Stem Cell Therapy Market — Strategic Imperatives for 2026

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present an executive primer on our latest Stem Cell Therapy Market study. This research synthesizes market dynamics, regulatory inflection points, manufacturing realities, and an up-to-the-minute competitive map to inform high-stakes decisions in 2026. The market is no longer an academic curiosity: it has doubled in scale since 2020 and, under our base-case outlook, continues to expand at a strong mid-single digit compound annual growth rate (CAGR). For commercial, R&D, and corporate development leaders, the choices made this year will determine whether organizations capture meaningful share as the sector transitions from pioneering trials to scalable clinical programs and selective commercialization.

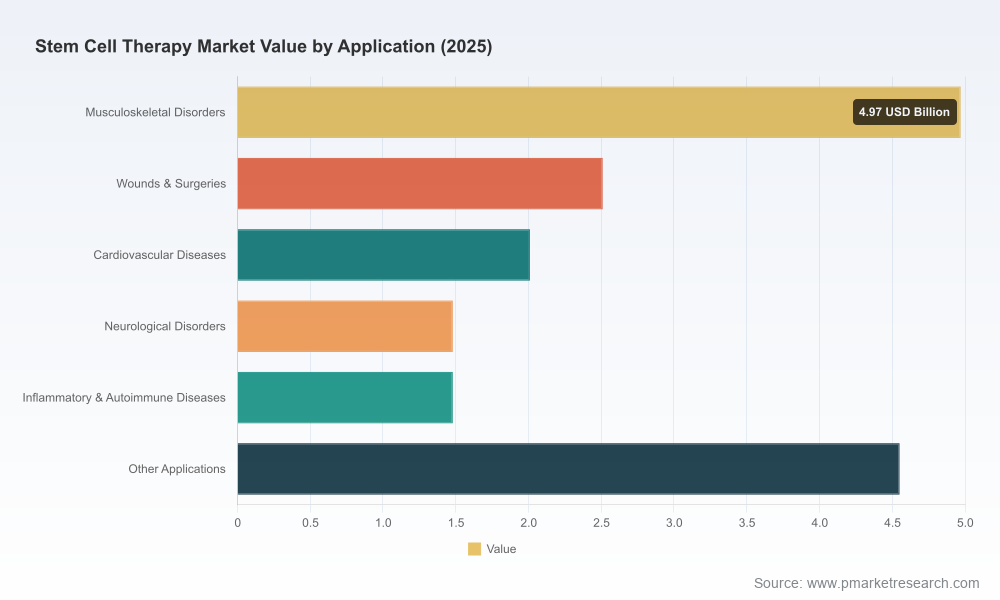

Stem Cell Therapy Market

Market at a glance — macro trajectory you can act on

Our modeling uses 2025 as the base year and traces historical performance (2020–2025) into a multi-scenario forecast (2026–2032). The market moved from single-digit billions in 2020 to a materially larger global opportunity by 2025. With a modeled CAGR of roughly 8.4% through our forecast horizon, base-case scenarios anticipate continued acceleration driven by a combination of regulatory pathway maturation, improved manufacturing economics, and an expanding clinical footprint. By the end of the forecast window, the industry is expected to approach new scale that will enable differentiated commercial strategies and greater investor confidence.

Stem Cell Therapy Market

Why this study matters for 2026 decisions

- Timing capital deployment: Our report identifies the windows where clinical readouts, regulatory clarity, and manufacturing scale converge — a critical input for venture boards, corporate M&A committees, and strategic investors deciding where to allocate growth capital in 2026.

- Prioritizing pipeline investments: We map clinical utility, reimbursement barriers, and expected time-to-market for leading therapeutic classes, enabling R&D and portfolio teams to rank indications by expected value-capture and execution risk.

- Manufacturing and supply-chain strategy: With raw-material compliance and GMP supply chains exerting outsized influence on cost and speed-to-clinic, our work provides an operational roadmap for in-house vs. CDMO strategies.

- Market-entry and commercialization playbooks: For product teams, we distill go-to-market options — from high-touch center-of-excellence rollouts to scaled commercial launches — based on likely payer behavior and physician adoption curves.

What the full report delivers (practical contents)

- Robust market sizing and three-tier forecasting scenarios (conservative, base, upside) with sensitivity analyses tied to regulatory and reimbursement outcomes.

- Clinical pipeline mapping with milestone timelines, probability-weighted valuation impacts, and commercial readiness scoring.

- Manufacturing landscape and cost-to-goods models that link material specifications (including compendial requirements) to per-dose economics.

- Competitive heat maps and capability matrices for cell sourcing, engineering platforms (including iPSC and MSC approaches), and CDMO capacity.

- Regulatory playbook and checklist for CMC, expedited pathways, and early-phase release criteria under evolving FDA guidance.

- Commercial and reimbursement scenario modeling, including price sensitivity analyses and channel strategies for hospital, clinic, and outpatient settings.

- Actionable M&A and partnership frameworks, including target profiles, valuation ranges, and integration risk assessments.

Key dynamics shaping 2026 strategic choices

The industry is being reshaped by five interconnected dynamics that drive both upside and risk.

Stem Cell Therapy Market

- Regulatory inflection — The last 12–18 months have delivered tangible regulatory signals: approvals and designations that clarify pathways for certain hematopoietic and immunomodulatory products, new FDA draft guidance on expedited review for regenerative medicine, and increased CMC flexibility for early investigational stages. These changes reduce technical uncertainty for advanced programs but shift the onus to sponsors to demonstrate robust, scalable manufacturing controls early.

