¿Los Mejores Servicios De Mudanza Para Traslados Locales Y De Larga Distancia?

Networking |

2026-05-25 09:55:51

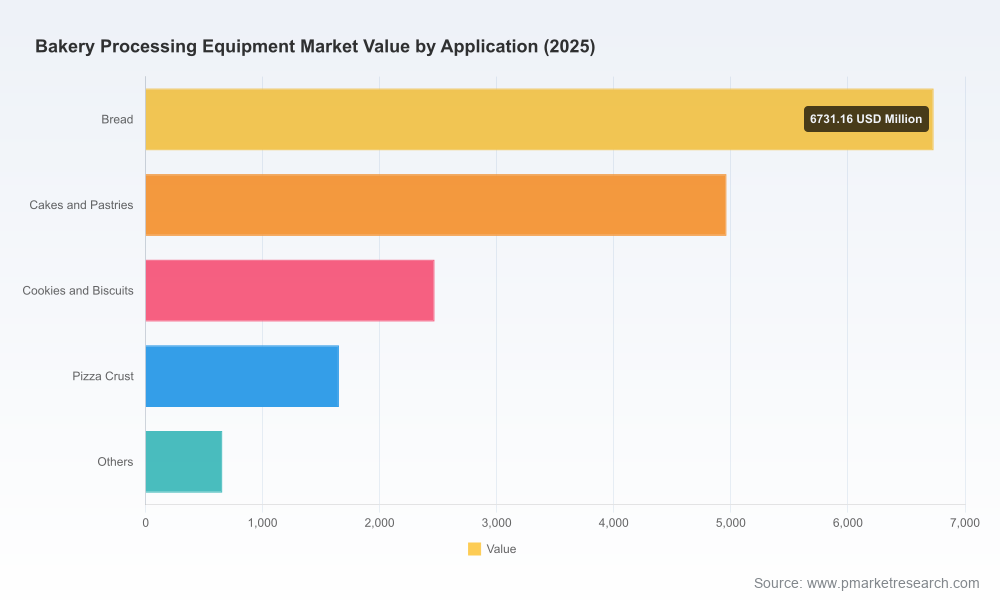

As food manufacturers, equipment OEMs, and private investors plan for 2026, the Bakery Processing Equipment market presents a clear growth arc and a set of actionable inflection points. PW Consulting’s latest study frames this market as a robust multi‑billion dollar opportunity that expanded steadily through the early 2020s and is set for accelerated expansion across the forecast window. Measured on a consistent USD basis, the market grew from roughly USD 12.2 billion in 2020 to about USD 16.47 billion in 2025, and our modeling points toward a market exceeding USD 27 billion by 2032 — reflecting a mid‑single digit compound annual growth rate of 7.6% from the 2026 outset.

Bakery Processing Equipment Market

Three strategic realities make 2026 a pivotal year for buyers, sellers, and strategic investors in bakery processing equipment:

Bakery Processing Equipment Market

The headline CAGR of 7.6% encapsulates two linked dynamics: steady baseline consumption growth and periodic step‑function investments as bakeries industrialize and pivot to higher‑margin product lines. For 2026 planners this means the market is not merely growing in size — it is diversifying in demand profile. Investment decisions must therefore balance near‑term capacity needs against medium‑term modularity and upgradability.

Bakery Processing Equipment Market

From an investment standpoint, the trajectory supports three capital allocation strategies: (1) targeted replacement of legacy assets to meet hygiene and labor‑efficiency targets, (2) modular expansions to support new product introductions, and (3) selective pursuit of scale via integrated continuous processing lines in blue‑chip plants. Each strategy maps to different supplier profiles and risk exposures.

The competitive map combines established industrial engineering leaders, specialist process equipment vendors, and regional manufacturers. Key firms covered in the study include global engineering brands and focused bakery systems specialists. What differentiates winners from the pack is not just machine performance but portfolio completeness, aftermarket capability, and the ability to certify compliance with sanitary and food‑safety standards.

Our competitive review profiles leading vendors, assesses product roadmaps, and benchmarks aftermarket capabilities. The study also quantifies market concentration and explores how CR3/CR5 dynamics influence pricing power, warranty design, and channel strategy.

Regulatory clarity and tightening sanitation standards are reshaping procurement specifications and product roadmaps. Recent standards and lists — including new food protection and sanitation requirements and accepted equipment lists for dairy and meat adjacent processing — have practical consequences for design specification, acceptance testing and documentation during procurement cycles.

For 2026 buyers this means equipment evaluation must include not only performance metrics but third‑party certifications, traceability of materials, and documented cleaning protocols. For OEMs, proactive certifications and transparent validation packages accelerate adoption among regulated customers.

This study was built with the buyer and strategist in mind. It contains modelling, tools and playbooks that a procurement or strategy team can put to work immediately:

To preserve commercial value for subscribers and clients, the report provides these assets alongside proprietary sub‑segment tables, supplier revenue breakdowns and regional demand models. Those detailed datasets are intentionally gated to guide vendors and buyers seeking executable market entry and procurement strategies.

Investors should view the bakery processing equipment market as a combination of steady underlying demand and periodic capital events driven by regulatory shifts, new product introductions, and retail/foodservice channel expansion. Valuation premium will increasingly attach to companies that demonstrate recurring revenue streams (spares, service contracts, software), certification credentials, and robust channel relationships. For private equity, bolt‑on consolidation plays that add geographic reach or aftermarket scale are particularly compelling.

Trade events and industry expos continue to validate both the growth narrative and the rapid rate of product innovation. Major industry gatherings in 2025 and 2026 showcased new integrated lines, hygienic innovations and digital service offerings — confirming the technology transitions discussed in this report. Additionally, updates to sanitation and equipment acceptance lists from national standards bodies are already being integrated into procurement specifications across regulated segments.

This introduction outlines the strategic contours that will shape capital and procurement decisions in 2026. PW Consulting’s full report contains the detailed sub‑segment financials, regional demand models, and supplier revenue tables that underpin the executive guidance above. Those datasets and proprietary vendor benchmarks are intentionally held behind our subscription gateway to preserve actionable insight for clients who require implementation‑grade intelligence.

For detailed analysis of this topic, please visit the official page:Bakery Processing Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com