Royal Clinic Saudia for Modern Skin Care Innovation

Health |

2026-05-19 07:57:49

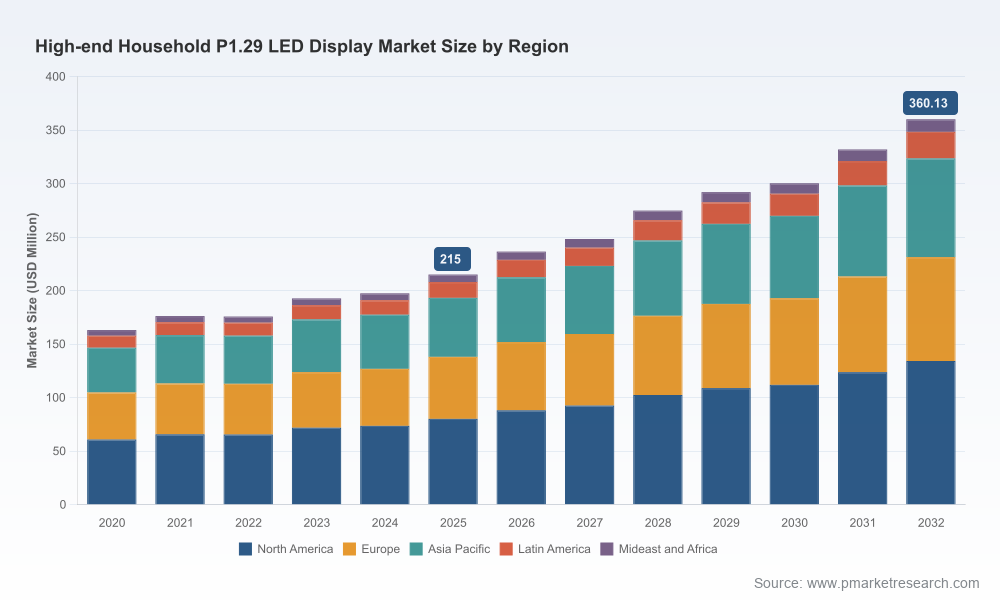

As premium residential displays continue to migrate from large LCD and OLED panels toward ultra-fine-pitch LED video walls, the P1.29 mm class has emerged as a strategic battleground for incumbents and challengers alike. Our market model — based on rigorous primary interviews, component-level cost builds, and end-use adoption curves — places the global high-end household P1.29 LED display market at approximately USD 215.0 Million in the base year 2025. After a period of steady expansion (2020–2025), the market is forecast to grow at a compound annual growth rate (CAGR) of 7.8% through the 2026–2032 horizon, reaching an estimated USD 360.13 Million by 2032.

High-end Household P1.29 LED Display Market

This preview distills the directional implications of those trends for strategic decisions in 2026: product investments, manufacturing footprint, sourcing, channel strategy, pricing architecture, and M&A priorities. It is expressly designed to demonstrate the depth and actionability of PW Consulting’s full study while reserving proprietary granular splits and node-level data for report subscribers.

High-end Household P1.29 LED Display Market

Timing matters: 2026 is the inflection year for several industry dynamics — component supply normalization, new microLED/OLED hybrid launches, and regulatory adaptations around residential brightness and safety. Firms that finalize their product roadmaps and sourcing strategies in early 2026 will capture the first-mover premium in a market growing at roughly 7.8% annually.

High-end Household P1.29 LED Display Market

High capital intensity and long lead times: P1.29 mm assembly and qualification require specialized SMT processes, precision driver electronics, and controlled optical calibration. Decisions on factory upgrades versus outsourced module buys must weigh multi-year ROI under the market growth profile highlighted above.

Value beyond units: In premium residential deployments, value accrues not just from unit sales but from integrated services — design, custom framing, calibration, AV integration, and extended warranties. The market trajectory supports service-led monetization strategies that drive higher lifetime value.

Our analysis identifies four thematic forces shaping vendor economics and go-to-market choices in 2026:

Supply-chain constraints and cost volatility. Premium SMD LEDs and precision optics remain subject to periodic constrained availability, with lead times that can extend multiple months for top-tier components. Critical input materials used in RGB LED chips — notably gallium and indium derivatives — exhibit quarter-to-quarter price volatility that materially alters marginal cost models.

Trade and regulatory friction. Ongoing tariff regimes and regional trade policy introduce meaningful import cost asymmetry for assemblies sourced from certain origins. Vendors must model effective landed costs by scenario and consider local assembly or bonded manufacturing to protect margin.

Standards and safety thresholds. Residential installations of very high-brightness displays encounter specific photobiological safety requirements; compliance will affect product design, certification timelines, and installation protocols. For example, displays exceeding defined luminance thresholds require documented conformance testing and installer training.

