North America Frozen Fruit and Vegetable Market: Size, Share, and Growth Forecast 2025 –2032

Gardening |

2026-06-25 06:21:20

As PW Consulting’s lead industry analyst, I present an executive preview of our latest market research on Radiation Shielding Textiles. This briefing distills the signals that will matter to corporate strategy teams in 2026: where the market is coming from, where it is headed, what operational shocks to expect, and how leading suppliers are positioning. The analysis is intentionally directional — rich enough to shape near-term strategic bets while reserving full segment-level detail and datasets for the complete report.

Radiation Shielding Textile Market

The global radiation shielding textile market has demonstrated steady expansion through the 2020–2025 historical window and is forecast to continue growing through 2032. Our base-year view for 2025 places the market near USD 90 Million (revenue unit: Million USD). Under the assumptions and demand drivers modeled in the study, the market is expected to grow at a compound annual growth rate (CAGR) of approximately 5.1% across the 2026–2032 forecast horizon, bringing the market to roughly USD 130 Million by 2032.

Radiation Shielding Textile Market

Timing of investment and product development: A predictable mid-single-digit CAGR creates a window for disciplined, staged investment. Companies with near-term capacity or IP advantages can capture durable margins by sequencing investments with regulatory milestones and procurement cycles in healthcare and defense buyers.

Radiation Shielding Textile Market

Supply-chain reset and cost pass-through: Raw-material shocks and trade policy shifts have altered cost baselines for shielding fabrics. Procurement teams must reframe supplier engagement, hedging strategies, and contract tenors to protect margins while preserving lead-times.

Regulatory-driven product re-specification: Chemical and materials restrictions are actively reshaping allowable material mixes — driving alternative metallization techniques, metal-fiber blends, and non-lead ionizing shielding solutions. R&D and compliance functions must be aligned from product concept through market launch.

Historical growth from 2020 to 2025 shows a resilient adoption curve, supported by medical imaging expansion, industrial radiography, increased personal protection demand, and selective military procurement. Looking into 2026 and beyond, growth is sustained by incremental adoption in medical protective garments, expansion of technical textiles for industrial shielding, and continued innovation in lead-free materials for ionizing radiation protection.

Key structural characteristics to note:

Moderate market concentration: The market exhibits a moderate level of concentration among the largest suppliers. Our concentration metrics show the top three firms control a meaningful share of commercial volumes, with the top five materially increasing combined control — an important factor for competitive dynamics, pricing power, and standards-setting.

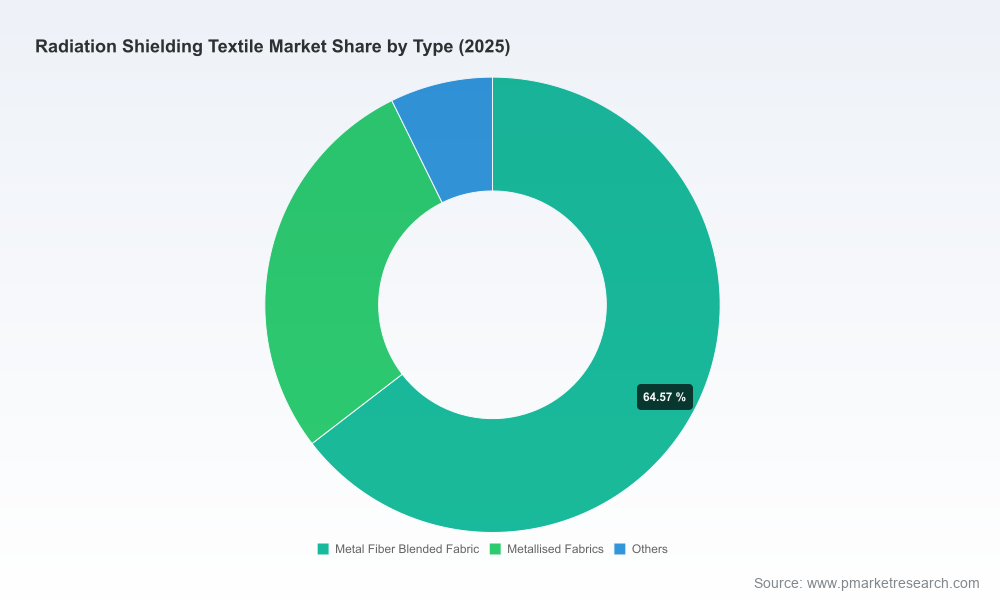

Technology bifurcation: Two technology pathways coexist — metallized/conductive textiles for electromagnetic and radio-frequency shielding, and dense, often polymer-metal composite fabrics engineered for ionizing radiation attenuation. Each pathway implies different supplier ecosystems, regulatory risk profiles, and route-to-market models.

Pricing and raw materials volatility: Lead and tungsten-related commodity movements, plus metal-coating input costs, feed directly into finished-goods economics. Market participants must plan for episodic cost inflation and potential sourcing bottlenecks.

Chemical restriction regimes: Existing restrictions limiting certain hazardous compounds in textiles continue to tighten product formulations and supplier qualifications. This affects legacy lead-containing products and PFAS-enabled finishes, prompting migration to compliant alternatives and new compliance costs.

Tariffs and trade barriers: Recent tariff actions have increased effective import costs in some markets, compelling buyers to re-evaluate nearshoring, dual-sourcing, and total landed-cost optimization more proactively than before.

