Revealed: Nickel Zinc Rechargeable Battery Market Expected to Soar by 2035

Other |

2026-05-13 09:45:37

As companies reset priorities for 2026, the stone paper market is emerging from niche sustainability conversations into boardroom-grade strategic planning. This preview distills the signal from the noise: the market is not only growing, it is maturing into a space where procurement, brand positioning, regulatory compliance, and manufacturing strategy intersect. Our full Stone Paper Market study (base year 2025) provides the empirical foundation executives need; here we outline the high-level strategic implications while preserving the granular segmentation and proprietary analytics that drive transaction- and product-level decisions for paying clients.

Stone Paper Market

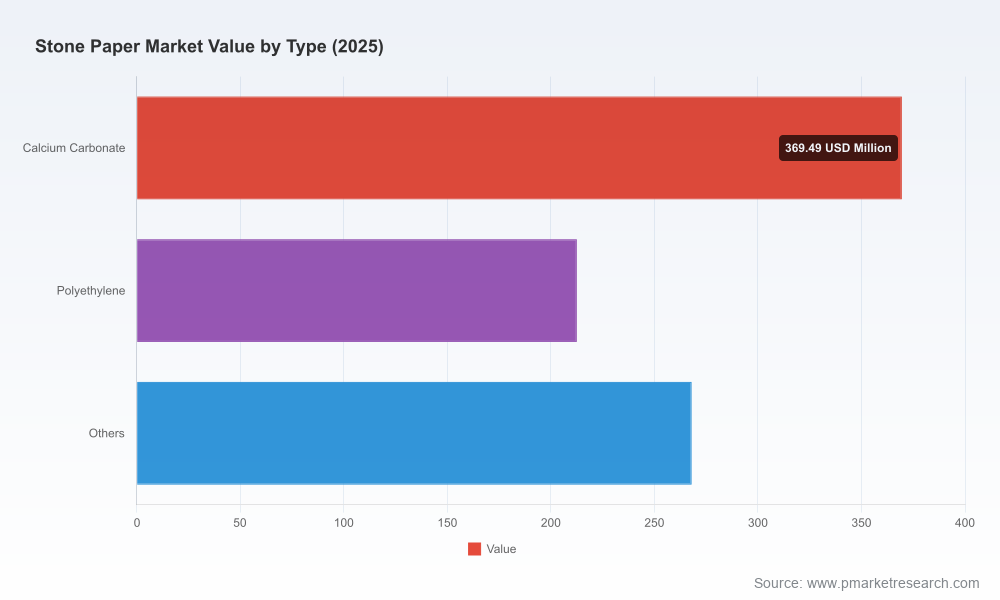

From 2020 through 2025 the industry expanded steadily, reaching a market size of USD 850.0 Million in 2025. Our forecast horizon (2026–2032) projects compound annual growth of 6.5%, taking the market to approximately USD 1,316.0 Million by 2032. That growth rate, sustained over multi-year horizons, has three important implications for corporate planning in 2026:

Stone Paper Market

The stone paper industry is best described today as moderately concentrated: the top three firms control a meaningful but not dominant share of the market, and the top five firms together account for a majority presence. This structure creates dual opportunities—scale advantages for incumbents and niche openings for specialized players. For 2026 strategy, this means: consolidation is possible but will favor acquirers that bring cost synergies (feedstock access, resin technology, distribution networks); innovators that solve downstream processing or certification issues can capture premium niches.

Stone Paper Market

Two external forces are shaping decisions now: Extended Producer Responsibility (EPR) regimes and raw material price dynamics. EPR policies in major markets are raising the cost of single-use plastic packaging and printed paper while creating substitution incentives for materials that demonstrate lower lifecycle impact. Select regional laws now compel producers to internalize end-of-life costs—an accounting shift that favors stone-based, recyclable or easily managed alternatives.

On the input side, calcium carbonate—an essential feedstock for stone paper—shows regional price divergence that matters to sourcing strategy. Price indices and recent spot reports indicate meaningful differences between markets, creating arbitrage and near-shoring incentives. For manufacturers reliant on mineral feedstock, hedging commercial exposure and securing FOB supply agreements are immediate priorities in 2026.

Understanding the moves of established players provides a practical roadmap. Three firms exemplify current strategies:

Based on our scenario modeling and client advisory engagements, we prioritize six strategic imperatives:

The full Stone Paper Market report (base year 2025; historical 2020–2025; forecast 2026–2032) translates the macro trends above into operational deliverables tailored for management and transaction teams. Key features include:

The market’s path is shaped by a handful of high-impact uncertainties: the pace and stringency of EPR rollouts, calcium carbonate price volatility, acceptance by major brands, technological advances in resin chemistry, and conversion-side barriers (printing, adhesive compatibility). Our report models five plausible scenarios and provides corresponding action matrices—enabling executives to set trigger-based plans rather than static forecasts.

For leadership teams making 2026 investment and sourcing decisions, the choice is not whether stone paper matters—it does. The critical questions are when and how much to allocate into capacity, partnerships, and product conversion. Our analysis shows a clear window for strategic advantage: early movers who combine supply assurance, certification credibility, and downstream convertibility can secure both margin and market share as the industry scales to over a billion dollars within the forecast horizon.

We intentionally leave the granular segmentation and proprietary dashboards behind the paywall of the full report. If your 2026 plan requires concrete numbers to model investments, access supplier-by-supplier benchmarking, or drill into regional demand curves and application-level economics, the full Stone Paper Market study contains those datasets, scenario models, and executable playbooks.

PW Consulting’s industrial materials team is available for briefings, scenario workshops, and tailored vendor diligence. Request the full report to convert this strategic preview into a 2026 action plan.

For detailed analysis of this topic, please visit the official page:Stone Paper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com