Asia-Pacific Water Purifier Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-13 09:06:32

As PW Consulting’s lead industry analyst, I present a focused strategic preview of the Blood and Fluid Warmer market intended to orient executive decisions in 2026. The market has shifted from a niche clinical adjunct into a core component of perioperative and emergency care pathways. Our baseline modelling (base year 2025) shows the industry at roughly USD 1.29 billion, growing at a compound annual growth rate of 7.85% through our forecast horizon to 2032. By 2032 the market is projected to exceed USD 2.17 billion — a trajectory that creates discrete windows of opportunity for manufacturers, health systems, private equity sponsors, and clinical technology partners.

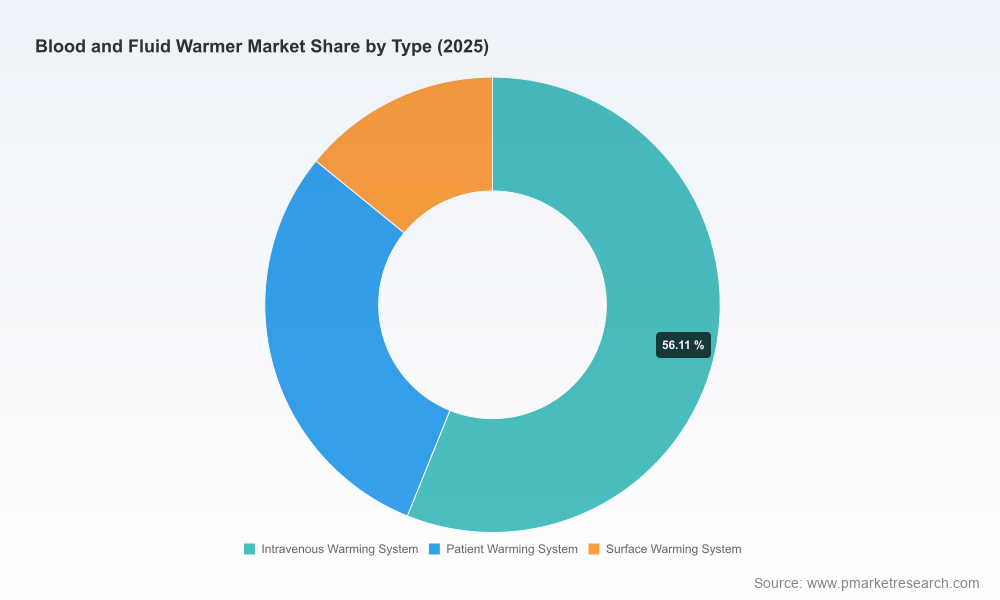

Blood and Fluid Warmer Market

Regulatory and clinical guideline momentum: The AORN guideline update in 2025 explicitly reinforced active warming strategies including fluid warming, elevating clinical demand signals across perioperative and critical care settings.

Blood and Fluid Warmer Market

Reimbursement and economic levers: Coding and payment updates scheduled for 2026 materially change reimbursement dynamics for outpatient and hospital-based uses, altering product economics and procurement negotiation leverage.

Blood and Fluid Warmer Market

Technology and safety focus: Market entrants and incumbents are racing to integrate safety features such as automatic air detection and pediatric-specific clearances while balancing the cost cadence of disposables and reusable components.

These three vectors converge in 2026. Organizations that treat 2026 as a planning horizon to reorganize product portfolios, update go-to-market playbooks, and secure regulatory clarity will gain the first-mover advantage as adoption accelerates.

From a macro perspective, the market’s growth profile is robust and consistent: after expanding from under a billion dollars in 2020 to approximately USD 1.29 billion in 2025, our forecast anticipates continued expansion to just over USD 1.41 billion in 2026 and into the low billions by the end of the decade. This trajectory is driven by expanding indications in surgical and neonatal care, greater adoption in emergency and pre-hospital settings, and incremental product innovation that lowers barriers to use.

Despite this growth, concentration metrics indicate a market that remains contestable. Our CR3 and CR5 measures point to moderate concentration among leading firms, leaving substantial room for disruption by specialized device innovators and targeted M&A by larger medtech platforms.

Manufacturers: Prioritize safety features (air detection, flow and temperature monitoring), pediatric labeling, and operational ergonomics for emergency and transport use. Portfolio strategies should balance low-margin disposables with differentiated capital or system sales that create stickiness with hospitals.

Hospital and health system procurement: Reframe sourcing decisions around total cost of ownership and clinical outcomes rather than unit price alone. The upcoming reimbursement changes make it essential to model hospital margin impact, device utilization, and compatibility with existing infusion ecosystems.

