Budesonide Inhaler Market Insights and Growth Trends

Other |

2026-07-03 09:34:08

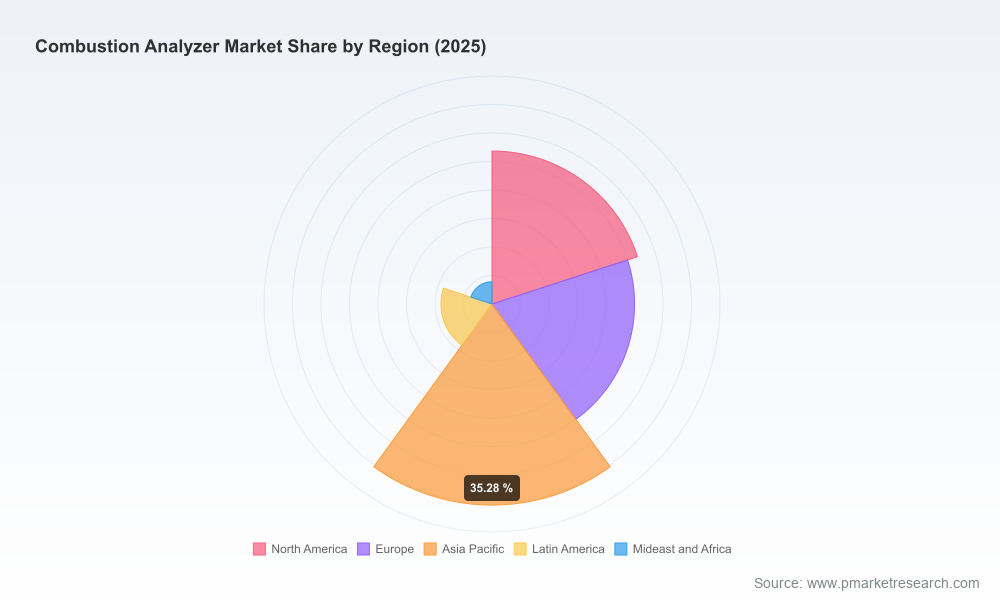

PW Consulting’s latest Combustion Analyzer Market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes the technical, regulatory, and commercial vectors that will determine winners and losers through the next investment cycle. With an aggregate market trajectory expanding at a 6.49% CAGR and top‑line market growth from the mid‑2020s into the early 2030s, the landscape is large enough to merit targeted plays but fragmented enough to reward disciplined strategy. This preview highlights the study’s strategic value for 2026 decision-making while deliberately withholding granular segmentation tables and regional/application breakdowns to encourage direct engagement with the full report.

Combustion Analyzer Market

Timing: 2026 is a turning point — regulatory enforcement, technician certification requirements, and fleet refresh cycles intersect to create an accelerated procurement window for combustion measurement tools and services.

Combustion Analyzer Market

Actionability: The report moves beyond descriptive market sizing to provide use-case driven decision frameworks — from procurement scorecards for facility managers to product roadmap priorities for OEMs.

Combustion Analyzer Market

Risk-adjusted planning: Our scenario models evaluate demand under multiple regulatory and energy‑transition outcomes, enabling capital planners and product teams to size investments with downside protection.

Across 2020–2025 the market demonstrated steady expansion, accelerating into 2025. Our base‑year synthesis shows the market measured in USD (Million) reaching a substantive level by 2025 and continuing to grow through the forecast window to 2032 under a central forecast path that compounds at 6.49% annually. This growth is underpinned by persistent replacement cycles, serviceable installed bases in commercial and industrial settings, and a renewed emphasis on emissions and indoor air quality that is driving both retrofit and new‑build demand.

For corporate decision‑makers evaluating CapEx and R&D allocations in 2026, the implication is straightforward: the market is large and mature enough to justify targeted investments (product feature differentiation, digital services, certification partnerships) but still amenable to disruption through software, sensor improvements, and integrated service offerings.

The full PW Consulting report is structured to support immediate tactical choices and medium‑term strategic planning. Highlights include:

Executive decision matrix — prioritizes actions by impact and implementation horizon for OEMs, distributors, and service providers.

Commercial playbook — channel segmentation, distributor economics, and a partner evaluation template for field service networks and training organizations.

Product and technology scorecard — sensor technologies, probe chemistries, software integrations (telemetry, mobile apps), and the cost/benefit of field‑replaceable components versus service contracts.

Regulatory and standards appendix — mapping of the most consequential local and national requirements that influence procurement specifications, including recent training and school-district level mandates that are already shaping buyer behavior.

Financial modeling toolkit — discounted cash flow templates, margin and pricing sensitivity analyses, and traderules for valuation in M&A and minority investments within the combustion measurement space.

