags Market 2026 Strategic Brief — Why PW Consulting’s IV Bags Market Study Is a Must-Read for 2026 Decision-Makers

As health systems rebalance post-pandemic, IV therapy remains a core delivery channel for fluids, electrolytes, and parenteral drugs. Our PW Consulting IV Bags Market Study (base year 2025; historical 2020–2025; forecast 2026–2032) translates macro momentum into actionable guidance for manufacturers, buying groups, hospital systems, and private-equity sponsors planning for 2026 and beyond. The report synthesizes measured growth projections with regulatory inflection points and supplier behaviour to deliver a decision-useful narrative — while reserving the granular commercial datasets and segment-level forecasts for the full report accessible on our site.

IV Bags Market

Market Trajectory: Quantified, Stable, and Improving

At a macro level the IV bags market demonstrates steady expansion. Measured in USD (Billion), the market grew from a market size of roughly USD 2.94 billion in 2020 to about USD 3.90 billion in 2025. Our forecast framework projects the market to pass USD 4.1 billion in 2026 and to approach USD 5.8 billion by 2032, reflecting a compound annual growth rate (CAGR) of approximately 5.8% across the 2026–2032 forecast window.

IV Bags Market

For executives this profile signals three planning imperatives for 2026: (1) capacity expansion and supply-chain resilience to capture near-term volume growth, (2) disciplined product and channel portfolio management to protect margins as material mixes shift, and (3) regulatory readiness to avoid stoppages and recall-related disruptions that can cascade through procurement and clinical operations.

IV Bags Market

Key Dynamics Shaping 2026 Decisions

- Regulatory-to-Product Reconfiguration: Emerging regulation — from state-level bans on certain plasticizers to intensified EU and FDA guidance on polymer compatibility — is accelerating transitions away from legacy PVC/DEHP systems. Manufacturers and hospitals must model the profitability and timeline implications of switching to autoclave-compatible, non-PVC polymers.

- Cost Impact of Material Transition: The move to DEHP-free and non-PVC materials is not neutral: sector analysis indicates the average product cost of DEHP-free polymers is materially higher than legacy PVC. Procurement and pricing teams need to translate these cost delta scenarios into contract renegotiations and clinical substitution strategies.

- Quality and Recall Risk: High-profile recalls and product integrity events over 2024–2025 underline the cost of lapses in sterile-fill and particulate control. Quality assurance investments and supplier audits are no longer optional; they are essential risk-management levers.

- Consolidation & Concentration: The market remains moderately concentrated: the three largest suppliers account for a commanding majority of supply, and the top five exert even greater share of influence. For buyers this concentration simplifies strategic sourcing but increases exposure to single-supplier disruptions.

Competitive Landscape — Who Matters and Why

Our study profiles the active global participants that shape capacity, technology trends, and pricing dynamics. Leading players include established medtech and pharmaceutical-packaging specialists with vertically integrated sterile-fill capabilities, as well as niche converters offering multilayer technologies and connector systems. Representative profiles (summarized here) include manufacturers with global sterile-fill platforms, sustainability-focused producers, and specialists in dual-chamber and high-volume empty bag formats.

- Baxter International Inc. — A leading supplier of flexible IV solutions with extensive sterile-fill capacity and a strategic focus on premixed products to meet rising hospital demand.

- B. Braun Melsungen AG — A Europe-rooted player emphasizing non-PVC, DEHP-free options and sustainability certifications; active in regulatory engagement and voluntary quality actions.

- Fresenius Kabi AG — Known for proprietary bag technologies optimized for sterile filling and drug-delivery integration, with recent product initiatives targeting eco-friendly materials.

- Sippex SAS — A specialist converter producing PVC, multilayer polypropylene, and EVA empty bags and associated connectors, focused on pharmaceutical customer specifications.

- ICU Medical, Inc. — Competitive in non-PVC/non-DEHP container formats and closed-system transfer systems that reduce occupational exposure and contamination risk.

- Nipro Corporation — Offers differentiated dual-chamber systems and high-volume manufacturing suited to parenteral mixing and regional supply contracts.

Recent company-level moves in early 2026 reinforce strategic themes: some players are expanding sterile-fluid capacity in the U.S. to meet premix demand, while others are launching PVC-free product lines to position for tightening regulation and buyer sustainability mandates. These tactical choices matter to procurement and corporate strategy teams evaluating supply-line redundancy, price pressure, and innovation partnerships for 2026.

Operational & Commercial Imperatives for 2026

- Capacity Planning with Scenario Flexibility: Use multi-scenario capacity models that incorporate both accelerated DEHP bans and slower, market-driven material migration. Flexibility options (co-packing, toll-filling arrangements) reduce stranded-capacity risk.

- Raw-Material Hedging & Supplier Diversification: Given the observed premium for non-PVC polymers, structure long-term supply agreements with indexed pricing and shared-cost migration clauses. Consider dual-sourcing critical polymer and connector components.

- Quality-by-Design Investments: Expand particulate-control and sterility-test capabilities. Buyers should demand transparent process validation packages and recall mitigation playbooks as part of procurement evaluations.

