Breaking: US Tire Pressure Monitoring System Market Poised for Rapid Growth

Other |

2026-07-02 10:19:55

As companies set budgets, capital allocation and product roadmaps for 2026, understanding where the Super Absorbent Polymer (SAP) market is heading is table stakes. This briefing — drawn from PW Consulting’s full SAP Market study (base year: 2025; historical window: 2020–2025; forecast: 2026–2032) — synthesizes the evidence you need to prioritize investments, de-risk supply chains and shape portfolio choices. We show the directional forces, competitive plays and practical strategic moves while intentionally withholding the granular sub‑segment numbers that are delivered in the full report to preserve commercial exclusivity for subscribers.

Super Absorbent Polymer (SAP) Market

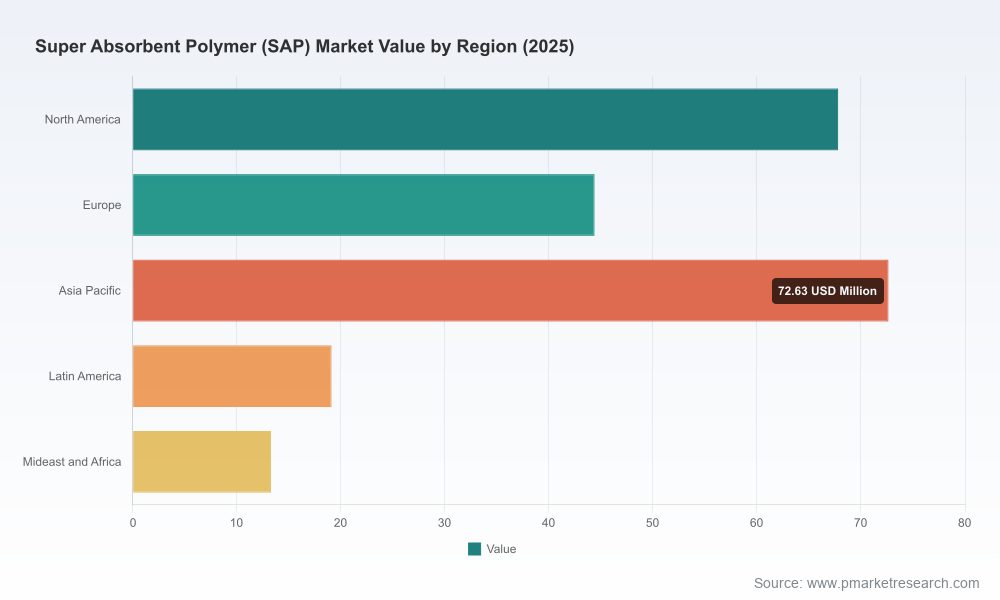

Market scale and growth: The SAP market expanded steadily from an estimated USD 168.5 Million in 2020 to USD 217.2 Million in 2025. Our forecast sees continued expansion through the 2026–2032 horizon, reaching approximately USD 352.1 Million by 2032 — an overall trajectory consistent with a mid‑single-digit CAGR (6.8%).

Super Absorbent Polymer (SAP) Market

Implication for 2026 planning: this pace of growth supports moderate to aggressive capacity investments for firms with credible access to feedstock and cost advantages, and cautions against speculative green‑field projects without secured offtake or feedstock integration.

Super Absorbent Polymer (SAP) Market

Demand composition and resilient end‑markets: Personal hygiene applications (disposables and adult care) continue to anchor demand, with agriculture, medical and industrial uses providing diversification. Buyers should plan for stable base demand with episodic upticks tied to demographic trends and regional sanitation programs.

Supply chain and raw material integration: Vertical integration on acrylic acid and adjacent intermediates materially changes cost curves. Recent disclosures from major producers show investments in on‑site or captive acrylic acid capacity across multiple geographies — a structural advantage for players that have it.

Capital intensity and scale economics: Capacity additions in Asia and low‑cost manufacturing hubs are compressing margins for undifferentiated grades. That said, specialty grades and sustainability‑certified products command a premium and create defensible niches.

Regulation, certification and ESG as market drivers: Product carbon footprint and certification are moving from marketing to procurement requirements. The market has already seen commercially scaled “zero product carbon footprint” claims combined with third‑party certification — a fast‑moving purchasing criterion in hygiene contracting and institutional procurement.

Market concentration: Competitive dynamics reflect a mix of global majors and regional capacity players. The structure favors firms that can combine technology, scale and integrated feedstock — but meaningful share and margin opportunities remain for innovators and value‑chain integrators.

Sustainability differentiation is real and investable: Leading producers have launched SAP variants that materially reduce product carbon footprint through renewable energy sourcing and biomass‑balance approaches, validated by internationally recognized certification frameworks. In 2025 several launches and certifications signaled that sustainability is now a procurement filter, not merely a stakeholder narrative.

