Low Pressure Molding with Polyamides Market: Strategic Outlook for 2026 Decision-Makers

As PW Consulting’s senior industry analyst, I present a focused strategic preview of our new market research on Low Pressure Molding (LPM) with polyamides. This briefing is designed to help executives, product leaders, supply‑chain managers and investors orient their 2026 decisions around a technology and material combination that is transitioning from niche protection to mainstream encapsulation across electronics, automotive and industrial applications.

Low Pressure Molding with Polyamides Market

Why this market matters now

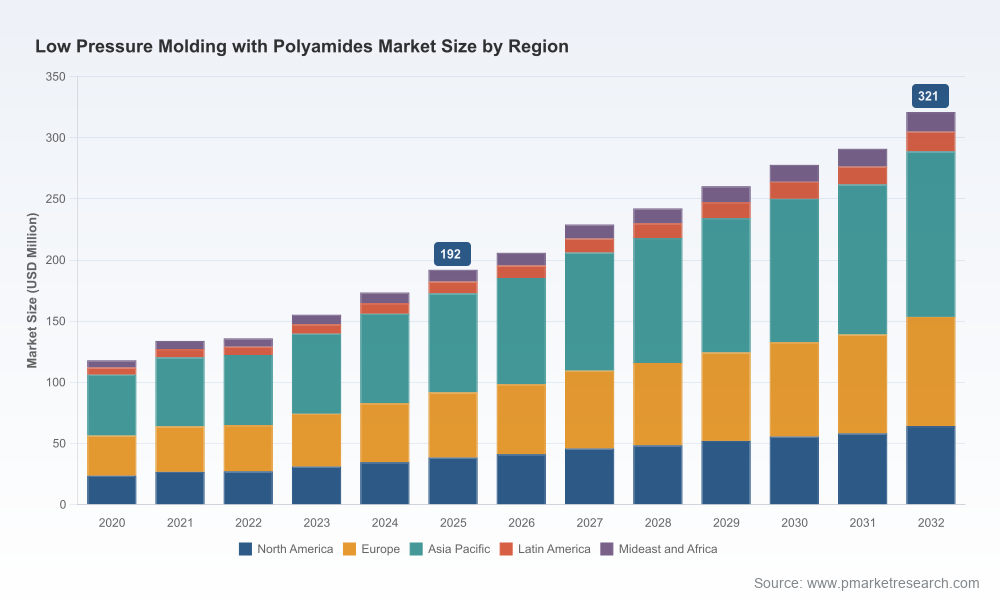

Low Pressure Molding with polyamides is no longer an experimental option. Over the past half‑decade the market has evolved from early adopter use cases into commercially scaled production lines. Our macro view shows the total market expanding from roughly USD 118 million in 2020 to about USD 192 million in 2025. With continued adoption and product evolution, we project further growth through the 2026–2032 forecast window at a compound annual growth rate of 7.5%, taking total market size toward the high hundreds of millions by the end of the decade.

Low Pressure Molding with Polyamides Market

These dynamics create a classic moment for strategic action: technologies that improve yield, reduce lifecycle costs, and address tightening environmental rules are becoming differentiators for OEMs and material suppliers alike. The economic runway is long enough to justify capital allocation, but rapid enough that delaying market entry or capability upgrades risks ceding advantage to more proactive players.

Low Pressure Molding with Polyamides Market

What this research delivers — practical, decision‑grade insight

- Quantified market sizing and multi‑year forecasts (base year 2025, historical 2020–2025, forecast 2026–2032) to support top‑down revenue planning and scenario stress‑testing.

- Supply‑chain and input‑cost analysis capturing specialty polyamide feedstock volatility and its impact on margin modelling and pricing strategies.

- Regulatory and sustainability mapping showing where formulations and process investments will be required to meet evolving VOC and chemical policy regimes.

- Competitive landscaping and vendor profiles with capability matrices that help procurement and R&D teams short‑list partners and assessing make vs. buy decisions.

- Operational playbooks for manufacturing optimization — from LPM system selection and retrofits to cycle‑time reduction, material handling and quality control best practices.

- An investment framework and prioritized initiatives (product, process, partnerships, M&A) tailored to four corporate archetypes: incumbent polymer suppliers, adhesive formulators, equipment OEMs and end‑market OEMs.

Note: The full study contains detailed segmentation, region/application splits and unit economics that are intentionally reserved for subscribers and clients. The overview here demonstrates analytical depth while directing executional readers to the full report for tactical figures required for budgeting or contract negotiation.

Competitive landscape: who to watch and why

The LPM-with-polyamides ecosystem is populated by material innovators, equipment OEMs and hybrid suppliers that straddle formulation and system integration. Market concentration metrics indicate a market where the largest three vendors account for a meaningful share, but the top five collectively command an even larger portion — a structure that supports both scale players and specialized challengers.