- Value-Based Contracting & Price Pass-throughs: Clinical buyers should negotiate contracts that recognize the incremental cost of safer, eco-friendlier materials while extracting value through service levels, shelf-life extension, and bundled logistics.

- M&A & Strategic Partnerships: The competitive footprint favors bolt-on acquisitions and minority investments in niche converters and sterile-fill specialists to secure technology routes (e.g., dual-chamber systems, multilayer PP films).

What PW Consulting’s Full Report Delivers (Practical, Deployable Content)

The full IV Bags Market Study is structured to move teams from insight to execution. Highlights include:

- Detailed market-size history (2020–2025) and a granular model with scenario-based forecasts to 2032, allowing CFOs to stress-test revenue and margin outcomes.

- Supply-chain mapping from resin producers through bag converters to sterile-fillers, with node-level risk scoring and mitigation tactics.

- Margin-impact analysis for material transitions (PVC → non-PVC/DEHP-free) including sensitivity tables and recommended contract terms to preserve gross margins.

- Regulatory matrix cross-walking U.S. state actions, EU MDR implications, and FDA guidance to likely timeline and compliance cost estimates.

- Competitive benchmarking with five-year strategic profiles, capacity maps, recent developments, and M&A activity signals by player and region.

- Go-to-market playbooks for manufacturers and distributors: tender playbooks, hospital-clinical adoption strategies, and private-label models.

- Investment and divestment shortlists, with a quantified rationale for buy-side diligence filters and a prioritized target list for executives seeking to expand sterile-fill or polymer capability.

- Appendices with methodology, data sources, supplier questionnaires, and a reproducible unit-cost model for internal use.

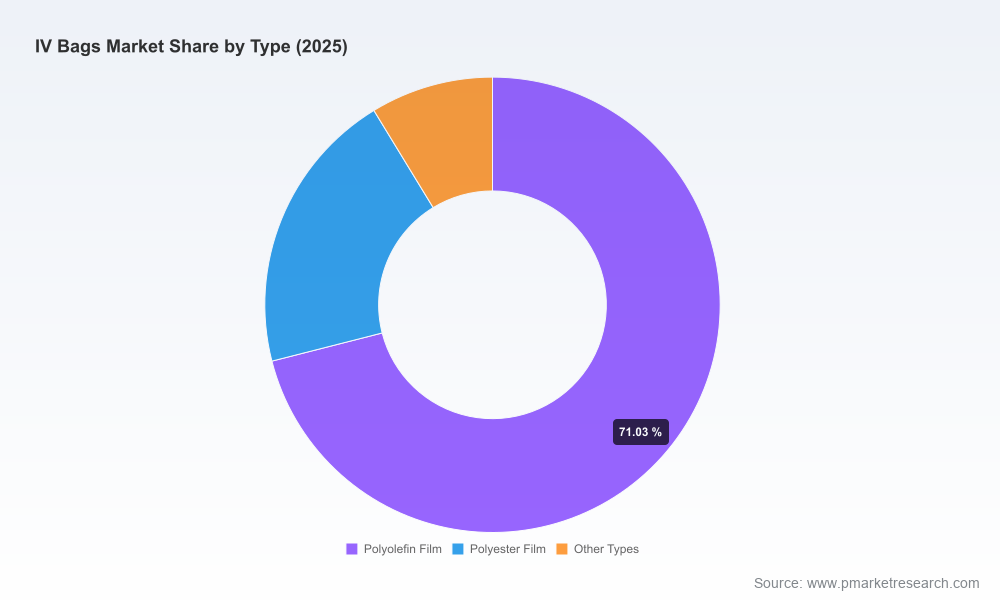

Note: To preserve the utility of this briefing and protect the commercial value of our datasets for paying subscribers, we have intentionally withheld the detailed segment and regional tables from this public summary. The full report contains the complete by-region, by-type, and by-application breakdowns together with downloadable spreadsheets and proprietary forecasts.

How to Use This Brief in 2026 Planning Cycles

- Boards & Strategy Teams: Use the macro trajectory and risk signals to validate capital allocation for sterile-fill expansions or alternative polymer investments.

- Procurement Directors: Request migration-pricing scenarios and quality packages from incumbent suppliers; augment contracts with performance and recall indemnities.

- Private Equity & Corporate Development: Use the M&A filters and target shortlist to prioritize roll-ups focused on non-PVC film capability and sterile-fill capacity in low-risk jurisdictions.

- R&D & Product Management: Align product roadmaps with autoclave-compatible polymer adoption and design products that optimize filling line throughput.

Conclusion — A Pragmatic Roadmap, Not a Forecast Alone

The IV bags market is forecasting steady growth through 2032 with a mid-single-digit CAGR, but 2026 is a pivot year where regulatory pressure, raw-material economics, and supplier concentration will define winners and losers. Our report turns those macro signals into practical, executable options for executive teams. For those responsible for procurement, manufacturing strategy, regulatory affairs, or M&A, the full PW Consulting IV Bags Market Study provides the granular, sourceable datasets and the actionable playbooks required to convert 2026 uncertainty into strategic advantage.

Access the full report for the complete by-region/by-type/by-application tables, downloadable financial models, and proprietary supplier scoring frameworks that support immediate decision-making.

For detailed analysis of this topic, please visit the official page:IV Bags Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com