Circularity and recycling roadmaps: Chemical recycling pilots for diaper-grade SAP are transitioning toward commercialization timelines. Companies that align pilot projects with branded offtake or OEM partners will capture early mover advantages in closed‑loop value chains.

Bio‑balanced and bio‑based formulations: Producers are balancing bio‑based offers with cost‑competitive acrylic chemistries. Early adopters in end markets that value low‑embedded carbon are rewarding certified suppliers with longer contract tenors.

Global integrators and technology leaders: Large chemical groups leverage global production networks, R&D scale and certification capabilities to serve hygiene and industrial customers with differentiated, sustainability‑aligned grades. Their playbook: protect high‑margin specialties, expand credentials, and selectively grow capacity where feedstock integration lowers unit costs.

Regionally scaled producers: Several manufacturers have invested heavily in scale and cost‑efficiency, focusing on high‑absorbency grades for hygiene markets and bulk supply agreements. Their strategic edge lies in volume economics, rapid capacity response and local customer intimacy.

Chinese and Asian manufacturers: Fast‑scaling local producers are increasing global competitiveness through large capacities, focused R&D portfolios and aggressive pricing in commoditized segments. For buyers, these firms present both procurement opportunities and competitive pressure for western producers.

What recent moves reveal: In 2025–2026 we observed three actionable signals: (1) product launches that tie sustainability credentials to premium pricing, (2) greenfield/expansion projects in Southeast Asia to capture regional diaper and agriculture demand, and (3) pilots of chemical recycling aimed at closing lifecycle A→Z loops for disposable hygiene. These moves delineate two winning plays: integrate upstream or differentiate downstream.

Prioritize feedstock security and vertical options: If you are a producer, accelerate negotiations for captive acrylic acid or long‑tenor supply agreements. For buyers, lock in multi‑year contracts with suppliers that demonstrate integration or sustainability certification to manage cost and reputational risk.

Invest selectively in sustainability credentials: Certification and transparent product carbon footprints are fast becoming procurement thresholds. Allocate program funding for product certification (ISCC or equivalent) and renewable sourcing pilots during 2026 to preserve premium channels.

Align capex with customer offtake and scenario tests: Use phased capacity ramps and tolling partnerships to avoid oversupply shocks. Scenario modelling should include demand shocks, feedstock price volatility and accelerated substitution in premium segments.

Targeted M&A and partnerships: Look for bolt‑on capabilities in chemical recycling, specialty grades and regional distribution that provide immediate margin uplift or deflation protection. Strategic tie‑ups with OEMs in hygiene can secure product design wins and long‑term take‑off volumes.

Differentiate through formulations and service: Compete on product performance (e.g., high CRC/high absorbency), certification and supply reliability rather than solely on price. End‑market customization (medical vs hygiene vs agriculture) reduces direct competition with large commodity suppliers.

Procurement playbook: Hedge price volatility with diversified supplier panels covering integrated incumbents, regional volume players and specialty innovators. Include sustainability KPIs in supplier scorecards and tie a portion of volumes to certified grades.

Verified market sizing (USD, Million) with historical series (2020–2025) and forecasts for 2026–2032, scenario modelling and sensitivity analysis based on price and demand shocks.

Segment dynamics and demand drivers by application and type, plus supplier economics and raw‑material pass‑through modelling.

Competitive intelligence: in‑depth company profiles, capability maps and recent strategic actions for leading global and regional players.

Regulatory and certification landscape, including sustainability pathways, ISCC considerations and certification impact modelling on procurement.

Practical playbooks: capex prioritization templates, supplier negotiation frameworks, go‑to‑market strategies for differentiated grades and M&A target screening criteria.

Proprietary tools: demand‑by‑usecase models, margin waterfall templates and scenario dashboards for board‑level briefings.

Note: to preserve the strategic value of the study for subscribers, the public summary intentionally omits granular regional and application share tables and detailed sub‑segment financials. These granular matrices and downloadable models are included in the full report available via PW Consulting’s publication page.

For executive teams preparing 2026 plans, the SAP market offers a clear trade‑off: scale and integration deliver defendable cost positions in commoditized grades, while sustainability, recycling and specialty formulations unlock margin premium and contracting durability. The market’s projected trajectory (base year 2025, forecast through 2032 at a 6.8% CAGR) supports investment — but only if it is paired with disciplined risk management: secure feedstock, validated offtake, credible sustainability credentials and flexible deployment of capital.

PW Consulting’s full SAP Market report packages the data, strategic frameworks and executable playbooks you need to move from intention to action in 2026. Contact PW Consulting to access the complete dataset, the sub‑segment matrices and the modelling tools that will inform your board’s next set of capital and commercial decisions.

For detailed analysis of this topic, please visit the official page:Super Absorbent Polymer (SAP) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com