Custom Ecommerce Web Design Services: Building Online Stores for Sustainable Growth

Other |

2026-06-23 19:33:14

Key Highlights

Why This Matters Now

The Solid Oxide Fuel Cell Market is facing a simultaneous challenge: reducing emissions while maintaining reliable electricity supply. Aging power grids, extreme weather events, and rising electricity consumption from digital infrastructure are accelerating demand for decentralized clean energy systems.

Solid oxide fuel cells are gaining attention because they generate electricity through electrochemical conversion rather than combustion. This allows lower emissions, higher efficiency, and improved energy security compared with conventional fossil fuel-based power systems.

The rapid expansion of artificial intelligence infrastructure and hyperscale data centers has further increased demand for dependable power solutions. Fuel cell systems are becoming an attractive alternative because they provide continuous electricity generation without depending entirely on grid availability.

Government support for hydrogen economies, carbon reduction programs, and clean technology investments is also strengthening market momentum. Manufacturers are responding by improving durability, reducing costs, and developing fuel-flexible systems capable of operating with hydrogen, natural gas, and renewable fuels.

Market Overview

The Solid Oxide Fuel Cell (SOFC) Market represents advanced electrochemical energy systems that convert chemical energy from fuels such as hydrogen and natural gas into electricity through high-temperature ion conduction using ceramic electrolytes.

Unlike conventional energy generation technologies, SOFC systems provide high electrical efficiency ranging between 60% and 85%, while producing fewer greenhouse gas emissions. Their ability to operate continuously makes them suitable for stationary power generation, backup systems, industrial facilities, military applications, and data centers.

Market growth is being driven by rising global decarbonization targets, increasing investment in hydrogen infrastructure, and the need for resilient energy networks.

The supply landscape is also evolving as major manufacturers expand production capabilities. Companies including Bloom Energy, Ceres Power, and FuelCell Energy are scaling manufacturing capacity while improving stack performance and reducing production costs.

Demand is particularly strong in regions where electricity reliability and carbon reduction are strategic priorities. Utilities are adopting SOFC systems for distributed generation, while commercial operators are using them to reduce dependence on traditional grids.

Key Trends Driving Growth

Reversible SOFC Systems Enable Hydrogen Production

A major industry shift is the development of reversible Solid Oxide Fuel Cell and Solid Oxide Electrolyzer Cell (SOEC) technologies. These systems can generate electricity when energy is required and produce hydrogen when excess renewable power is available.

Companies such as Bloom Energy and Mitsubishi Power are investing in dual-function systems that support both clean electricity generation and hydrogen production.

This technology improves asset utilization and strengthens the role of SOFC systems in future hydrogen economies.

Lower-Cost Manufacturing Improves Market Adoption

Historically, high manufacturing costs limited SOFC deployment. However, companies are adopting steel-based stacks, advanced manufacturing methods, and ceramic production improvements to reduce costs.

Ceres Power and Sunfire GmbH are focusing on scalable manufacturing approaches designed to improve commercial competitiveness.

Lower production costs are expected to expand adoption beyond industrial applications into residential and commercial markets.

Data Centers Become a Strategic Growth Market

The rapid expansion of cloud computing and artificial intelligence infrastructure is increasing demand for reliable electricity sources.

Fuel cells are gaining interest among data center operators because they provide continuous power, reduce carbon emissions, and support energy independence.

Companies are increasingly evaluating SOFC systems as alternatives to diesel backup generators and conventional grid dependency.

Government Policies Accelerate Investment

Energy transition policies across major economies are supporting SOFC development. Clean energy incentives, hydrogen programs, and emissions reduction targets are encouraging companies to invest in fuel cell infrastructure.

The United States remains a major investment hub due to government-supported hydrogen initiatives and clean technology funding programs.

Explore detailed analysis, insights, and growth opportunities

Segment Insights

Planar SOFC Segment Maintains Market Leadership

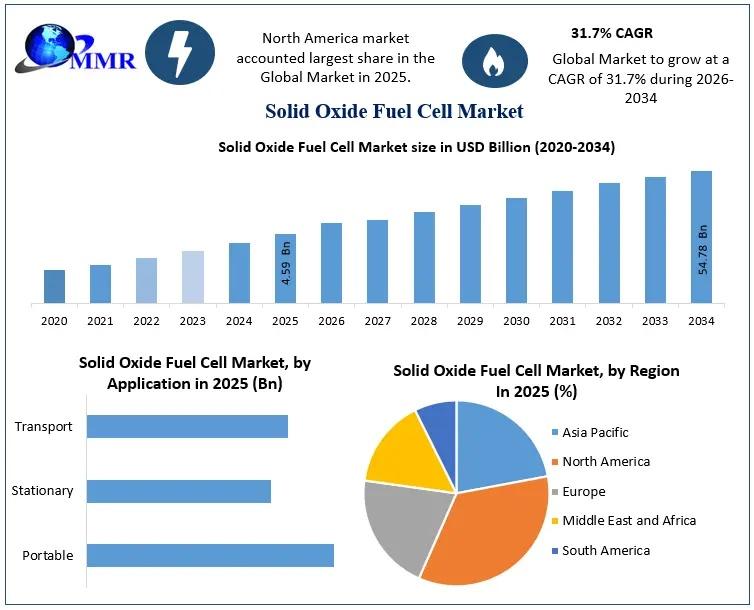

Based on type, the market is segmented into planar and tubular technologies. The planar SOFC segment dominated the market in 2025 with approximately 65% share.

