A Complete Guide to RIDDOR Reporting in the Workplace

Other |

2026-06-25 12:00:50

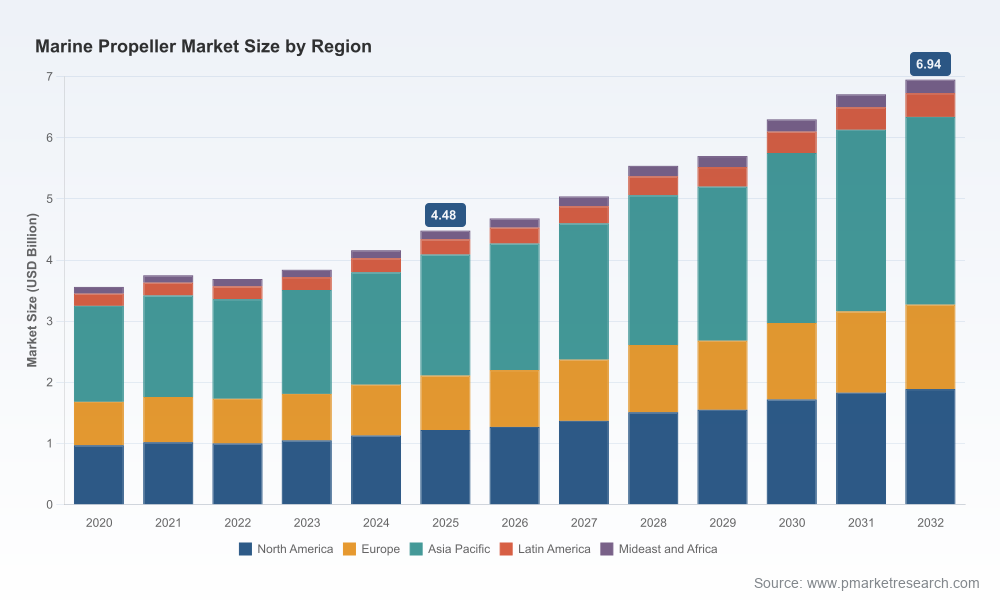

The marine propeller market is at an inflection point. After a measured recovery through the early 2020s, the global market has expanded from a base of roughly USD 3.6 Billion in 2020 to about USD 4.5 Billion in our 2025 baseline, and is projected to approach roughly USD 6.9 Billion by 2032. That trajectory represents a structural compound annual growth rate (CAGR) of 6.6% over the forecast window. For executive teams planning budgets, partnerships, and product roadmaps in 2026, this study reframes the propeller opportunity from a component sale to a systems-and-service growth engine.

Marine Propeller Market

2026 is the year many shipowners, OEMs, and aftermarket service providers will move from planning to execution. Regulatory signals (notably recent ISO and IMO guidance) combined with persistent cost pressures on raw materials and emerging trade-policy interventions are compressing strategic timelines. The market’s mid-single-digit CAGR masks a shift in profit pools: higher-value differentiated propeller technologies, rapid-response repair and retrofitting services, and integrated propulsion systems will capture disproportionate upside. Our research quantifies those shifts and translates them into actionable options for capital allocation, supply-chain protection, and go-to-market design.

Marine Propeller Market

Recovery and reacceleration: The market has rebounded steadily since 2020 and is on a multi-year growth path. Base-year 2025 data provide a practical pivot for 3–5 year strategic plans.

Marine Propeller Market

Concentration and competition: The top three and top five manufacturers account for a majority share of industry revenue, indicating a moderately concentrated supplier landscape. This concentration drives both bargaining power and acquisition opportunities for mid-sized participants.

Value migration: Revenue growth will be increasingly concentrated in higher-performance propeller designs, aftermarket optimization services, and digital-enabled maintenance offerings rather than commodity replacements.

Regulation drives design: New standards around component design and lifecycle emissions — for example recent ISO guidance on fixed-pitch hub design and IMO lifecycle GHG-intensity guidance — are raising technical entry barriers and creating product differentiation opportunities for firms that invest early in certification and testing.

Material and shipyard cost pressure: Upward movement in shipbuilding price indices and alloy costs has lengthened procurement lead times and elevated the unit economics of repair vs. replacement strategies. Firms that can compress lead times or offer certified retrofit pathways will command premium margins.

Trade and supply-chain resilience: Tariff conversations and targeted trade measures are prompting buyers to reassess sourcing footprints. Localized repair networks, qualified domestic casting and finishing partners, and contractual agility have become practical risk mitigants.

Technology convergence: CNC machining, advanced casting, and novel production approaches (including recent scaling of 3D sand-casting) are shortening production cycles and expanding design complexity that can be manufactured at scale.

The marketplace is a mix of legacy OEMs, specialized niche manufacturers, precision casting houses, and repair-and-service specialists. Below are distilled strategic profiles of representative players covered in our research, emphasizing how their capabilities map to emerging value pools.