- Manufacturing and raw-material rigor — Clinical-grade manufacturing requires compendial-grade raw materials and tightly controlled supply chains. Firms that lock down GMP-compliant inputs, validated seed stocks, and reproducible differentiation processes will shorten time-to-investigational-readiness and preserve value at exit or launch.

- Commercial economics and reimbursement — Outside of clearly approved indications, many stem-cell-based interventions rely on out-of-pocket or private-pay channels today. Price points vary widely by indication and care setting, and orthopedic and cosmetic use cases continue to exhibit unique payer behaviors. Effective market access strategies must therefore combine clinical evidence generation with targeted payer engagement.

- Platform convergence and vertical specialization — Two technical vectors are competing: off-the-shelf engineered iPSC platforms that enable scale, and autologous/mesenchymal approaches that emphasize niche, high-margin applications. Strategic plays that bridge platform-level scale with indication-level differentiation will command long-term advantage.

- Fragmented competitive landscape — The market remains fragmented: many specialized developers, suppliers, and CDMOs occupy adjacent parts of the value chain. Fragmentation opens opportunities for consolidation and for focused entrants to build defensible niches through partnerships and proprietary process IP.

Competitive landscape — who to watch and why

The competitive field combines platform developers, clinical-stage biotechs, CDMOs, and reagent suppliers. Below are concise strategic profiles of firms that are shaping near-term trajectories and whose moves signal where the market is heading.

- Applied StemCell, Inc. (Milpitas, CA) — A genome-engineering and iPSC specialist with a clear focus on enabling allogeneic programs. Its recent strategic partnership with a CDMO emphasizes an end-to-end approach: integrating genetic engineering with scalable manufacturing to reduce handoffs and technical transfer risk. For potential partners and investors, Applied StemCell exemplifies the value of coupling platform IP with manufacturing pathways.

- Fate Therapeutics, Inc. (San Diego, CA) — Positioned at the vanguard of off-the-shelf iPSC-derived immunotherapies, Fate’s regulatory progress — including expedited designations for an iPSC-derived CAR T program in autoimmune disease — underscores the regulatory openness to engineered cell therapeutics when CMC and clinical rationale are robust. Their model demonstrates how advanced designation can derisk development timelines and catalyze strategic collaborations.

- Brainstorm Cell Therapeutics (New York, NY) — Focused on autologous mesenchymal approaches for neurodegeneration, Brainstorm illustrates the persistent clinical demand for personalized cell therapies in high-unmet-need neurology, even as off-the-shelf approaches scale. Their work highlights the importance of durable efficacy signals for adoption in specialty clinics.

- Mesoblast Limited (Melbourne, VIC) — An exemplar of allogeneic mesenchymal strategies targeting inflammatory and degenerative diseases. Mesoblast’s programmatic focus shows how clinical and regulatory discipline can create sustainable commercial hooks around specific indications that have favorable reimbursement dynamics.

- JCR Pharmaceuticals (Ashiya, Japan) — As a manufacturer and supplier of clinical-grade stem cell products, JCR demonstrates the strategic importance of regional supply capabilities and regulatory know-how in markets with differing regulatory frameworks.

- REPROCELL, Inc. (Durham, NC) — Their regulatory submission for clinical iPSC seed clones marks a strategic bet on establishing trusted seed banks and DMFs that can accelerate sponsor programs. Seed-clone stewardship will be a commercial advantage for firms able to provide validated, regulatory-compliant starting materials.

- STEMCELL Technologies Inc. (Vancouver, BC) — A critical upstream player supplying GMP reagents and systems. Suppliers of this class will increasingly influence cost structure and process robustness; partnerships with reagent suppliers can materially shorten validation timelines for developers.

Strategic implications and recommended actions for 2026

- Prioritize CMC early: Treat manufacturing and raw-material qualification as a top-tier strategic initiative. Early investments in validated seed stocks, compendial-grade supplies, and CDMO partnerships reduce regulatory friction and protect valuation.

- Calibrate platform vs. indication choices: Balance the scale advantages of allogeneic/iPSC platforms with the revenue potential and payer dynamics of autologous or niche applications. Use our probability-weighted valuation models to stress-test portfolio choices.

- Pursue targeted regulatory engagement: Where possible, seek designations and pilot programs that shorten timelines. The recent regulatory moves signal that early, collaborative engagement with authorities yields both timing and evidentiary benefits.

- Plan commercialization as a staged expansion: Start with center-of-excellence launches or hospital-based programs in high-value indications, then iterate toward broader market access as evidence and reimbursement pathways mature.

- Use partnerships to de-risk: Strategic alliances — whether with CDMOs, reagent suppliers, or specialty biotechs — can accelerate clinical readiness while preserving optionality for later M&A or licensing outcomes.

Methodology and provenance — why you can rely on our conclusions

PW Consulting’s analysis synthesizes primary interviews, proprietary financial models, regulatory filings, clinical registries, and vendor CDMO data. Forecasts are constructed using bottom-up uptake curves tied to indication-level incidence, anticipated regulatory timing, reimbursement assumptions, and supply-chain constraints. Sensitivity and scenario testing frame upside and downside outcomes, and our competitive scoring system integrates technological defensibility, manufacturing maturity, and commercial readiness.

Next steps — get the full intelligence

This primer is designed to surface the strategic choices that will matter in 2026. The full PW Consulting Stem Cell Therapy Market report contains the granular segmentation, regional and application-level detail, company profiles, financial models, and downloadable data tables required to make executable decisions. For teams evaluating investment, licensing, or commercialization pathways, accessing the complete dataset and tailored advisory services will materially improve speed and certainty of execution.

Contact PW Consulting for report access and custom briefings that map these insights to your portfolio and strategic objectives.

For detailed analysis of this topic, please visit the official page:Stem Cell Therapy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com