Planar designs have gained commercial preference due to higher power density, compact structure, and easier scalability. These characteristics make them suitable for stationary power generation, commercial buildings, and data center applications.

Planar SOFC systems can achieve electrical efficiencies of approximately 55–65%, providing advantages over tubular alternatives in large-scale deployments.

The dominance of planar technology reflects growing demand for compact, high-performance energy systems where space efficiency and operational reliability are critical.

Power Generation Segment Drives Market Demand

By end-user, power generation represented the largest market segment in 2025.

Utilities, commercial facilities, residential complexes, telecom networks, and industrial facilities are adopting SOFC systems for distributed electricity generation and backup power.

The segment benefits from increasing concerns over grid instability and rising electricity demand.

Bloom Energy has strengthened this segment through distributed power deployments across the United States and international markets, including South Korea, Japan, and India.

Hydrogen Generation Emerges as a High-Potential Application

Hydrogen generation is becoming an increasingly important application area as industries seek low-carbon alternatives.

SOFC technology integrated with electrolysis capabilities allows companies to produce hydrogen more efficiently, creating new opportunities in industrial decarbonization, transportation fuels, and renewable energy storage.

Regional Growth Story

North America Leads Global Adoption

North America held the largest share of the Solid Oxide Fuel Cell Market in 2025 due to technological leadership, strong investment activity, and supportive clean energy policies.

The United States has emerged as the leading market, supported by advanced research programs, commercial deployments, and growing demand from utilities and data centers.

Companies such as Bloom Energy have established significant commercial presence in the region, strengthening North America's position in SOFC deployment.

The region benefits from a mature energy infrastructure, government incentives, and increasing demand for reliable distributed electricity.

Asia Pacific Gains Momentum Through Manufacturing Strength

Asia Pacific is expected to register rapid growth due to rising electricity demand, expanding industrial activity, and government investment in hydrogen technologies.

Japan and South Korea are leading regional adoption through residential micro-CHP systems and utility-scale applications.

Manufacturers including Mitsubishi Power, Aisin Corporation, and Kyocera are strengthening the regional supply chain.

Europe Focuses on Hydrogen Integration

Europe is advancing SOFC adoption through hydrogen economy initiatives and industrial decarbonization programs.

Germany, the United Kingdom, and Italy are emerging as important markets due to investments in clean energy technologies and fuel cell manufacturing.

Companies such as Bosch, Ceres Power, and Sunfire GmbH are supporting regional technology development.

Competitive Landscape

The Solid Oxide Fuel Cell Market is becoming increasingly competitive as manufacturers move from pilot projects toward commercial-scale deployment.

Bloom Energy maintains a strong market position through large-scale stationary power installations and data center solutions. Its focus on high-efficiency systems positions the company as a major supplier for commercial energy applications.

FuelCell Energy differentiates itself through industrial-scale solutions, hydrogen production capabilities, and carbon capture integration initiatives.

European companies such as Ceres Power and Sunfire GmbH are focusing on cost reduction through advanced manufacturing and reversible SOFC technologies.

Japanese players including Mitsubishi Power and Aisin Corporation are strengthening their position through utility and residential applications.

The competitive landscape is shifting toward companies that can achieve lower manufacturing costs, improve system durability, and integrate hydrogen capabilities.

Recent Developments

Future Outlook

The Solid Oxide Fuel Cell Market will be shaped by companies that successfully combine lower-cost manufacturing, hydrogen integration, and reliable large-scale deployment, while manufacturers unable to overcome cost and durability challenges risk losing market share.

About Maximize Market Research

Maximize Market Research Pvt. Ltd. (MMR) is a global market research and consulting company that provides reliable, data-focused, and practical business insights. The firm serves a wide range of industries, including healthcare, pharmaceuticals, technology, automotive, electronics, chemicals, personal care, and consumer goods. Through market forecasts, competitive analysis, strategic consulting, and industry impact assessments, MMR helps organizations understand changing market conditions, identify growth opportunities, and make informed business decisions for long-term success.

Contact Us :

2nd Floor, Navale IT Park Phase 3

Pune Banglore Highway, Narhe

Pune, Maharashtra 411041, India

+91 9607365656

[email protected]