Michigan Wheel — A legacy supplier with broad product coverage across recreational and commercial segments. Recent strategic divestments indicate a focus on core markets and product rationalization. Strategic takeaway: divestiture signals an opportunistic window for acquisitive competitors to consolidate geographic footprints, while Michigan Wheel’s redirected focus may improve service depth in prioritized segments.

VEEM Marine — High-precision CNC-led manufacturer with a portfolio tuned to high-speed and superyacht markets. Their engineering-to-manufacture integration positions them well for premium segments where hydrodynamic performance and low-vibration signatures command price premiums. Strategic takeaway: premium OEMs should consider co-development or white-labeling arrangements to accelerate product differentiation.

Sharrow Marine — Notable for patented blade geometries and rapid production scaling through an industrial partnership that slashes lead times. Recent launches of advanced multi-blade products combined with mass-production techniques create a hybrid model: patented performance at near-commodity throughput. Strategic takeaway: expect margin compression for copycat designs but defenses available through patent portfolios and manufacturing moats.

Nakashima Propeller — A global ocean-going propeller specialist with strong presence in made-to-order solutions. Their sourcing and product breadth make them a logical consolidator in markets where scale and customization intersect. Strategic takeaway: international OEMs should consider strategic alliances to secure long-lead, large-diameter propellers for commercial fleets.

AccuTech Marine Propeller — A service-focused player leveraging advanced diagnostic technologies for repair and tuning. Their positioning highlights aftermarket as a high-margin growth vector. Strategic takeaway: building diagnostic capability (scan/MRI-type tools) is a rapid path to aftermarket share and recurring revenue.

PowerTech!, Quality Castings Wisconsin, Anchor Miami Propeller — These firms illustrate three service archetypes: volume OEM-supply, precision casting for customized parts, and regional high-performance specialists. Strategic takeaway: suppliers with flexible casting capacity and regional service coverage will be vital partners for owners seeking minimized downtime.

Portfolio rationalizations and cross-border sales are reconfiguring supplier footprints and creating consolidation opportunities for strategic acquirers.

Manufacturing collaboration and production scaling initiatives are compressing time-to-market for new designs, which increases the importance of IP protection and fast product validation cycles.

Industry forums and trade events continue to accelerate technology transfer and buyer education — a useful runway for firms launching retrofit or efficiency-upgrade services.

This study is deliberately tactical. It combines proprietary market-sizing with scenario-driven financial modeling and operational toolkits designed for 2026 decision-making, including:

Forecast models with sensitivity to raw-material shocks, tariff scenarios, and accelerated regulation pathways.

Supply-chain maps highlighting critical nodes, lead-time hotspots, and near-term consolidation targets.

Commercial playbooks for OEMs, aftermarket service providers, and casting/finishing partners — including pricing levers, service-bundling tactics, and retrofit monetization frameworks.

Technology and IP landscape: patent trends, production-process benchmarking (CNC, advanced casting, and additive techniques), and recommended R&D investment priorities.

Due-diligence checklists and M&A scorecards calibrated to the market concentration dynamics and real-world deal precedents documented in the study.

Invest in certification early: Prioritize ISO/IMO-aligned product validation to win preferred supplier status with shipowners subject to lifecycle emissions scrutiny.

Build rapid-turn aftermarket capacity: A network of certified repair hubs and in-field diagnostic tools will capture high-margin retrofit spend driven by fleet operators seeking efficiency gains.

Hedge supply exposure: Use staggered contracts, dual-sourcing for key alloys, and nearshore casting partnerships to mitigate tariff and raw-material exposures.

Pursue bolt-on acquisitions that close capability gaps — particularly in advanced manufacturing, digital diagnostics, or regional service networks — to accelerate time-to-market without lengthy organic build cycles.

Monetize IP through licensing or white-label partnerships for premium blade designs to diversify revenue without heavy capex.

Use the study as a decision-support engine: map the forecast and scenario outputs to your capital expenditure calendar, procurement cycles, and product development sprints. The report’s operational toolkits are designed to plug into procurement RFx, M&A due-diligence, and product launch playbooks so that 2026 initiatives are founded on realistic lead-time, cost, and regulatory assumptions rather than aspirational targets.

This introduction demonstrates the depth and structure of PW Consulting’s Marine Propeller Market research: rigorous market-sizing, scenario-driven forecasts, and highly practical tools for executives. To preserve the strategic advantage for clients, detailed segmentation matrices, granular regional and application splits, and the full financial models are reserved for the full report. For a complete set of data tables, sensitivity analyses, supplier scorecards, and executable playbooks tailored to your company’s role in the value chain, access the full report and supporting annexes on our publications page or contact your PW Consulting account representative.

For detailed analysis of this topic, please visit the official page:Marine Propeller Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com