- Henkel AG & Co. KGaA (Düsseldorf): A technical leader in low pressure thermoplastic polyamide hot melts, Henkel’s established product platforms (TECHNOMELT®, LOCTITE®) have been redeployed into electronics, medical and industrial encapsulation. Henkel’s recent launch of bio‑based polyamides reduced emissions in targeted applications and improved recyclability — a useful template for incumbents balancing performance and ESG demands.

- Bostik (Paris): Bostik has pushed the sustainability envelope with high‑biosourced polyamide formulations and expanded high‑strength compounds for automotive. Their recent product-line expansion demonstrated measurable improvements in yield and defect reduction, underscoring the commercial payoff of formulation R&D focused on vehicle‑grade durability.

- Equipment and system providers (MoldMan Systems, LPMS International, Austromelt and others): System capability is now a commercial lever. Recent system upgrades reported by MoldMan produced near‑double‑digit production efficiency gains and material energy reductions, proving the value of integrating machine and material roadmaps when planning line upgrades.

- Regional and specialist compounders (SUNTIP, KY Chemical, Rixin, Taiyu, Huntsman): These suppliers play a critical role accelerating specialized applications — from medical‑grade formulations to tailored flame‑retardant and mechanical profiles. SUNTIP’s approvals for medical device polyamides, which materially improved product durability and reduced failure rates, exemplify how niche technical wins convert to cross‑market credibility.

Our vendor profiles in the full report go beyond public summaries, offering capability matrices, patent and product pipeline scans, plant footprints, and partner ecosystems to enable tactical sourcing and partnership dialogues.

Industry dynamics shaping 2026 choices

- Raw material volatility: Specialty polyamide feedstock price swings and supply disruptions materially affect margin sensitivity. Buyers and manufacturers must design flexible formulations and hedging policies to de‑risk production schedules.

- Regulatory tightening: Europe and China are intensifying controls on VOCs and chemical safety. Companies that preemptively reformulate and validate compliant alternatives will avoid retrofit costs and maintain time‑to‑market for regulated sectors like medical and automotive.

- Capital intensity and adoption hurdles: LPM conversion often requires higher upfront materials and equipment spend versus legacy potting or encapsulation approaches. However, where lifecycle benefits (weight, repairability, vibration dampening, IP protection) are quantified, TCO‑positive cases are already emerging.

- Sustainability as a market filter: Bio‑based polyamides and recyclability improvements are shifting procurement specifications. Early movers who can demonstrate verified lifecycle advantages will capture specification wins in electronics and new mobility segments.

Strategic implications for 2026 planning cycles

Executives framing their 2026 playbooks should prioritize three intersecting lines of effort:

- Product roadmaps aligned with regulation and ESG: Commit R&D to lower‑VOC, higher‑bio content formulations and validate them with end‑market customers to secure qualification windows that often extend 12–24 months in regulated industries.

- Operational excellence investments: Upgrade or partner for LPM systems that demonstrably reduce cycle time and energy per part. Recent field upgrades demonstrate that single‑site efficiency gains in the high‑teens percentage range are achievable and translate directly to unit‑cost reduction.

- Supply‑chain resilience and sourcing diversification: Mitigate feedstock risk through multi‑sourcing, strategic inland inventories, and longer‑dated supplier agreements. Consider backward integration or financial hedges where feasible for high‑use polymer streams.

For investors and M&A teams, the market profile supports selective consolidation: targets with differentiated formulations, validated end‑market approvals (medical, automotive), or proprietary system integration capabilities can accelerate scale while preserving premium margins.

How to use the research in your 2026 decisions

Our study is structured to be actionable within quarterly planning cycles:

- Use the market sizing and scenario outputs to set revenue targets and runway requirements for new product initiatives.

- Leverage the supplier capability assessments when drafting RFPs or negotiating long‑term supply agreements; the report highlights where single‑source exposure is most risky.

- Apply the manufacturing playbooks and case studies to construct base, upside and downside production models for capital approval packages.

- Adopt the regulatory and sustainability checklists to front‑load compliance validation into your product development sprints and avoid late‑stage redesigns.

Closing: the decisive window

The LPM-with-polyamides market is moving from engineering curiosity to industrial default in several high‑value applications. The macro trajectory — a multi‑year expansion from roughly USD 118 million in 2020 to around USD 192 million in 2025, and onward at ~7.5% CAGR through 2032 — indicates both scale and durability. That combination favors organizations that can align materials innovation, capital planning and regulatory foresight in the next 12–18 months.

PW Consulting’s full report provides the granular segmentation, pricing curves, vendor scorecards and implementation templates needed to operationalize these insights. For teams preparing 2026 budgets, sourcing strategies or M&A screens, the report is structured to convert strategic intent into measurable action plans.

Contact PW Consulting to access the full study and obtain tailored briefings, supplier negotiation support and a customized roadmap for entering or scaling in the Low Pressure Molding with Polyamides market.

For detailed analysis of this topic, please visit the official page:Low Pressure Molding with Polyamides Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com