Coverslipper Market 2026: Strategic Imperatives for Executives

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a concise, high-impact preview of our new Coverslipper Market study — engineered to inform boardroom decisions in 2026. This briefing distils the strategic implications you can act on now, demonstrates the analytics we used, and explains why the full report is a necessary next step for any organization targeting sustainable growth in automated coverslipping and related laboratory automation ecosystems.

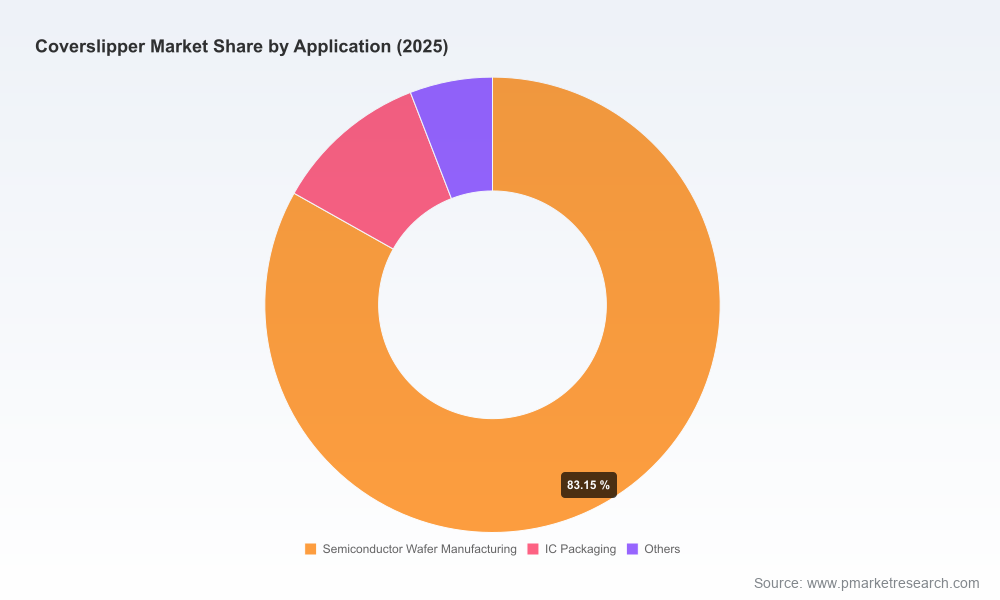

Coverslipper Market

Market trajectory at a glance

The coverslipper market has entered a steady, predictable growth phase. Using 2025 as our base year, the global market expanded from approximately USD 163.15 Million in 2020 to USD 215.0 Million in 2025. Our forecast through 2032 projects the market to reach roughly USD 344.8 Million by 2032, reflecting a compound annual growth rate (CAGR) of 5.2% over the forecast period 2026–2032. The immediate outlook for 2026 anticipates a continued uplift, positioning 2026 as a pivotal year for strategic deployment and capital allocation.

Coverslipper Market

Two cross-cutting dynamics explain the steady expansion: first, deeper adoption of automated coverslippers across clinical histology and cytology workflows as laboratories seek throughput, reproducibility, and safer solvent handling; second, incremental technology convergence, where coverslippers are being bundled into integrated staining and digital pathology chains. These dynamics create a landscape that rewards vendors and investors who can combine product reliability with systems-level interoperability.

Coverslipper Market

Why this matters for 2026 corporate decisions

- CapEx timing and procurement strategy: With predictable market growth, procurement managers and clinical lab networks can plan multi-year rollouts that optimize volume discounts and spare-parts logistics. 2026 is the year to lock preferred vendor relationships for multi-site deployments.

- R&D prioritisation: Firms should focus R&D budgets on automation features that substitute hazardous solvents and reduce manual touchpoints — these create defensible differentiation while aligning with regulatory trends.

- M&A and partnership playbooks: The market remains fragmented (top three players capture less than a quarter of global revenue; CR3 ≈ 24.6%, CR5 ≈ 26.2%), which opens mid-market M&A and distribution partnership opportunities for acquiring channels, minor technology adjacencies, or service capabilities.

- Channel and service economics: Vendors that combine consumable strategies with service-level agreements and remote diagnostics will extract higher lifetime value from installed bases.

Practical uses of the full PW Consulting report

This preview demonstrates the strategic vantage the report offers; the full study is designed as an operational toolkit rather than a descriptive pamphlet. Executives who download the complete deliverable will gain:

- Actionable market-sizing and demand-curve modeling calibrated to 2026 procurement cycles.

- Scenario-based forecasts (base, conservative, and accelerated) to stress-test investment and inventory plans across a seven-year horizon.

- Competitive benchmarking with product-level feature matrices, total cost of ownership models, and vendor value-proposition scoring.

- Commercial playbooks: go-to-market roadmaps for new entrants, channel expansion checklists for incumbents, and prioritized product feature sets for R&D investment.

- Regulatory pathway guidance and compliance risk matrices that link device classifications and solvent usage protocols to clinical procurement constraints.

- Risk-adjusted M&A scorecards and integration checklists for acquiring small automation players or consumable manufacturers.