Competitive benchmarking — proprietary vendor scoring across product breadth, service capability, channel reach, and R&D momentum (CR3 and CR5 concentration metrics included to help assess consolidation risk).

Field validation studies and case studies — operational TCO comparisons from live installations and commissioning projects across representative industrial and commercial contexts.

The market is characterized by a mix of specialist test‑instrument OEMs, industrial analytics suppliers, and safety equipment vendors. Market concentration metrics indicate a moderate level of fragmentation (our CR3 and CR5 metrics underpin this view), which creates opportunities for niche leaders and for consolidation in adjacencies (service, software, probes).

UEI Test Instruments (Tustin, CA) — recent product expansion and service guarantees mark UEI as an aggressive service‑led competitor. Their January 2026 ACA launch, coupled with same‑day recertification commitments, signals a strategic bet on shortening service cycles and increasing customer lifetime value through premium support offerings.

Fieldpiece Instruments (Orange, CA) — portfolio strength lies in field usability and wireless integration. Their touchscreen models and app ecosystems target HVACR professionals focused on workflow efficiency and job documentation — an area where software‑enabled diagnostics can generate recurring revenue.

Testo (Lenzkirch, Germany) — broad product span from portable residential tools to heavy‑duty industrial analyzers positions Testo as a supply anchor for institutional procurement. Recent deployments referenced in public compliance reports illustrate how vendor selection can be driven by specification-level mandates.

MSA Safety (Cranberry Township, PA) and Bacharach (New Kensington, PA) — focus on entry‑level and residential segments with high serviceability. Their strategy centers on ease of use, affordability, and channel penetration through safety distributors.

Sauermann, Seitron, Wöhler, Gerhardt, Emerson — these vendors reflect regional strengths, niche technical capabilities (e.g., emissions accuracy, zirconia oxygen probes), and differentiated certifications. Seitron’s NCI approval and industry recognition in late 2025 underscore how certification can be a meaningful competitive moat in HVAC markets.

Taken together, the vendor mix suggests three viable strategic archetypes for 2026: product incumbents doubling down on channel and service, software/service disruptors layering diagnostics and subscription services, and regional specialists exploiting certification and regulatory alignment. Each archetype implies different capital intensity and time-to-value.

Regulatory action and training standards are a near‑term accelerant. Localized initiatives — such as recent technical training classes emphasizing O2/CO/CO2/temperature/pressure measurement and school‑district source test requirements — are shifting procurement toward validated instruments and certified technicians. These dynamics have three direct implications:

Procurement specifications will increasingly include certified model lists and performance verification steps, favoring vendors with recognized certifications and robust calibration networks.

Training and certification partnerships become a strategic channel: vendors that embed technician certification, fast recertification, and equipment‑as‑a‑service will capture higher wallet share.

Public‑sector compliance work creates reproducible, large‑ticket opportunities for service providers that can scale verification and reporting workflows.

Buyers (facility owners, service contractors): Prioritize instruments with strong calibration networks and software traceability. Consider service bundles that reduce downtime and regulatory friction.

OEMs and product leaders: Invest in field‑replaceable sensors, app integration, and expedited recertification services. Use certifications as commercial leverage in regulated verticals.

Distributors and channel partners: Differentiate through value‑added training, bundled inspection services, and digital job management platforms that lock in recurring revenue.

Investors and M&A teams: Look for tuck‑in targets that provide either software for workflow automation or regional calibration/service footprints that accelerate nationwide coverage.

In keeping with our “trailer” approach, this article highlights strategic themes and actionable implications without publishing the granular region, product‑type, and application split tables contained in the full PW Consulting report. Those tables — along with vendor scorecards, model‑level pricing benchmarks, and an interactive dataset — are purposefully gated. Why? Because the most valuable competitive intelligence is context‑sensitive: companies must interpret segment elasticity, channel margins, and unit economics relative to their unique cost structures and go‑to‑market ambitions. The full report provides that context alongside calibrated recommendations you can act on in 2026.

Access the full dataset and scenario models to stress‑test your 2026 CapEx and R&D plans against regulatory tightening and accelerated technician certification trends.

Use our vendor scorecard to validate supplier choices before negotiating multi‑year service contracts.

Engage our advisory team for a tailored 90‑day go‑to‑market sprint that aligns product roadmaps, channel incentives, and certification partnerships to capture near‑term procurement flows.

Combustion analysis will remain a fundamental building block of safe, efficient thermal systems. In 2026, the companies that combine precise instrumentation with rapid service, software‑enabled workflows, and certification alignment will seize disproportionate value. PW Consulting’s full Combustion Analyzer Market study equips leaders with the data, frameworks, and vendor intelligence needed to make those choices with confidence.

For detailed analysis of this topic, please visit the official page:Combustion Analyzer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com