Labor and precision manufacturing premiums. High-precision SMT and module repair demand experienced labor and sophisticated tooling; assembly labor rates for premium modules can command a significant premium over baseline electronics assembly rates, compressing margin for low-cost assembly strategies.

The vendor map in 2025–2026 is a mix of large integrated panel manufacturers, projector/processing specialists, and focused module OEMs. Market concentration metrics show a moderately concentrated industry (top-3 share ~45%; top-5 ~60%), indicating meaningful scale advantages but also opportunity for specialized players to capture niches.

Samsung Display (Suwon, South Korea): Strong capabilities in microLED and high-resolution panel engineering position Samsung to pursue integrated luxury residential systems. Recent strategic partnerships emphasize ecosystem play (processing + consumer microLED) rather than component-only competition.

LG Display (Seoul, South Korea): With advanced OLED and microLED research, LG is focusing on differentiated pixel-driving techniques and HDR optimization to appeal to premium home theater buyers and bespoke installers.

Panasonic Corporation (Osaka, Japan): Panasonic’s historic strength in end-to-end systems and B2B integration supports all-in-one residential solutions and turnkey AV packages for high-net-worth installations.

Sharp Corporation (Sakai, Japan): Recent capability acquisition in microLED driver tech accelerates Sharp’s roadmap for compact, high-brightness modules — a competitive edge where installation footprint and color fidelity matter.

Barco (Kortrijk, Belgium): A specialist in high-performance video walls, Barco’s X1.2 series and processing expertise make it a go-to partner for premium indoor installations that require unmatched image processing and scaling.

Leading Chinese OEMs (AOTO, Liantronics, Absen, Leyard, Unilumin): These firms combine aggressive R&D in small-pitch COB/GOB technologies with flexible manufacturing footprints and strong price/performance curves. They remain key suppliers for system integrators and increasingly for direct-to-consumer channels.

Specialist integrators (e.g., AVMS): Niche European integrators focus on high-resolution module assembly and turnkey indoor systems, adding value via certification, custom enclosures, and localized support.

Notable moves to watch (selection): a strategic co-development between a major consumer microLED developer and a high-performance video-wall processor in 2025; a leading manufacturer’s launch of a microLED home display optimized for premium home theater; and acquisition of driver-technology IP to accelerate microLED roadmap execution. Each of these events underscores a trend toward ecosystem aggregation and IP consolidation.

Subscribers receive a hands-on playbook designed for executives and product teams making resource allocation decisions in 2026. Deliverables include:

Proprietary market-sizing model (2020–2032) with scenario toggles and sensitivity to component pricing, tariff regimes, and adoption curves.

Unit economics and BOM-level cost build-ups for representative P1.29 mm SKUs under multiple sourcing strategies.

Regulatory and certification checklist mapped to installation classes and brightness tiers, with recommended test houses and timeline estimates.

Supplier map and risk heatmap (tiered suppliers for LEDs, drivers, optics, and electronics), plus negotiation playbooks and contract templates.

Channel and service monetization models for premium residential deployments: installation, calibration, financing, and subscription service levers.

Competitive benchmarking, product-spec scorecards, and go-to-market options for OEM, ODM, and integrator strategies.

Targeted M&A and partnership shortlist based on technology fit, IP ownership, and regional logistics advantages — with diligence checklists.

Hedge component supply and price risk: sign dual-source agreements for high-brightness LEDs and negotiate price collars for critical minerals.

Validate certification pipelines: initiate photobiological compliance testing early for any SKU that may exceed residential luminance thresholds.

Assess manufacturing trade-offs: model nearshoring or bonded assembly to mitigate tariff exposure and reduce lead-time risk for high-priority markets.

Pilot integrated experiences: deploy a limited set of fully integrated home installations with select channel partners to refine install, calibration, and service economics before scaling.

Pursue selective partnerships: prioritize alliances that combine display IP with premium processing and installation ecosystems to capture the higher-margin, experience-first customers.

For executives preparing capital and product decisions in 2026, this body of work provides both the quantitative trajectory and the qualitative playbooks required to convert market growth into durable advantage. The market is sizable enough to justify differentiated investments yet concentrated enough that scale and IP matter. Our full study packages the proprietary granular segmentation, scenario models, and supplier-level intelligence you need to execute with confidence; this preview intentionally omits those splits to protect proprietary valuation and go-to-market signals.

To review the complete dataset, detailed segment economics, and downloadable playbooks, please access the full report via the PW Consulting publications page.

For detailed analysis of this topic, please visit the official page:High-end Household P1.29 LED Display Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com