To preserve commercial value for clients, we intentionally withhold specific regional/application revenue splits and unit-level pricing in this preview. The full report supplies these detailed tables and supporting models, enabling robust financial planning and bid-level negotiations.

Competitive landscape — who moves the needle

The competitive field is diverse, combining legacy medical-device manufacturers, niche automation specialists, and agile entrants from Asia targeting cost-performance leadership. Key companies featured in our competitive analysis include:

- SLEE medical GmbH (Nieder-Olm, Germany) — a specialist in modular glass coverslippers and film-based systems for automated histology. Recent product introductions continue to emphasise throughput and modular integration with upstream staining platforms. (https://www.slee.de)

- INTELSINT SRL (Villarbasse, Italy) — a provider of fully automated coverslippers that are designed to be part of broader histology automation lines. Their approach focuses on workflow integration and laboratory footprint optimisation. (https://www.intelsint.it)

- DAKEWE (Shenzhen) Medical Equipment Co., Ltd. (Shenzhen, Guangdong, China) — an aggressive innovator in combined staining-and-coverslipping workstations. Their recent launches have signalled a push into end-to-end automation for medium- and high-throughput labs. (https://www.dakewemedical.com)

- Sakura Finetek USA, Inc. (Torrance, California, USA) — a market-recognized developer of both film- and glass-based automated coverslippers, with clear regulatory positioning for clinical use and consumable ecosystems that lock-in customers around polymer films and mounting media. (https://www.sakuraus.com)

Our competitive chapter pairs qualitative profiling with tactical matrices — assessing each player on product breadth, channel reach, service capability, regulatory footprints, and consumable lock-in potential. We also map likely acquisition targets and alliance partners that could alter market dynamics within 12–24 months.

Technology and regulatory dynamics shaping competitive advantage

Several practical technology and regulatory developments are already influencing procurement choices in 2026:

- Regulatory positioning can be a commercial accelerator. For example, certain film-based automated coverslippers are cleared under widely recognised in vitro diagnostic device classifications; this simplifies hospital adoption cycles in regulated markets.

- Solvent and consumable engineering matters. Film-based systems that use adhesive films activated by common solvents, and glass systems that can operate with low- or zero-xylene protocols when paired with complementary mounting media, are materially improving lab safety profiles and regulatory alignment.

- Integration with staining and digital pathology platforms drives higher ARPU (average revenue per user). Vendors who offer validated workflows combining staining + coverslipping + slide tracking capture downstream value and create effective switching costs.

These dynamics mean that product roadmaps should prioritise solvent-minimisation, consumable interoperability, and validated integration kits for common lab automation ecosystems.

Recent, market-moving developments

- March 2026 — SLEE medical GmbH launched a new film coverslipper positioned for high-performance automated histology and cytology workflows. This product reflects a broader industry shift toward high-throughput film technologies.

- September 2025 — DAKEWE unveiled an integrated staining and coverslipping workstation at a major medical trade show, signalling competitive emphasis on bundled systems rather than single-point devices.

- Regulatory notes — certain film-based automated coverslippers are marketed with established regulatory classifications in mind, and some glass coverslippers now support validated zero-xylene workflows when used with specific mounting media. These factual touchpoints materially reduce adoptability friction in regulated hospital environments.

Strategic playbook for 2026

If you are an executive preparing decisions this year, consider the following prioritized actions:

- Immediate (0–6 months): Validate vendor roadmaps against your lab’s integration roadmap; negotiate multi-year service agreements; hedge consumable contracts to secure supply-chain resilience.

- Near term (6–18 months): Pilot integrated staining + coverslipping workstations in high-volume sites; quantify labor and solvent-savings to build a business case for wider rollouts; evaluate opportunistic M&A to secure distribution or consumable manufacturing.

- Medium term (18–36 months): Invest in digital workflow validation to capture value from slide-tracking and remote diagnostics; consider partnerships with digital pathology vendors to bundle offerings and increase stickiness.

How PW Consulting’s report supports execution

The full Coverslipper Market report is structured to move advisory outcomes into executable plans. It includes:

- Granular demand models and regional roll-out templates tied to procurement cycles;

- Negotiation playbooks and TCO (total cost of ownership) calculators for both glass- and film-based systems;

- Regulatory guidance linked to device classifications and solvent-use optimisation;

- Vendor scorecards and a short list of acquisition or partnership targets ranked by strategic fit and integration risk.

We intentionally limit disclosure in this preview to preserve commercial advantage for clients. The full deliverable contains the granular segment and regional tables, unit economics, and downloadable Excel models that your strategy, finance, and procurement teams can use immediately.

Next steps

For boards, private-equity sponsors, and corporate strategy teams, 2026 is the year to convert structural market growth into defensible market positions. The PW Consulting Coverslipper Market report provides the market sizing, competitive intelligence, and tactical playbooks you need to make high-confidence decisions.

Contact PW Consulting to obtain the complete study, the supporting financial models (USD, revenue in Million units), and a tailored briefing where we map specific opportunities and risks to your organisation’s strategic priorities.

For detailed analysis of this topic, please visit the official page:Coverslipper Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com