Certification and medical-device alignment: In medical and occupational PPE segments, regulatory certification (including PPE and relevant medical device clearances) is a gating factor for procurement and reimbursement. Demonstrated durability and attenuation performance are becoming procurement differentiators.

Procurement playbook: Develop a supplier scorecard that integrates regulatory compliance, raw-material exposure, certification status, capacity flexibility, and logistics resilience. Lock in multi-year agreements with indexed pricing clauses where possible, and create contingency frameworks for material substitutions that do not invalidate certifications.

R&D and product strategy: Prioritize validation programs that align with buyer procurement cycles — focusing on durability testing, dose-attenuation performance, and washability where relevant. For firms competing on innovation, demonstrate FEA-backed design benefits and independent lab certifications to shorten buyer adoption timelines.

Commercial model refinements: Buyers are moving toward bundled solutions (textile + certification + service/maintenance) in high-value channels such as hospitals and defense programs. Consider offering consumption-based or managed-service pricing to capture greater lifecycle economics.

The full PW Consulting report is designed as a working toolkit for executives and functional leaders. Highlights include:

Market sizing and rigorous forecast model (base year 2025, historical 2020–2025, forecast 2026–2032) with scenario analysis and sensitivities for raw-material price swings and regulatory outcomes.

Detailed competitive benchmarking, including product portfolios, regulatory certifications, channel strategies, and recent strategic moves.

Go-to-market playbooks for Healthcare, Industrial, Military, and Consumer-adjacent channels — each with buyer decision-trees, procurement levers, and value-capture tactics.

Supply-chain stress tests and recommended procurement contracts, including clauses for material substitution, tariff shocks, and quality audits tied to certification renewals.

Technology & material roadmap options, with trade-off matrices comparing lead-free alternatives, metallization approaches, and composite architectures in terms of cost, manufacturability, and regulatory readiness.

Our vendor analysis focuses on established specialists and emerging challengers that shape sourcing, innovation, and standards within shielding textiles. The branded players below illustrate archetypal strategies relevant to buyer and investor decision-making.

Swiss Shield AG (Flums, Switzerland) — Known for high-tech yarns and fabric constructions aimed at high-frequency shielding. Their approach emphasizes material science and premium-brand positioning in garments and home textiles, an advantage where buyer trust and demonstrated attenuation performance are primary purchase drivers.

Shieldex (Statex, Bremen, Germany) — Specialist in metallized silver-plated fabrics and conductive textiles, serving technical and EMC markets. Shieldex exemplifies suppliers whose core competency is metallization and process control, which are critical in industrial and electronic-shielding use-cases.

Radiation Shield Technologies (RST, Miami, USA) — The commercial face of Demron® and lead-free ionizing protection solutions. RST’s product strategy highlights differentiation through material substitution (lead-free) and product-system configurations (suits, blankets, tents) for medical and tactical customers.

Texray AB (Sweden) — A notable innovator with textile-based radiation protection systems certified under PPE and FDA regimes. Recent durability and dose-reduction study results have strengthened their value proposition for medical professionals — a signal that validated product performance can accelerate market uptake in credential-sensitive channels.

Joyncleon (China) — Represents cost-competitive scale suppliers focused on maternity and consumer apparel segments. Their advantage is manufacturing scale and access to large apparel supply chains; however, margins and differentiation depend on certification and branding investments.

Metal Textiles (France) — Specialized producer of metal-coated and metallized fabrics for shielding applications, reflecting the continuum of suppliers that dominate certain technical niches where process expertise is a barrier to entry.

Collectively, market leadership combines technical IP, validated certifications, and global distribution reach. The top tier’s share of global volumes underlines the importance of strategic partnerships and certification-led differentiation.

Durability as a procurement differentiator: Independent testing confirming multi-hundred-thousand flex-cycle durability and significant dose-reduction in clinical settings has immediate procurement implications: buyers increasingly require lifecycle proof-points rather than single-parameter claims.

Raw material and geopolitical exposure: Commodity and trade developments have materially influenced landed costs and sourcing choices. Companies should re-assess material exposure (including tungsten and lead alternatives), examine tariff mitigation strategies, and consider multi-region sourcing to reduce single-point-of-failure risk.

Regulatory drag and innovation opportunity: Restrictions on certain chemical classes and legacy heavy-metal content create near-term compliance costs but open an innovation window for companies that can commercialize certified, lead-free, and PFAS-free material systems.

CEOs and corporate strategy teams: Use the forecast scenarios and supplier heatmaps to set three-year capital plans and M&A targets aligned with certification-led differentiation.

Supply-chain and procurement heads: Implement the supplier scorecard and contract templates to mitigate cost and regulatory risk, and pilot multi-sourcing in critical material families.

R&D and product management: Prioritize validation programs that convert performance claims into certified procurement criteria; accelerate trials with key hospital systems or defense buyers to shorten adoption cycles.

This preview highlights the strategic inflections we expect to drive value capture in 2026: certification-backed product performance, supply-chain resilience amid material and trade volatility, and focused commercialization in higher-value channels. For teams ready to convert insight into action, the full PW Consulting report provides the detailed segment-level modeling, supplier scorecards, pricing ladders, and playbooks necessary to implement the moves outlined above. Access to the complete dataset and proprietary scenario models is available through our research portal.

For detailed analysis of this topic, please visit the official page:Radiation Shielding Textile Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com