Embedded Software Market Size, IoT and Automotive Software Development Trends and Forecast to 2033

Networking |

2026-03-18 07:15:22

PW Consulting’s latest industry briefing frames the strategic choices that matter for market players entering 2026. This introduction summarizes the macro trajectory, competitive dynamics and the tactical playbook embedded in our full Organic Dairy Products Market study (base year 2025). It is designed as a “trailer”: we reveal the analytical logic and the high-level implications that should shape boardroom decisions, while reserving the segment-level detail and full model for subscribers and licensed users.

Organic Dairy Products Market

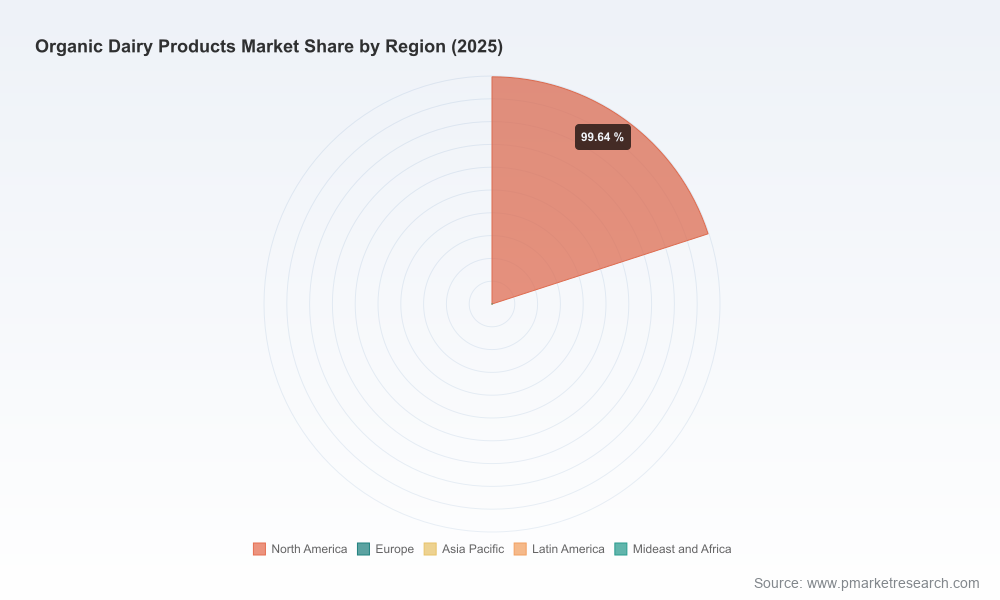

The organic dairy market has moved from a sizeable but still maturing category to a sustained growth sector. Our topline model—anchored on historical performance (2020–2025), a base year of 2025 and a forecast window from 2026–2032—shows growth from roughly USD 16.3 billion in 2020 to USD 21.51 billion in 2025. At a compound annual growth rate of 5.37% across our forecast horizon, the market is projected to approach approximately USD 31.0 billion by 2032.

Organic Dairy Products Market

Two implications are immediate for executive teams planning 2026 resource allocations: (1) the category is large enough to justify scale investments (manufacturing, cold chain, and branded marketing) but (2) growth is steady rather than explosive, which elevates the value of margin improvement, channel efficiency and product differentiation as sources of near‑term return.

Organic Dairy Products Market

Note: the full report contains the detailed segment tables, regional maps and downloadable financial model that underpin the above deliverables. Those granular elements are intentionally omitted here to preserve premium content value.

The competitive set combines farmer‑owned cooperatives, legacy processors and specialty craft brands. Three structural archetypes drive outcomes:

Representative profiles in the report illustrate the strategic tradeoffs for each archetype. For example, fully integrated processors benefit from sourcing control and SKU breadth but carry higher fixed costs and recall exposure; cooperatives have superior farmer alignment and resilience in supply but face capital formation constraints; specialty creamery players excel at premium positioning but must solve scale economics to expand without diluting brand authenticity.

Recent company‑level developments underscore operational risk and the need for robust recall playbooks: in March 2026 a prominent national brand initiated a voluntary recall related to packaging seals, and in May 2026 a regional creamery recalled select ice cream lots over potential foreign material. These events highlight two lessons: (1) even well‑established organic brands are vulnerable to supply‑chain and production integrity issues; and (2) traceability, rapid containment and transparent consumer communications materially mitigate brand erosion and regulatory fallout.

Market concentration metrics in our analysis indicate moderate fragmentation: the combined share of the three largest firms and the five largest firms remains below the concentration thresholds typical of highly consolidated consumer staples categories. This fragmentation creates space for consolidation, strategic alliances and differentiated go‑to‑market plays in 2026.

Feed and input costs continue to be a leading operational variable for organic milk economics. Observed market data points to elevated delivered costs for organic feed commodities during early 2026—the type of cost pressure that compresses margins unless offset by yield gains, sourcing innovations or price adjustments.

On regulation and programmatic support, two items are especially relevant for 2026 planning: the Origin of Livestock rule (effective 6 June 2022) which codified transition and ongoing management norms for organic herds, and the Organic Certification Cost Share Program, which continues to subsidize certification fees for qualifying producers (up to specified reimbursement caps). Together these shape herd transition timelines, certification economics and farmer onboarding strategies for brands and cooperatives that expect to expand organic lactating herd capacity.

Based on our scenario analysis and stress tests, PW Consulting recommends five priority moves for companies seeking to defend and grow position in the near term:

We designed the deliverables to plug directly into typical 2026 decision processes:

The organic dairy market’s steady CAGR (5.37% on our centralized scenario) and expanding absolute market size create a window in 2026 to convert brand strength into sustained margin improvement and share gains. However, the combination of input cost volatility, evolving certification rules and episodic operational risks means that passive strategies are unlikely to preserve competitive position.

PW Consulting’s full report contains the granular segment tables, regional breakouts, company dashboards and the financial model that underpin the strategic recommendations summarized here. For teams preparing budgets, M&A pipelines, or operational investments in 2026, the report provides the actionable intelligence and ready‑to‑use tools needed to move from planning to execution.

Contact PW Consulting or visit our publications portal to license the complete Organic Dairy Products Market report, download the financial model and book a workshop to translate findings into a 90‑day implementation plan for 2026.

For detailed analysis of this topic, please visit the official page:Organic Dairy Products Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com