Investors and acquirers: Seek targets that combine clinical differentiation with scalable manufacturing and regulatory clearances in priority segments (e.g., pediatric and moderate-to-high flow devices). Expect higher valuation premia for companies that can demonstrate integrated infusion-warming solutions and strong post-market safety practices.

Clinical leaders: Incorporate fluid warming into perioperative hypothermia prevention bundles and neonatal thermal care pathways. Rapid adoption will hinge on clear procedural protocols and demonstrable outcomes improvements.

The competitive field blends global diversified healthcare companies with specialist device builders. Established medical device platforms have the advantage of integrated hospital relationships and distribution scale; specialist innovators are introducing focused features — battery-powered portability, dry-technology warming, automatic air-in-line protection, and pediatric-focused systems.

Incumbent platforms continue to defend share through bundled hospital contracts and integrated fluid management offerings.

Small to mid-size specialists are winning adoption in emergency medicine and transport use cases where portability and rapid deployment are decisive.

Recent regulatory actions and approvals — including new FDA clearances for moderate-to-high flow systems with automatic air detection and explicit pediatric indications — are reshaping clinical trust and purchase criteria.

Key organizations shaping this market include multinational device manufacturers and nimble innovators alike. Several entities have advanced product sets addressing portability and safety; others have issued post-market notices that serve as important risk signals. Leaders and challengers cited in our intelligence include global diversified medtech firms, established infusion/critical-care specialists, and focused portable device makers. Their strategic playbooks vary from vertical integration and system bundling to targeted clinical trial strategies and tactical regulatory clearances.

Regulatory scrutiny remains elevated: FDA safety communications on intravascular air risk underline the need for robust engineering controls and post-market surveillance. The 2025 label correction by a major incumbent on temperature and flow specification is a reminder that compliance lapses can materially affect market trust and uptake.

Reimbursement shifts are material for commercial modelling: Coding changes effective mid-2026 alter outpatient economics and influence hospital purchasing pathways. Stakeholders must update commercial assumptions to avoid margin erosion.

Materials and test standards matter: Advanced devices incorporate coated aluminum heating chambers and are subject to leaching and biocompatibility testing per established ASTM and FDA guidelines. Sourcing strategies should include testing contingencies and supplier audits.

Our full market study is designed to be immediately operational for corporate planning and investor diligence. Highlights include:

Market sizing and 2020–2032 forecasting with scenario trees that isolate demand by clinical use case and product archetype (note: detailed segment tables are available in the full report only).

Competitive scorecards and strategic positioning maps for leading and emerging suppliers, including product feature matrices and regulatory status timelines.

Go-to-market playbooks for new product launches, procurement negotiation templates, and bundled offering design guidance.

Regulatory and reimbursement trackers with suggested mitigation steps and coding readiness checklists for the 2026 payment environment.

Supply chain and raw-material risk assessments, including ASTM-compliance pathways for heating chamber materials and contingency sourcing strategies.

M&A screening filters and valuation comparators that reflect the market’s moderate concentration and the premium attached to pediatric and high-flow clearances.

To honor the “trailer” principle: this preview demonstrates the analytical depth and practical scope of the study while intentionally withholding granular split tables and region-by-application percentages so stakeholders will consult the full dataset for transaction-level decisions.

Update internal revenue and margin models to reflect the 7.85% CAGR baseline and test sensitivity to reimbursement shifts effective July 2026.

Audit labeling and clinical claims against the latest FDA and AORN guidance; prioritize post-market surveillance investments that mitigate air-in-line and thermal accuracy risks.

Accelerate pediatric-specific submissions where possible: regulatory clearance in this niche drives premium adoption in neonatal and pediatric hospitals.

Rework commercial contracts to reflect total cost of ownership and clinical outcome metrics rather than per-unit price only.

Secure supply chain assurances for specialized materials and validate testing protocols for coated heating chambers and disposable sets.

Design pilot deployments in emergency medicine and transport that emphasize ease-of-use and battery life; collect real-world evidence to accelerate system-wide adoption.

The Blood and Fluid Warmer market in 2026 is both larger and more strategically consequential than many organizations appreciate. Clinical guideline updates, reimbursement reclassification, and device-level safety innovation combine to create a compressed window for value capture. The macro growth story is clear — the industry is expanding at a near-8% CAGR with predictable scale by 2032 — but the winners will be determined by who best integrates safety, regulatory readiness, clinical evidence, and economically sensible commercial models.

PW Consulting’s full report provides the granular segmentation, regional breakdowns, and transaction-level datasets required to convert these strategic signposts into executable plans. For clients preparing budgets, M&A pipelines, or launch programs in 2026, use this preview as the decision framework — and consult the detailed study for the line-of-sight intelligence that closes deals and secures market share.

For detailed analysis of this topic, please visit the official page:Blood and Fluid Warmer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com